Has your insurance company declared your car a total loss and presented a settlement offer that feels far too low? You are not alone, and you don’t have to accept their initial valuation. This guide will show you how finding a certified total loss appraisal near me is the most effective step you can take to challenge a lowball offer and get the compensation you deserve.

This isn’t just about getting a second opinion. It’s about arming yourself with objective, data-driven proof to level the playing field and secure the full insurance total loss payout you are rightfully owed.

Your Guide to Challenging an Insurer’s Lowball Offer

When an insurance adjuster declares your vehicle a total loss, their first offer is rarely their best. Think of it as an opening bid in a negotiation. Their primary goal is to close your claim as quickly and inexpensively as possible for their company.

Accepting that initial number without question can leave thousands of dollars on the table—money you need to purchase a truly comparable replacement vehicle.

The good news is that you have the right to dispute their valuation. An independent appraisal provides the credible evidence you need to negotiate effectively.

Why a Total Loss Appraisal Matters

Insurance companies rely on automated valuation software that often fails to capture your vehicle’s true worth. These systems are designed for speed and cost-efficiency, not accuracy. They frequently overlook key details like:

- Excellent Condition: The software may not properly account for a vehicle that was meticulously maintained.

- Recent Upgrades: New tires, brakes, or a premium sound system are often ignored.

- Local Market Value: The system may use data from other regions, not what similar cars are selling for in your specific area.

This results in a skewed car value after accident calculation that benefits the insurer, not you. An independent appraiser works for you. Their sole focus is to determine the accurate, fair market value of your vehicle before the accident.

An independent appraisal from a certified professional is your best tool. It replaces the insurer’s generic report with a detailed analysis grounded in real-world data, instantly strengthening your negotiating position. For a complete playbook, check out our step-by-step guide to disputing a total loss offer.

The principle of seeking fair compensation is universal. Whether it’s an insurance claim or another valuation dispute, having an expert on your side is critical. For instance, the same ideas apply when it comes to understanding your rights when the government threatens to take your land. An independent appraisal ensures you don’t leave money behind.

The Problem with Automated Valuations

Let’s call it what it is: a conflict of interest. An insurance company’s goal is to minimize claim payouts. The software they use, such as CCC ONE or Mitchell, is simply a tool to achieve that goal, often at your expense.

This is how your carefully maintained, low-mileage car—the one you just put new tires on—gets compared to a high-mileage base model that sold at a wholesale auction two states away. It’s a standard play designed to protect their bottom line.

How Modern Tech Stacks the Deck Against You

Today’s cars are more complex than ever, which worsens the problem. Vehicles are loaded with sophisticated technology, from advanced driver-assistance systems (ADAS) to a network of interconnected sensors.

A seemingly minor collision can damage expensive components, sending repair costs soaring and making a “total loss” declaration more likely. This is a critical factor that automated valuation tools often don’t weigh properly against your car’s actual pre-accident market value. You can discover more insights about how market trends affect appraisals.

This is where an independent appraisal becomes your most powerful tool. It provides the hard, data-backed evidence you need to push back against the insurer’s lowball offer and is essential for winning your insurance total loss payout negotiation.

Choosing the Right Appraiser: Local vs. Online Services

When you start searching for a “total loss appraisal near me,” you’ll find two main options: a traditional local appraiser who physically inspects your car, or a modern online service that handles everything digitally.

Making the right choice can significantly impact the speed, cost, and outcome of your insurance claim.

The Old Way vs. The New Way

A local appraiser might sound appealing because they physically inspect the vehicle. However, this traditional approach often comes with serious downsides, including long wait times for an appointment, higher fees to cover travel, and limited availability in rural areas.

Online appraisal services have revolutionized the process. They offer a faster, more convenient, and more affordable path to getting the same—or better—results. By using digital photos, documents, and comprehensive market data, they eliminate the need for a physical inspection, saving you time and money.

The Modern Advantage of Online Appraisals

Online services like SnapClaim provide a certified, court-ready report backed by real data, but without the delays and high price tag of a traditional appraiser.

Instead of waiting for someone to show up, you can submit your car’s information and photos directly from your phone. In many cases, you can receive a comprehensive report in less than an hour.

This isn’t just about speed; it’s about accuracy. Our process is built on robust, real-time market data. We analyze thousands of data points—from local dealer listings to private party sales—to pinpoint your vehicle’s true pre-accident value. An insurance adjuster will find it difficult to argue with a report built on such objective evidence.

If you want to dig deeper into what makes a great appraiser, check out our guide on finding the best diminished value appraisers.

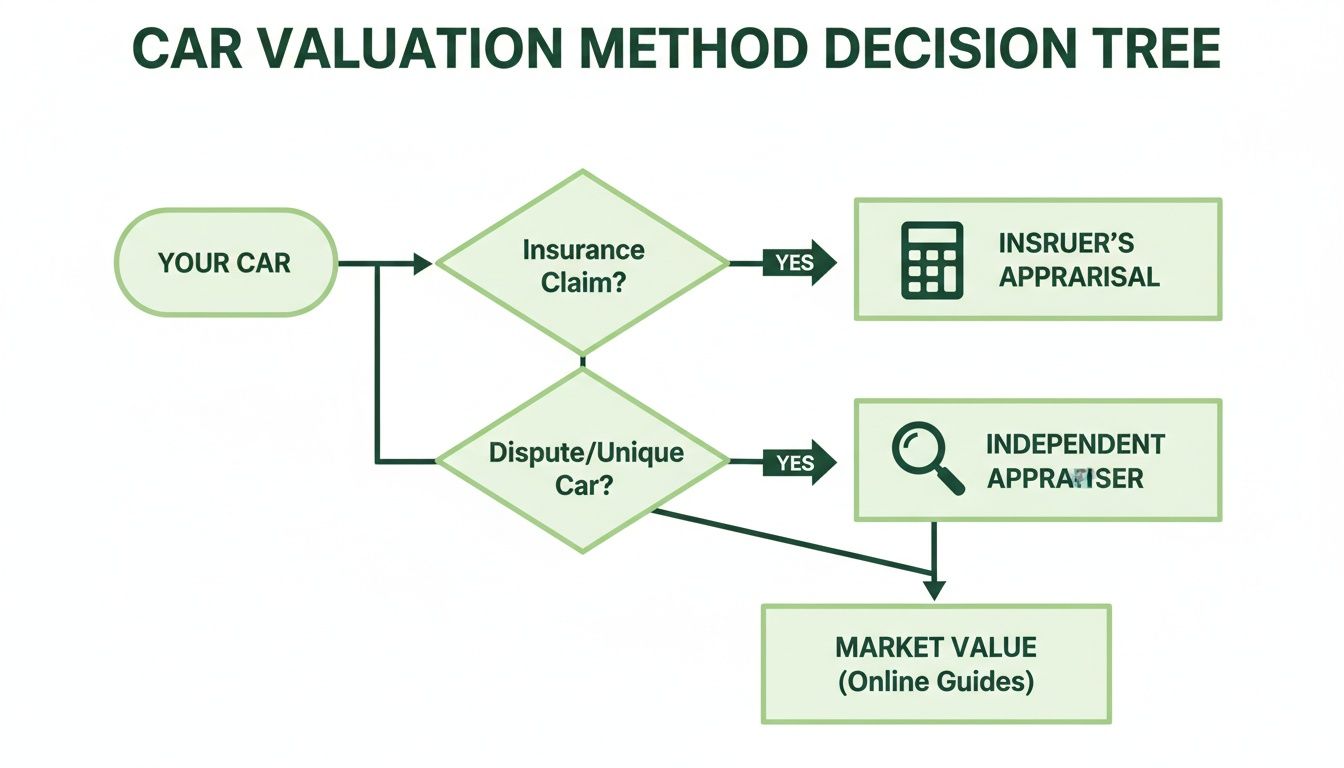

This decision tree shows the two main paths you can take to figure out your car’s value after a wreck.

As the graphic shows, while your insurance company has its own tools, an independent appraiser is your best bet for an unbiased valuation that gets you paid fairly.

Comparing Your Options Side-by-Side

To see the difference clearly, let’s compare a traditional local appraiser with an online service like SnapClaim.

Local Appraiser vs. Online Appraisal Service (SnapClaim)

| Feature | Local Appraiser | SnapClaim Online Appraisal |

|---|---|---|

| Turnaround Time | Days or even weeks | Under 1 hour |

| Cost | Typically higher ($300-$500+) | More affordable |

| Convenience | Requires scheduling an in-person meeting | Fully online, submit anytime from anywhere |

| Data Source | Local knowledge, manual research | Comprehensive, real-time market data |

| Report Validity | Varies by appraiser | Certified and court-ready |

Ultimately, choosing an online service allows you to challenge your insurer’s lowball offer almost immediately. You get the expert proof you need without putting your life on hold, helping you reach a fair settlement faster.

Getting Ready for Your Total Loss Appraisal

A strong appraisal is built on solid evidence. To achieve the best possible outcome, you need to provide your appraiser with everything required to prove your vehicle’s true pre-accident value. Fortunately, preparing is easier than you might think.

Think of yourself as building a case for your car. Every document, receipt, and photo is a piece of evidence that tells the story of your vehicle’s real worth.

Pull Together Your Essential Paperwork

First, gather the official documents. These items establish ownership and provide a solid foundation for the appraisal.

Here’s your essential document checklist:

- Vehicle Title and Registration: The non-negotiable proof of ownership.

- Bill of Sale: If you bought the car recently, this helps establish its recent market value.

- The Insurer’s Valuation Report: This is critical. Have the lowball offer from your insurance company ready, as it is the document your appraiser will directly challenge.

Organizing these basics will make the entire process smoother and faster.

Prove Your Vehicle Was in Top-Notch Condition

Now, let’s prove your car was better than the generic “comparable” vehicles the insurance company used. This is where you can significantly increase your final insurance total loss payout.

Round up any records showing you were a diligent owner.

- Detailed Service Records: Every oil change, tire rotation, and routine maintenance receipt shows your vehicle was well-cared for.

- Receipts for Recent Upgrades: Did you install new tires, brakes, a battery, or a sound system in the last year? Every receipt adds to the vehicle’s value.

- Warranty Information: Any existing or extended warranties can also increase its worth.

This paperwork paints a clear picture of a vehicle that was in excellent shape right before the accident.

Take Clear, Comprehensive Photos

Visual proof is incredibly powerful. Even after the accident, you can still document the parts of your vehicle that show how well it was maintained.

- Capture the Interior: Snap photos of the clean upholstery, the dashboard, and any custom features.

- Show the Undamaged Exterior: Photograph any parts of the car untouched by the collision to showcase its pre-accident condition.

- Highlight Special Features: Document premium wheels, a roof rack, or an upgraded stereo.

This collection of documents and photos gives an appraiser the concrete proof they need to build a powerful, data-driven report. To prepare for your negotiation, it’s a good idea to learn how to read an appraisal report so you can confidently discuss the details.

How to Negotiate With Your Insurer Using the Appraisal

Getting an expert appraisal report is a crucial step, but you still need to present it effectively. Armed with a certified, data-backed valuation, you transform from a claimant into a prepared negotiator. This is your opportunity to shift the conversation away from the insurer’s low number and toward objective facts.

The key is to remain calm, professional, and persistent. Your job is to make the adjuster pause and recognize that your claim is backed by solid evidence they cannot ignore.

Formally Submitting Your Report

First, formally present your appraisal to the insurance adjuster via email. This creates a paper trail of your communication, which can be critical later.

Your email should be polite but firm. Clearly state your position, mention the attached proof, and make a direct request for a revised settlement.

You can adapt this phrasing:

“Dear [Adjuster’s Name],

Following up on our last conversation, I’ve had an independent appraisal done to establish my vehicle’s fair market value before the loss. The report, which is attached for your review, values my vehicle at [Your Appraised Value].

This valuation is based on a detailed analysis of comparable vehicles sold in my local market. Please review the attached report and send me a revised settlement offer that reflects this evidence-based value. I look forward to resolving this matter promptly.”

This professional approach immediately shows you’ve done your homework and are serious about getting a fair insurance total loss payout.

Invoking the Appraisal Clause

What if the adjuster still pushes back? It’s time to use the “Appraisal Clause,” a provision found in most auto insurance policies that outlines a formal process for settling valuation disputes.

You don’t have to be aggressive. Just mention it calmly:

“I believe my independent appraisal provides a well-supported valuation. If we can’t agree on a fair market value, I’d like to formally invoke the Appraisal Clause in my policy to resolve this.”

Mentioning this clause signals to the adjuster that you know your rights and are prepared to escalate the matter according to your policy’s terms. They are often motivated to negotiate more seriously to avoid this formal process.

Get the Fair Settlement You Deserve

An independent appraisal is the single best tool you can bring to the negotiating table. It levels the playing field and provides the proof you need to negotiate from a position of strength.

SnapClaim provides the ammunition you need, faster than anyone else. Forget waiting weeks for a traditional appraiser. You can have a certified, data-backed report in your hands in under an hour. That speed allows you to push back against a lowball offer immediately.

Our Risk-Free Money-Back Guarantee

We are so confident in our reports that we stand behind them with a simple promise.

SnapClaim’s Money-Back Guarantee: If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee — guaranteed.

Getting an appraisal is a no-risk decision. You either achieve a significantly higher insurance total loss payout, or you don’t pay for our report. We built this guarantee because we believe you deserve expert support without any financial gamble.

An independent appraisal from a service that can help you find a total loss appraisal near me online gives you the proof you need to negotiate effectively. It’s time to stop feeling stuck and start taking control.

Frequently Asked Questions (FAQ)

Can I get an independent appraisal after my insurer makes an offer?

Yes, absolutely. In fact, that is the perfect time to get one. The insurer’s offer is just their starting point. An independent appraisal report serves as your data-backed counter-offer, providing the leverage you need to negotiate for your vehicle’s true value.

How much does a total loss appraisal cost?

The cost varies. A traditional in-person appraiser can charge several hundred dollars and take weeks. Modern online services like SnapClaim are more affordable and faster. Our certified reports are delivered in under an hour and are backed by a risk-free guarantee.

If our report doesn’t help you recover at least $1,000 more from your insurer, we refund the full appraisal fee.

What happens if my insurance company rejects my appraisal?

This is a common concern, but it’s rarely the end of the road. Most auto policies include an “Appraisal Clause” that outlines a formal process for settling valuation disputes. A high-quality report from SnapClaim is built on verifiable market data, making it difficult for an adjuster to dismiss without a valid reason. If they refuse to negotiate, you can formally invoke the appraisal clause in your policy.

How long does the appraisal process take?

With a traditional local appraiser, you could wait days or weeks. SnapClaim was designed to eliminate that delay. Our online platform allows you to upload your vehicle’s details and photos and receive a certified, data-driven total loss report in less than an hour.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes.

Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step.

Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.

👉 Get your total loss appraisal today