If you’re trying to learn how to file a diminished value claim with USAA, the process is different from what many drivers expect because USAA does not provide a specific claim form.

Has your vehicle been in an accident? You’re likely searching for a “USAA diminished value claim form,” but the truth is, a specific form for this doesn’t exist. Your diminished value claim is handled as part of the standard property damage process, which means you need to know how to present your case from the start.

This guide will walk you through the exact steps to build and file a successful claim with USAA. We’ll show you how to provide the evidence needed to recover your car’s lost value after repairs.

Your First Moves After a Car Accident

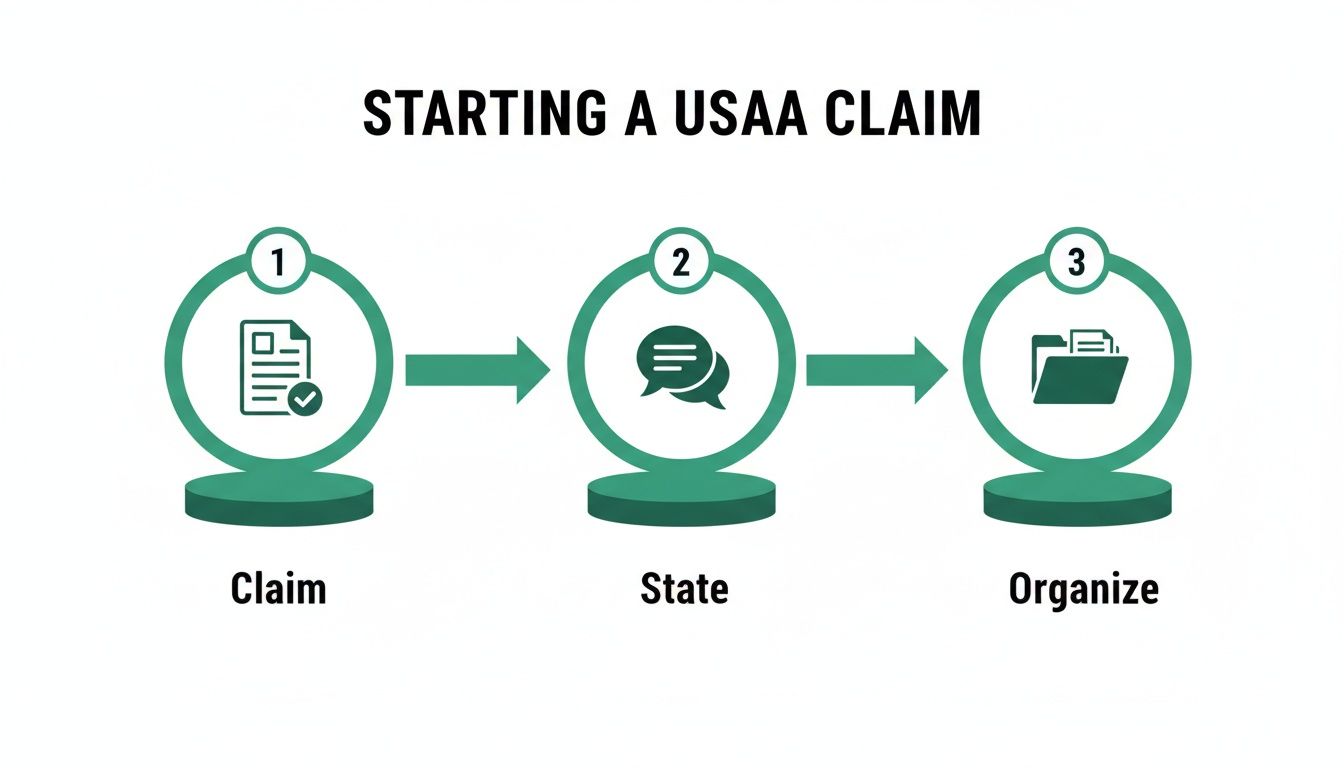

Getting the first few steps right is critical. This process isn’t about finding a secret form; it’s about officially opening your claim and making it clear that you are seeking compensation for your car’s diminished value. Doing this sets the stage for a stronger negotiation.

First, open a standard auto claim with USAA online or by phone. During that initial conversation or in your online submission, you must be direct. Simply expressing frustration about the accident won’t be enough. You need to state your intent to pursue a diminished value claim formally.

Stating Your Intent Clearly

When you speak with the adjuster, use simple, direct language. A statement like this works perfectly:

“In addition to the repair costs, I am formally requesting compensation for my vehicle’s inherent diminished value resulting from this accident. I will be providing a certified appraisal to document this loss.”

This single sentence puts your request officially on the record. It tells the adjuster that you understand your rights and plan to back up your claim with professional evidence. If you’re new to the concept, our guide on what a diminished value claim is is a great place to start.

The Importance of Early Organization

From day one, organization is your best friend. Get a folder—digital or physical—and save every document related to the accident and your claim. This prep work will save you from searching for paperwork later and sends a clear message to the insurer: you are serious and organized.

This simple flowchart breaks down those critical first actions.

It boils down to three key steps: open the claim, state your intent, and organize your documents.

Here are the key documents you should gather right away:

- The Police Accident Report: This is the official record that establishes what happened and who was at fault.

- Photos of the Damage: Take detailed pictures from every angle before any repairs are made.

- The Other Driver’s Information: A quick photo of their insurance card and driver’s license is ideal.

Having these items on hand before the first repair estimate arrives puts you in control. It elevates your claim from a simple request to a well-documented case, showing the adjuster you are prepared to prove your vehicle’s financial loss.

How USAA Calculates Diminished Value

Ever wonder why the first diminished value offer from an insurer seems so low? It’s not a random number. When you file a claim with USAA, their response is the product of a standardized internal formula designed to minimize their payout.

Understanding how their system works is the first step to challenging it. Their initial offer isn’t the final word—it’s just a starting point. Knowing this gives you the power to counter their automated assessment with real-world proof of what your vehicle is now worth.

The 17c Formula Explained

Like many insurers, USAA often relies on a calculation known as the “17c formula” or a similar method from a third-party vendor. This formula is designed to standardize payouts but often ignores the real market dynamics for a specific, accident-damaged vehicle.

The process starts by immediately capping your potential recovery.

The formula typically sets a hard ceiling on your claim, capping the base loss at just 10% of your vehicle’s pre-accident value.

So, if your car was worth $40,000 before the wreck, their formula automatically limits the maximum possible diminished value to $4,000. And that’s before they apply additional deductions.

How Modifiers Reduce the Payout

Once that initial cap is set, the formula applies a series of “modifiers” to reduce the payout further. These deductions account for your car’s specific details and the damage it sustained.

The two biggest modifiers they use are:

- Damage Modifier: This adjusts the amount based on the severity of the damage. Minor cosmetic issues will result in a larger reduction than serious structural or frame damage.

- Mileage Modifier: Your car’s odometer reading is used to cut the payout again. A car with 100,000 miles will see a much steeper deduction than one with only 20,000 miles.

This cookie-cutter math rarely reflects reality. The final number they offer is based on their internal calculations, not on how an actual buyer in the used car market will view a vehicle with an accident on its CARFAX report. To get a better handle on the legal foundation of your claim, it’s worth reading a comprehensive guide to diminished value claims from legal experts.

Why Their Formula Falls Short

USAA often sends diminished value claims to third-party services that apply these boilerplate formulas. The 17c method, for example, is notorious for capping the base diminished value before any other deductions are even applied.

A car’s true loss in value isn’t decided by an insurance company’s spreadsheet. It’s determined by what a real buyer is willing to pay. That gap between their formula and the free market is where your negotiation power lies. You can get a much clearer picture of what you’re really owed when you calculate your diminished value using real market data.

Building a Claim USAA Can’t Ignore

Knowing USAA’s formulaic approach is one thing; overpowering it with undeniable proof is another. This is where you flip the script and force the negotiation onto your terms.

Building a powerful evidence package is about constructing a clear, logical narrative that proves your vehicle’s real-world market loss. An adjuster’s internal formula simply can’t stand up against organized, factual evidence.

Your goal is to present a professional demand backed by proof so solid they can’t dismiss it. This turns your request into a formal, documented case for compensation.

Your Essential USAA Claim Document Checklist

Before writing a demand letter, you need to gather the documents that will form the bedrock of your claim. Each piece of paper tells a part of the story, from the moment of impact to the final repairs.

Here’s a quick look at the documents you absolutely need.

| Document | Why It’s Critical | How to Obtain It |

|---|---|---|

| Official Police Report | Establishes the core facts of the incident, especially fault, which is crucial for a third-party claim. | Request a copy from the law enforcement agency that responded to the accident. |

| Pre- & Post-Repair Photos | Detailed photos of the initial damage prove the severity. Photos of the finished repairs show the cosmetic fix doesn’t erase the value loss. | Take them yourself immediately after the accident and once repairs are done. The body shop may also provide them. |

| Final Itemized Repair Invoice | This is a permanent, discoverable record of the collision for future buyers. It lists every part replaced and every hour of labor. | The auto body shop provides this once all repairs are completed and paid for. |

Having a solid grasp of repair costs also helps contextualize the damage. For instance, understanding specific repair costs like side mirrors can help illustrate how even seemingly minor repairs contribute to the vehicle’s permanent negative history.

These documents set the stage, but one final piece elevates your claim from standard to authoritative.

The Cornerstone of Your Claim: The Appraisal Report

While the documents above prove an accident happened and was repaired, they don’t quantify the financial loss. This is why the absolute cornerstone of your entire diminished value claim is a certified, independent appraisal report.

An insurer’s internal valuation is designed to protect its own bottom line. An independent appraisal from a trusted source like SnapClaim provides an unbiased, data-backed assessment that forces the negotiation onto neutral ground.

A certified report isn’t just an opinion; it’s professional evidence. It analyzes your specific vehicle, the nature of the repairs, and real-time market data to calculate the precise loss in value.

When you present this to the USAA adjuster, the conversation changes. You are no longer debating their lowball formula; you are discussing market facts. This simple act shifts the burden of proof. The adjuster must now find credible data to refute the findings in your certified report. It’s the most effective step you can take to strengthen your claim submission and level the playing field.

Navigating Pushback and Negotiating with USAA

Don’t be surprised if USAA’s first diminished value offer is low. This isn’t a rejection—it’s the opening move in a negotiation. Your preparation and professional appraisal have put you in a position to respond with facts, not frustration.

Remember, the adjuster’s goal is to close your claim quickly while minimizing the payout. They often lean on common arguments to downplay your claim. By knowing what to expect, you can prepare clear, evidence-based rebuttals that keep the conversation moving forward.

Common Objections and How to Respond

Anticipating the adjuster’s script lets you control the narrative. Your certified appraisal report from SnapClaim is your anchor. No matter what they say, always steer the conversation back to its market-driven data.

Here are three frequent arguments you’ll hear and how to respond:

- “Our high-quality repairs restored your vehicle’s full value.”

- Your Response: “I appreciate the quality of the repairs, but they cannot erase the vehicle’s accident history. A legally discoverable accident record permanently lowers its market value, which is what my professional appraisal documents.”

- “We don’t cover diminished value in your state.”

- Your Response: “Third-party diminished value is a recognized form of property damage in my state. The law requires me to provide proof of loss, which my certified appraisal establishes with verifiable market data.”

- “Your appraisal amount seems too high.”

- Your Response: “The figure in my report is based on an analysis of comparable vehicle sales and dealer quotes in our local market. Could you provide a detailed breakdown showing how your offer was calculated so we can compare the data?”

That last point is a power move. When you ask for their data, you shift the burden of proof back to them. You are forcing the adjuster to defend their low number against your comprehensive, market-based evidence.

Sticking to the Facts

Throughout every conversation, stay professional and persistent. Emotional arguments won’t get you anywhere; documented facts will. Reference specific pages in your appraisal, point to line items on the repair bill, and connect those dots to the car value after an accident.

Key Takeaway: The goal is to make it clear that your claim isn’t just an opinion—it’s a documented financial loss. Your polite insistence on discussing the evidence makes it difficult for an adjuster to dismiss your position.

In one well-documented case, a driver’s initial USAA offer of just $417 was raised to $6,000 after they presented an independent appraisal—a 1,300% increase. This shows how dramatically a data-backed report can shift the negotiation. You can discover more about how this driver successfully negotiated.

Your certified appraisal provides the proof you need to negotiate fairly. By consistently redirecting the conversation back to this evidence, you transform a potential dismissal into a fact-based negotiation.

Advanced Strategies When Negotiations Stall

You’ve presented your evidence and certified appraisal, but the adjuster still won’t offer a fair settlement. This is a frustrating but common part of the process. This is where many people give up, but it’s actually where you have the most leverage.

When initial talks hit a dead end, it’s time to escalate. You have clear, powerful options to enforce your right to be made whole.

An insurer’s business model often relies on policyholders getting tired and walking away. Having a game plan for your next move signals that you’re serious about getting the full value you’re owed.

Invoke the Appraisal Clause

One of the most powerful tools in your insurance policy is the appraisal clause. It’s often overlooked but can be a game-changer when you and the insurer disagree on the amount of your loss.

Here’s how it works: you formally invoke the clause, and then both you and USAA hire certified appraisers. Those two appraisers select a third, neutral appraiser to serve as an “umpire.” A decision agreed upon by any two of the three becomes binding.

This move takes the decision out of the adjuster’s hands and gives it to impartial experts. It forces a resolution based on professional evaluations, not stonewalling tactics. We have a detailed guide that shows you exactly how to invoke the appraisal clause.

File a Formal Complaint with the State

If negotiations and the appraisal clause don’t produce a fair result, your next step is filing a complaint with your state’s Department of Insurance (DOI). This regulatory agency oversees insurance companies to ensure they comply with state laws.

The DOI will review your case, including your documentation and the insurer’s responses. While they can’t force a specific payout, an official inquiry often motivates an insurer to reconsider its position and make a more reasonable offer.

Know When to Bring in an Attorney

If USAA continues to act in bad faith or refuses to negotiate, it might be time to consult an attorney specializing in insurance claims. A lawyer can take over communication, apply legal pressure, and file a lawsuit if necessary. This becomes especially important if your claim is for a significant amount.

A certified SnapClaim report is vital for these advanced strategies. It gives you the professional evidence needed to win an appraisal dispute, a DOI complaint, or a legal action. And with our Money-Back Guarantee, if your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee.

Frequently Asked Questions (FAQ)

Can I claim diminished value if the accident wasn’t my fault?

Yes. Diminished value is almost always a third-party claim. This means you file it against the insurance policy of the at-fault driver. Your own collision coverage is designed to repair your car, not to compensate you for the market value it loses after it’s repaired. The responsible driver’s insurance is obligated to make you financially whole, which includes the loss in your car’s resale value.

How long do I have to file my diminished value claim with USAA?

Every state has a deadline for filing property damage claims, known as the statute of limitations. These time limits typically range from two to six years from the date of the accident. However, waiting is a mistake. The best time to file your diminished value claim is right after your vehicle’s repairs are completed, when all evidence is fresh and relevant.

Will filing a diminished value claim make my insurance rates go up?

Filing a third-party claim against the other driver’s USAA policy should not affect your own insurance rates. Rate increases are generally linked to at-fault accidents where you file a claim under your own policy. You are legally entitled to recover the loss in value caused by another party’s negligence.

What if the adjuster says my state doesn’t allow diminished value claims?

This is a common pushback tactic. The truth is, nearly every state allows you to make a third-party claim for diminished value. When an adjuster says this, they are shifting the burden of proof back to you. This is why an independent appraisal is essential. A SnapClaim report provides the objective, market-driven evidence needed to prove your financial loss and counter this common objection.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes.

Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step.

Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.

👉 Get your free estimate today or order a certified appraisal report!