Dealing with an insurance company after an accident can be frustrating, especially when their settlement offer feels insultingly low. An independent car appraisal is a professional, unbiased valuation of your vehicle’s true worth, conducted by a certified expert who isn’t on the insurance company’s payroll. It provides the data-backed proof you need to negotiate a fair settlement.

Why You Need an Independent Car Appraisal

After an accident, the insurance company’s settlement offer finally hits your inbox, but the number just doesn’t seem right. This common scenario leaves you wondering how you’ll cover the financial gap.

This is exactly where an independent car appraisal becomes your most powerful tool. It’s a fair, data-driven valuation of your vehicle’s real-world worth, conducted by a professional with no ties to your insurance company.

Uncovering Your Vehicle’s True Value

An insurer’s assessment often comes from automated systems programmed to find the lowest possible value. An independent appraisal, on the other hand, considers your car’s unique story.

A professional appraiser establishes its true Fair Market Value (FMV)—what a real buyer would have paid for it right before the accident. They look at specific details that automated systems often miss.

- Specific Condition: Was your car perfectly maintained with low mileage and a flawless interior? A professional appraisal accounts for that.

- Recent Upgrades: That new sound system, custom wheels, or premium trim package all add value that an insurer’s algorithm is likely to ignore.

- Local Market Data: The appraiser analyzes comparable sales in your specific area, not from a generic national database, to get an accurate picture of your car’s local value.

The Foundation for Your Claim

This impartial report is the bedrock for two critical types of claims. It’s essential for a diminished value claim, which covers the loss in your car’s resale value after it’s been repaired. Even a perfectly fixed car is worth less simply because it has an accident on its record.

It’s also your best defense when disputing a low insurance total loss payout. If your vehicle is declared a total loss, the appraisal provides the proof you need to show its true pre-accident replacement cost. This helps ensure you get a check large enough to buy a comparable replacement vehicle.

Ultimately, an independent car appraisal provides the concrete evidence you need to negotiate for the full compensation you rightfully deserve.

Why Your Insurer’s Valuation Is Often Too Low

When an insurance company’s settlement offer seems too low, you’re not imagining things. You and your insurer have opposite goals: their job is to protect their bottom line, while your goal is to be made whole again. This conflict of interest is at the heart of nearly every lowball offer.

To justify their numbers, insurers lean heavily on automated valuation software. These platforms are built for speed and volume, not for the precision needed to determine a vehicle’s true fair market value.

The Problem with Automated Valuations

These software platforms can produce reports riddled with errors that conveniently work in the insurance company’s favor.

Here’s what typically goes wrong:

- Stale Sales Data: The software might pull “comparable” cars that sold months ago, missing recent market shifts that drove your car’s value up.

- Ignored Features: That premium sound system or brand-new tires you just put on are often overlooked by automated systems.

- Excellent Condition Overlooked: If your car was garage-kept and in pristine condition, a generic report will never capture that above-average value.

- Incorrect Comparisons: Reports might use “comparable” vehicles from a different state or misclassify your premium trim level as a base model to justify a lower number.

An insurer’s valuation is just their opinion of what they owe you. An independent car appraisal is a statement of fact about what your car was actually worth, backed by real-world market evidence.

An independent appraisal from SnapClaim cuts through the noise. It replaces the insurer’s biased, computer-generated number with a solid, defensible report grounded in real-time, local market data. It helps you negotiate a fair insurance total loss payout or prove your diminished value claim, leveling the playing field so the final settlement reflects your car’s true value.

Appraisals for Diminished Value vs. Total Loss Claims

An independent car appraisal is your best weapon in two frustrating post-accident scenarios: getting paid for diminished value or fighting a lowball total loss settlement.

While both situations are about proving what your car is really worth, they tackle different kinds of financial losses. Knowing which one you’re facing is the first step toward getting the compensation you’re owed. A professional appraisal from SnapClaim provides the cold, hard data needed to strengthen your claim.

Proving Diminished Value After an Accident

Diminished value is the drop in your car’s resale value after an accident, even if repairs are perfect. Why? Because a car with an accident history is worth less to the next buyer. No one wants to pay top dollar for a vehicle that’s been in a wreck.

Think about it: if you’re looking at two identical used cars, but one has a collision on its vehicle history report, you’d demand a serious discount. That price difference is the diminished value, and you have a right to be compensated for it. An independent appraisal is the only way to prove this “car value after accident” and force the insurer to take it seriously. Our Diminished Value Guide explains this concept in more detail.

Securing a Fair Total Loss Payout

An insurer declares a vehicle a “total loss” when the cost to fix it is more than its Actual Cash Value (ACV) before the crash. Instead of paying for repairs, they write you a check for what they claim your car was worth.

The problem is their number is almost always too low. They might offer you $15,000 for a car that would actually cost $19,000 to replace. A proper independent car appraisal corrects the record by establishing your vehicle’s true pre-accident replacement cost. Learn more in our Total Loss Guide.

In both cases, the goal of an appraisal is the same: to replace the insurer’s lowball opinion with an objective, market-based valuation backed by verifiable proof.

Here’s a simple breakdown of how an appraisal works for each claim type.

Diminished Value vs. Total Loss Appraisals

| Appraisal Focus | Diminished Value Claim | Total Loss Claim |

|---|---|---|

| Goal | Recover lost resale value on a repaired vehicle. | Secure a fair payout for a vehicle that won’t be repaired. |

| Valuation Point | Calculates the difference in value before the accident and after repairs. | Determines the vehicle’s full market value right before the accident. |

| Evidence Used | Repair quality, accident severity, market stigma, comparable sales data. | Pre-accident condition, mileage, options, and comparable vehicle listings. |

| Common Scenario | Your car is fixed and drivable, but its history report now shows an accident. | The cost of repairs exceeds the vehicle’s worth, so the insurer wants to “buy” it from you. |

Ultimately, whether you’re fighting for lost value or a total loss, you need an independent voice to establish the facts.

Navigating the Appraisal Clause

If you and the insurer can’t agree on the value, your insurance policy likely contains an “appraisal clause.” This provision gives both you and the insurer the right to hire your own independent appraisers to settle the dispute. Invoking this powerful contractual right can be the key to forcing a fair negotiation.

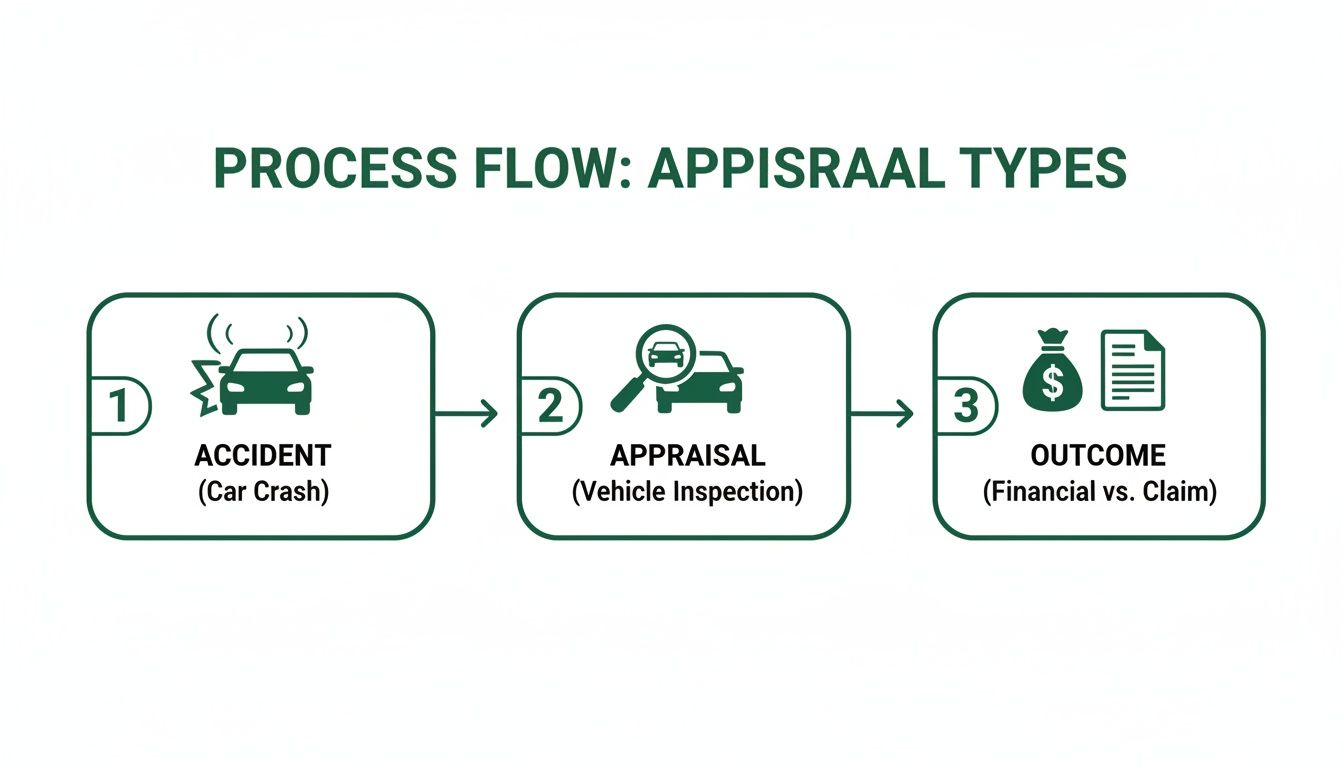

How the Independent Appraisal Process Works

So, you received an insurance settlement offer that feels too low. What’s next? Getting an independent car appraisal is more straightforward than you might think.

First, gather all your paperwork. This includes the police report, repair estimates, maintenance records, and any receipts for recent work, like new tires. This information gives your appraiser the ammunition they need to build the strongest possible case for your car’s actual value.

Once your documents are organized, it’s time to find a reputable, certified appraiser.

Choosing an Appraiser and Submitting Your Report

A qualified appraiser performs a deep dive into your car, either through a physical inspection or by analyzing detailed photos and your documentation. They look at your car’s specific condition, its unique features, and what similar cars are actually selling for in your local market.

The result is a comprehensive valuation report. This isn’t just an opinion—it’s an evidence-backed document that proves your car value after accident and strengthens your claim.

This process highlights how the appraisal becomes the central action that drives a fair outcome for your claim.

Using Your Report to Negotiate

With your certified report in hand, submit it to the insurance adjuster. This report becomes the foundation of your negotiation, replacing the insurer’s automated number with concrete proof of your vehicle’s actual worth.

Suddenly, the conversation shifts. It’s no longer just your word against theirs; it’s a dispute backed by hard data. This gives you the leverage you need to secure a better settlement for a diminished value claim or an insurance total loss payout.

The used car market is incredibly active, valued at USD 1,148.63 billion in 2023 and expected to grow. You can dive deeper into these trends at Maximize Market Research. This fast-moving market is why a professional independent car appraisal, grounded in current analysis, is so critical for a fair negotiation.

Strengthen Your Claim with a Certified Report

An independent car appraisal is more than a second opinion—it’s the most powerful piece of evidence you can have. A certified report from SnapClaim transforms your claim from a simple disagreement into a professional, data-backed dispute that an insurance company cannot easily ignore.

This isn’t about saying your car is worth more. It’s about proving it with a defensible document built on solid market analysis and strict industry standards.

The Anatomy of a Defensible Report

For an appraisal to be effective, it must be credible and built on verifiable data. At SnapClaim, we craft every report to meet that high standard.

Here’s what goes into it:

- Comprehensive Market Analysis: We analyze multiple valuation sources, including Kelley Blue Book and NADAguides, and cross-reference them with real-time local market data to lock down a true Fair Market Value.

- Adherence to USPAP: Our entire process follows the Uniform Standards of Professional Appraisal Practice (USPAP), the nationally recognized ethical and performance standards for the appraisal profession.

- Expert Review: Every SnapClaim report is reviewed and signed by professionals holding I-CAR and ASE certifications, ensuring the highest level of accuracy.

This rigorous approach means your report is a powerful piece of evidence that will stand up to scrutiny from adjusters, arbitrators, and even in a courtroom.

Turning a Disagreement into a Data-Backed Dispute

When you submit a certified independent car appraisal, you completely change the dynamic of the negotiation. Instead of being on the defensive, you’re presenting a credible case that the insurer is obligated to seriously consider.

The used car market is massive and complex, valued at around USD 1.67 trillion in 2023. As it keeps growing, the need for professional, data-driven valuations becomes even more critical for settling insurance claims fairly. You can read more on these market trends from Fortune Business Insights.

A SnapClaim report uses this hard market data to give you a real advantage. We’re so confident in our certified methodology that we offer a risk-free way to challenge your insurer’s lowball offer.

SnapClaim’s Money-Back Guarantee: If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee — guaranteed.

This guarantee takes the financial risk out of the equation, giving you the peace of mind to fight for what you’re rightfully owed. With a certified report, you’re not just asking for more money; you’re proving you deserve it.

Take Control with an Independent Car Appraisal

An independent car appraisal is the single most powerful tool you have to get a fair payout after an accident. It’s your equalizer against an insurer’s lowball offer, providing factual, market-based evidence they can’t ignore.

This certified report proves your actual losses, whether you’re fighting for a diminished value claim or a total loss payout. With a SnapClaim report, you are no longer just arguing with their number; you are negotiating from a position of strength. Don’t leave thousands of dollars on the table.

SnapClaim makes this entire process straightforward and risk-free.

👉 Get your free estimate today or order a certified appraisal report to strengthen your insurance claim.

Frequently Asked Questions (FAQ)

Here are answers to common questions vehicle owners have about getting an independent car appraisal.

Can I claim diminished value if the accident wasn’t my fault?

Yes, absolutely. In most states, you are entitled to file a diminished value claim against the at-fault driver’s insurance policy. An independent appraisal provides the necessary proof of your vehicle’s lost resale value. Your right to fair compensation is not affected by who caused the accident.

How much does an independent car appraisal cost?

Think of a certified appraisal as a small investment to avoid leaving thousands on the table. While fees can vary, a high-quality, data-driven report from SnapClaim provides the leverage you need to negotiate a higher payout. The average SnapClaim user sees a recovery of over $6,000, making the report a highly worthwhile tool.

What if the insurer rejects my appraisal report?

This is a common insurance tactic. If they refuse to consider your report, politely ask for their reason in writing. A credible report from a service like SnapClaim is built on verifiable market data and industry standards, making it difficult for them to justify dismissing it. If they still won’t negotiate, it may be time to formally invoke your policy’s Appraisal Clause.

How long does the appraisal process take?

The timeline can vary, but modern appraisal services have made the process incredibly quick. With SnapClaim, you can often get a certified, defensible report in about an hour. That speed is critical—it lets you push back against the insurer’s low offer right away, keeping your claim moving forward without frustrating delays.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes.

Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step.

Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.

👉 Get your total loss appraisal today