It’s a gut-punch feeling. The insurance company slides over a lowball offer for your vehicle, and you’re left staring at a number that feels completely wrong. You know your car was worth more, but how do you actually prove it and get a fair payout?

The answer is often hiding in your insurance policy: the appraisal clause. It’s a powerful but frequently overlooked tool that gives you the right to challenge your insurer’s valuation and force a fair, independent review of your total loss or diminished value claim.

What Is an Appraisal Clause and How Does It Help You?

An appraisal clause is a provision in most auto insurance policies that outlines a process for settling disagreements over a vehicle’s value. When you and your insurer are at a standstill, this clause lets both sides hire independent appraisers to determine the correct amount of loss.

Think of it as your contractual right to a second opinion. Instead of going back and forth with an adjuster who won’t budge, you can invoke the clause to move the dispute to neutral ground. This is essential when you’re dealing with an unfair insurance total loss payout or a low diminished value offer.

Breaking Down the Purpose of the Clause

At its core, the appraisal clause is designed to be a fair and efficient way to settle valuation disputes without ending up in court. It creates a structured path forward when negotiations have completely stalled.

Here’s how it empowers you:

- It levels the playing field. Insurance companies value cars all day. The appraisal clause lets you bring your own expert—a certified appraiser—to the table. This ensures your argument is backed by professional, data-driven analysis.

- It forces a neutral resolution. If the two appraisers can’t agree, a neutral third party, called an umpire, is brought in to make a final decision. An agreement between any two of the three parties becomes the final, binding settlement amount.

- It avoids costly litigation. This process is almost always faster and cheaper than suing your insurance company. It’s built to resolve one thing: the value of the loss, not who was at fault.

Key Takeaway: The appraisal clause isn’t an aggressive move. It’s a contractual tool designed for fair dispute resolution. Invoking it is simply exercising a right you already have in your policy to get an impartial assessment of your vehicle’s fair market value.

Understanding and using this clause is the key to getting the compensation you’re actually owed. Since regulations can influence the process, it’s a good idea to check out SnapClaim’s breakdown of total loss state laws to see how the rules apply in your area.

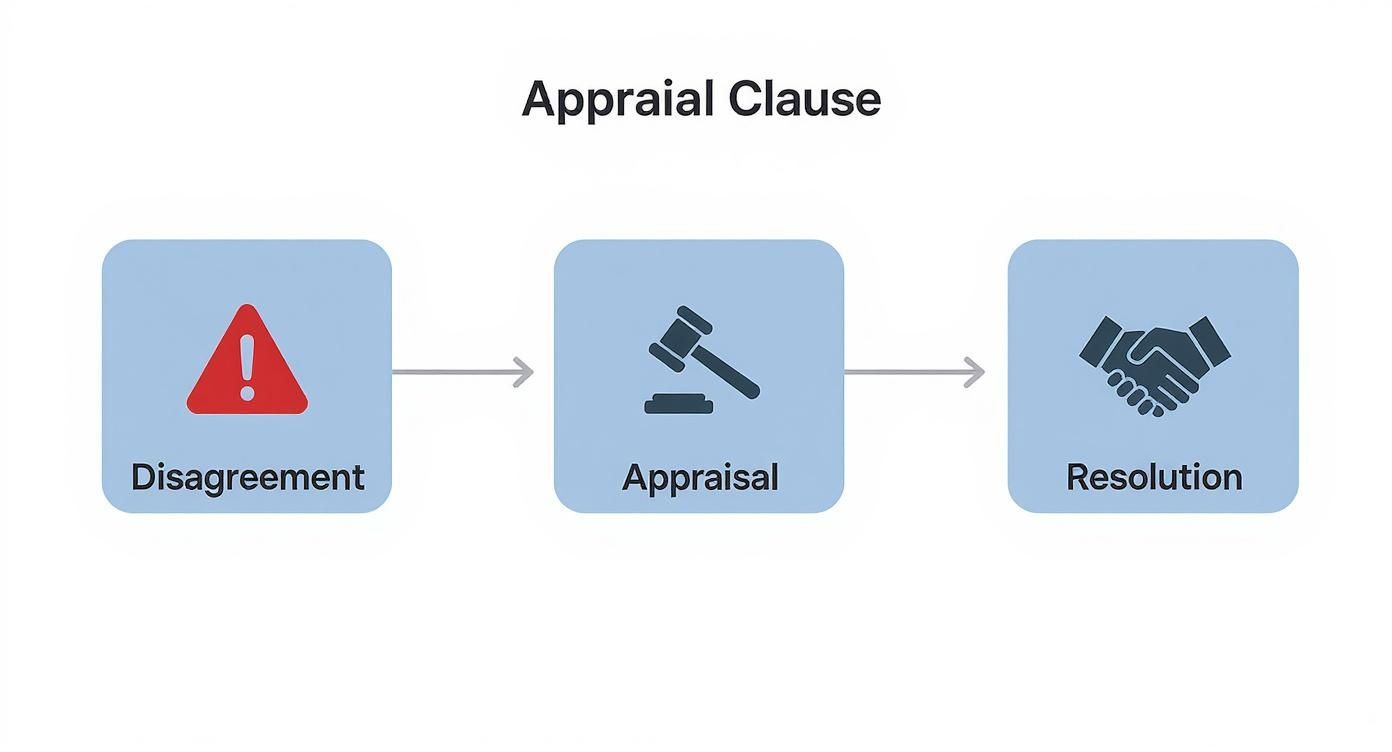

Navigating the Appraisal Clause Process Step by Step

Invoking the appraisal clause might sound complicated, but it’s a straightforward process with clear steps. When negotiations with an insurance adjuster stall, this is your policy’s built-in mechanism to get things moving again and land on a fair number.

This visual guide shows the simple flow from that initial disagreement to a final resolution.

As you can see, it’s a clear path designed to cut through the noise and get a binding answer.

Step 1: Formally Demand Appraisal in Writing

First, you have to officially kick off the process. This must be done in writing to create a paper trail.

A simple letter or email is all it takes. State that you’re disputing the Actual Cash Value (ACV) or diminished value they offered and are exercising your right to appraisal as laid out in your policy. This is also when you’ll name the independent appraiser you’ve chosen.

Step 2: Hire a Competent and Independent Appraiser

This is the most important decision you’ll make. Your appraiser is your champion in this process, so you need someone who can build a rock-solid, data-driven report that can withstand scrutiny.

Their job is to objectively determine the true value of your loss, whether that’s the pre-accident value of a totaled car or the drop in value after a repair. A flimsy appraisal report will sink your claim. SnapClaim specializes in certified appraisals built specifically for these disputes, arming you with the professional evidence you need.

Step 3: The Insurer Selects Its Appraiser

Once you’ve sent your demand and named your expert, the insurance company will hire its own appraiser to represent its valuation. Both appraisers are expected to be impartial, even though they were hired by opposing sides. Their goal isn’t to fight but to reach an agreement based on facts.

Step 4: Appraisers Work Toward an Agreement

Now, the two appraisers get to work. They’ll share their reports, compare their findings, and look at everything from data sources to final conclusions. Often, two competent professionals can find common ground and agree on a fair number, ending the process here.

The Appraisal Clause Process at a Glance

To make it even clearer, here’s a quick timeline of what to expect.

| Stage | Key Action | Typical Timeline |

|---|---|---|

| Stage 1: Demand | You send a written demand to the insurer and name your appraiser. | Day 1 |

| Stage 2: Insurer’s Response | The insurer acknowledges and names their appraiser. | Days 1-20 |

| Stage 3: Negotiation | The two appraisers share reports and work to agree on a value. | Days 20-50 |

| Stage 4: Umpire Selection | If no agreement, appraisers select a neutral umpire. | Days 50-65 |

| Stage 5: Final Decision | The umpire reviews the case and makes a binding decision. | Days 65-90 |

This structured timeline ensures the dispute moves toward a definitive conclusion.

Step 5: The Umpire Makes a Binding Decision

If the appraisers can’t agree, they must select a neutral third party called an umpire. This is usually a highly experienced appraiser with no connection to the claim.

Both appraisers present their case to the umpire, who acts as the tie-breaker. The rule is simple: an agreement by any two of the three parties becomes the final, binding settlement amount. Once that number is set, the debate is over, and the insurance company is obligated to pay.

Knowing When to Invoke Your Appraisal Clause

The appraisal clause is your best tool when negotiations with an insurance company have hit a dead end. But what does that really mean? Knowing the right moment to use it is key to protecting yourself financially after an accident.

Invoking the clause is the logical next step to break a stalemate and force a fair, impartial resolution. Most of these disputes happen in two classic scenarios: arguments over a total loss settlement or a diminished value claim.

The Total Loss Dispute Impasse

This is the most common reason to use your appraisal clause. A total loss dispute begins when your vehicle is totaled, but the insurer’s Actual Cash Value (ACV) offer is far too low compared to what your car was worth before the crash.

You know your well-maintained, low-mileage truck was worth more than the $18,000 they offered. You’ve sent them comparable listings, but the adjuster won’t budge. That is an impasse.

It’s probably time to invoke your appraisal clause when:

- The insurer uses poor “comps.” They might base their offer on vehicles in worse condition, with higher mileage, or missing the premium package your car had.

- They ignore recent upgrades. Did you just add new tires or a high-end sound system? The insurance company’s automated valuation tool almost certainly missed it.

- The offer is well below market value. If your research on reputable sites like Kelley Blue Book shows a huge gap between their number and reality, it’s time for a formal appraisal.

In these situations, invoking the clause takes the decision away from the insurer and puts it into a structured, unbiased process where facts determine the outcome.

The Diminished Value Claim Stalemate

The second trigger is a standoff over your diminished value claim. This is the loss in resale value your car suffers even after perfect repairs. That accident is now a permanent part of its history, and buyers won’t pay top dollar for it.

Many insurers will offer a tiny amount or deny the claim outright, hoping you’ll give up.

Scenario: Your luxury SUV gets rear-ended, causing $12,000 in damage. The body shop does a fantastic job, but its vehicle history report now has a black mark. You file a diminished value claim for the $6,500 loss in resale value. The insurer’s response? An offer of $800.

That’s not a negotiation—it’s a dismissal. When the gap is that wide, the appraisal clause is your most powerful tool. A professional appraiser can provide the certified, data-driven report needed to prove the true car value after an accident and compel a fair settlement.

Understanding the Financial Power of the Appraisal Clause

The appraisal clause is more than just a procedural step—it’s one of the strongest consumer protection tools in your policy. It provides a formal way to challenge an insurer’s valuation and fight back against a lowball offer on your total loss or diminished value claim.

In the real world, it can be the difference between accepting a disappointing payout and recovering the thousands of dollars you’re actually owed. Think of it as an investment in fairness.

A Small Investment for a Major Return

Many vehicle owners hesitate to use the appraisal clause because it means paying for their own appraiser. But it’s crucial to see this as a strategic investment. A small fee for a certified report can stop you from losing thousands on an undervalued insurance total loss payout.

Let’s say an insurer offers you $15,000 for your totaled car, but its true market value is closer to $19,000. By investing in a professional appraisal, you get the proof needed to close that $4,000 gap. The return on investment becomes obvious.

How the Numbers Prove Its Worth

The financial power of the appraisal clause isn’t just a theory; it’s backed by data. Insurance companies often lean on automated valuation systems that are notorious for undervaluing vehicles.

A deep dive into 46 appraisal clause outcomes in Texas showed that insurers’ initial offers were, on average, wrong by about 45.86% compared to the final appraisal award. That means customers were initially shorted by an average of $5,312.46 per claim.

Without the appraisal process, those vehicle owners would have lost significant compensation. The clause is the mechanism that corrects these errors and gets you the money you deserve.

Sharing the Costs of the Process

The appraisal clause manages costs fairly, which makes it a smart financial move. Here’s how it usually breaks down:

- You pay for your appraiser: This is your hand-picked expert.

- The insurer pays for its appraiser: They cover their expert’s fee.

- You both split the umpire’s fee: If an umpire is needed to break a tie, you and the insurance company share that cost 50/50.

This cost-sharing setup ensures neither side is unfairly burdened. Understanding the cost of a car appraisal is a great first step, and the potential to recover thousands more often makes it a no-brainer.

If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee — guaranteed. This takes the financial risk off the table, so you can challenge a lowball offer with total confidence.

How State Rules and Policy Language Can Differ

While the appraisal clause is a standard feature in most auto policies, the specifics—how it works and when you can use it—can change based on your state and the exact wording in your policy.

Insurance is not a one-size-fits-all product. Some states have strong consumer protection laws that define how the appraisal process works, while others give insurance companies more leeway.

The First Step: Read Your Policy

Before invoking the appraisal clause, pull out your insurance policy and read it. That document is your contract with the insurer, and the fine print matters. Look for a section titled “Appraisal” or “Mediation” to find the language that outlines your rights and the steps for handling a value dispute.

Pay close attention to these details:

- Timelines: Are there strict deadlines for demanding an appraisal?

- Binding Nature: Does the clause say the outcome is final and binding?

- Specific Conditions: Are there any unique requirements you have to meet?

This language is your game plan. Ignoring it could jeopardize your ability to challenge an unfair insurance total loss payout.

State Laws Can Change the Game

On top of your policy, state laws can add another layer of rules. Some states have passed laws that make the appraisal process more transparent and fair for policyholders.

For example, the Texas Department of Insurance (TDI) recently drafted new rules requiring personal auto policies to include a binding appraisal provision and creating a clear 120-day window to demand an appraisal. This is a huge step toward creating clear, fair guidelines.

Having a general grasp of understanding insurance compliance helps you see the bigger picture and advocate for yourself more effectively. Because laws are always evolving, it’s smart to check your state’s specific regulations on insurance disputes.

Why a Certified Appraisal Is Your Strongest Asset

When you invoke the appraisal clause, you’re entering a formal dispute. Winning comes down to one thing: credible evidence. An emotional argument or a handful of online car listings won’t work. This is where a professional, data-driven appraisal report becomes your most powerful tool.

Your opinion of your car’s value is just that—an opinion. But a certified appraisal from a company like SnapClaim is defensible proof, built to withstand scrutiny from insurance companies.

The Difference Between Opinion and Evidence

Insurance carriers love their automated valuation tools because they’re fast and cheap, but they often miss the mark. These systems rely on generic data and can’t account for your vehicle’s specific condition, upgrades, or local market.

A SnapClaim report is built from the ground up with detailed market analysis and precise condition adjustments. Our certified methodology considers every factor that gives your vehicle its true value.

- Real Market Data: We pull real-time sales data from your specific area, finding genuinely comparable vehicles.

- Detailed Condition Adjustments: We factor in your vehicle’s mileage, options, and overall condition.

- A Defensible Methodology: Our reports are designed to be clear and logical, with every conclusion backed by verifiable data.

This completely reframes your argument. You’re no longer saying, “I think my car is worth more.” You’re declaring, “Here is the certified proof of my car’s value, supported by extensive market data.”

From Claimant to Informed Negotiator

Handing over a certified appraisal report immediately changes the dynamic. You’re no longer just a claimant asking for more money; you’re an informed party presenting credible, third-party evidence that the insurer’s offer is wrong.

A well-built report makes it much harder for an adjuster to dismiss your claim. It forces them to address the specific facts and data you’ve presented. The conversation shifts toward a fair resolution based on evidence, not their initial lowball offer.

Key Takeaway: An independent appraisal is the single most effective tool for challenging a lowball insurance offer. It provides the objective, data-driven proof you need to make your case undeniable and ensure the appraisal clause process works in your favor.

Frequently Asked Questions (FAQ)

Does using the appraisal clause mean I’m suing my insurer?

Not at all. The appraisal clause is a cooperative tool built into your policy to settle disagreements over value without going to court. Think of it as triggering a formal negotiation, not a legal battle.

Can my insurance company refuse to participate in an appraisal?

If the appraisal clause is in your policy, they are contractually obligated to participate once you make a formal demand. Refusing could put them in breach of contract. They can only refuse if the dispute is about coverage (whether the damage is covered) and not about the dollar amount of the loss.

What if the two appraisers can’t agree on a value?

This is what the neutral umpire is for. If the appraisers can’t agree, they present their findings to the umpire, who acts as the tie-breaker. An agreement between any two of the three parties becomes the final, binding settlement amount.

Is the cost of an appraisal really worth it?

For most people, yes. While you pay for your own appraiser, the potential return can be huge, as initial insurance offers are often thousands of dollars too low. SnapClaim’s Money-Back Guarantee takes the risk out of the equation. If your final insurance recovery from the claim is less than $1,000, we refund our fee, allowing you to challenge an unfair payout with peace of mind.

Get your free estimate today or order a certified appraisal report to strengthen your insurance claim.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes.

Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step.

Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.

👉 Get your free fair market value estimate today