After a car accident, you know your vehicle isn’t worth what it used to be, even after perfect repairs. A USAA diminished value claim is your way to recover this loss in resale value when a USAA-insured driver was at fault. This guide explains how to build a strong case and negotiate for the compensation you deserve.

Understanding Your USAA Diminished Value Claim

When another driver damages your vehicle, its market value drops permanently. It doesn’t matter how excellent the repairs are; a car with an accident history is worth less to a potential buyer. That financial loss is called diminished value, and you have the right to claim it.

Filing a diminished value claim with USAA is the process of formally requesting compensation for that loss. This is separate from the money paid for repairs. It is entirely focused on the resale value your car lost after the repairs were completed.

The Different Types of Diminished Value

To build a solid case, it helps to understand the specific type of loss you’ve suffered. Diminished value typically falls into three categories:

- Inherent Diminished Value: This is the most common type and the focus of most claims. It’s the automatic loss in value a car suffers simply because it now has an accident on its vehicle history report. Even with flawless repairs, the stigma of a collision makes buyers wary.

- Repair-Related Diminished Value: This applies when the repairs are subpar. Examples include mismatched paint, the use of cheap aftermarket parts, or new rattles that weren’t present before the accident.

- Immediate Diminished Value: This is the difference between your car’s pre-accident value and its value immediately after the accident, before any repairs are made. This is not typically what you claim from an insurer.

For nearly every USAA diminished value claim, your focus will be on inherent diminished value. You are seeking compensation for the negative stigma now attached to your car’s VIN, which directly lowers its fair market value.

Are You Eligible to File a Claim?

Not every accident qualifies for a diminished value claim. Eligibility depends on who was at fault and the laws in your state. Before investing time and effort, confirm that you meet the core requirements.

Here’s a quick checklist to see if you can file a diminished value claim against a USAA policyholder.

USAA Diminished Value Claim Eligibility Checklist

| Requirement | Do You Qualify? | Why It Matters |

|---|---|---|

| The Other Driver Was At Fault | ✅ | You can only file a third-party claim against the at-fault driver’s insurance—in this case, USAA. |

| You Are Not At Fault | ✅ | You generally cannot claim diminished value against your own policy (a first-party claim). |

| Your Vehicle Was Repaired | ✅ | The claim is for the lost value after repairs. A vehicle declared a total loss does not qualify. |

| You Own the Vehicle | ✅ | You must hold the title. If you lease, the leasing company is the party that suffers the financial loss. |

If you checked all these boxes, you are likely in a good position to proceed.

Understanding these fundamentals is crucial. To learn more, read our complete guide on what a diminished value claim is and how the process works. This background knowledge will be your best asset when speaking with an insurance adjuster.

Why USAA’s First Offer Is Only a Starting Point

When USAA’s settlement offer for your USAA diminished value claim arrives, you might feel relieved. However, it’s wise to pause before accepting. This initial figure is almost always an opening bid, not a final settlement.

Insurance adjusters are tasked with closing claims as quickly and inexpensively as possible. Their first offer is not a true reflection of your vehicle’s lost market value; it’s a starting point for negotiation, calculated to protect their company’s bottom line.

Decoding the 17c Formula

Where does that low number come from? In most cases, it’s the result of a calculation known as the “17c formula.” This method originated from a Georgia court case and was widely adopted by insurers because it is very effective at minimizing payouts.

The 17c formula is the standard method used by USAA and most carriers to calculate diminished value. Its biggest flaw is that it systematically caps the maximum payout at 10% of your car’s pre-accident market value.

This creates an immediate, artificial ceiling on your claim. If your car was worth $30,000 before the accident, the 17c formula will not allow a diminished value payout of more than $3,000, even if the real-world loss is double that amount. It’s a rigid system that hurts owners of higher-value vehicles the most. You can find more details on how insurers like USAA handle these claims on SnapClaim.com.

The formula continues to apply reductions that work against you:

- The 10% Cap: It starts with your vehicle’s NADA or Kelley Blue Book value and immediately limits the maximum possible loss to 10%.

- Mileage Reductions: Next, it applies a “mileage modifier.” If your car has higher-than-average mileage, the amount is reduced further.

- Damage Reductions: Finally, a “damage modifier” is applied based on broad categories like “minor” or “severe,” which rarely capture the true market impact of the repairs.

This layered system of deductions means the final number they offer is just a fraction of your car’s actual loss. It’s a mathematical process designed for claim minimization, not fair valuation.

A Real-World Scenario

Let’s see how the 17c formula can undervalue a claim.

Imagine your nearly new SUV, valued at $40,000, was rear-ended. The repairs were significant, costing over $9,000 and involving structural work.

A USAA adjuster using the 17c formula would likely calculate the diminished value this way:

| Calculation Step | Description | Resulting Value |

|---|---|---|

| Step 1: Apply 10% Cap | Start with the NADA value and take 10%. | $40,000 x 10% = $4,000 |

| Step 2: Apply Damage Modifier | The adjuster flags the damage as “severe” (0.75 multiplier). | $4,000 x 0.75 = $3,000 |

| Step 3: Apply Mileage Modifier | Your vehicle has 50,000 miles (0.60 multiplier). | $3,000 x 0.60 = $1,800 |

The final offer from USAA is $1,800.

However, anyone familiar with the used car market knows a vehicle with that accident history could easily lose $5,000 to $7,000 in resale value. The formula ignores how real buyers react to structural damage, airbag deployment, or a negative vehicle history report.

This is why their initial offer should never be the final word. The key to successful negotiation is to counter their flawed formula with credible, market-based evidence. A certified appraisal report from SnapClaim provides the proof you need to negotiate fairly.

How to Prove Your Vehicle’s True Loss in Value

To counter USAA’s formula-based offer, you must prove your car’s actual drop in value. This requires shifting the negotiation from their internal spreadsheets to a discussion based on real-world market evidence. Building a strong case with the right documentation is key to getting fair compensation for your USAA diminished value claim.

Think of it as preparing for a legal case. You need credible, unbiased evidence that clearly shows your financial loss. An adjuster’s opinion or a generic online calculator is not enough. Your goal is to present a logical, fact-based argument they cannot easily dismiss.

Your Evidence Checklist

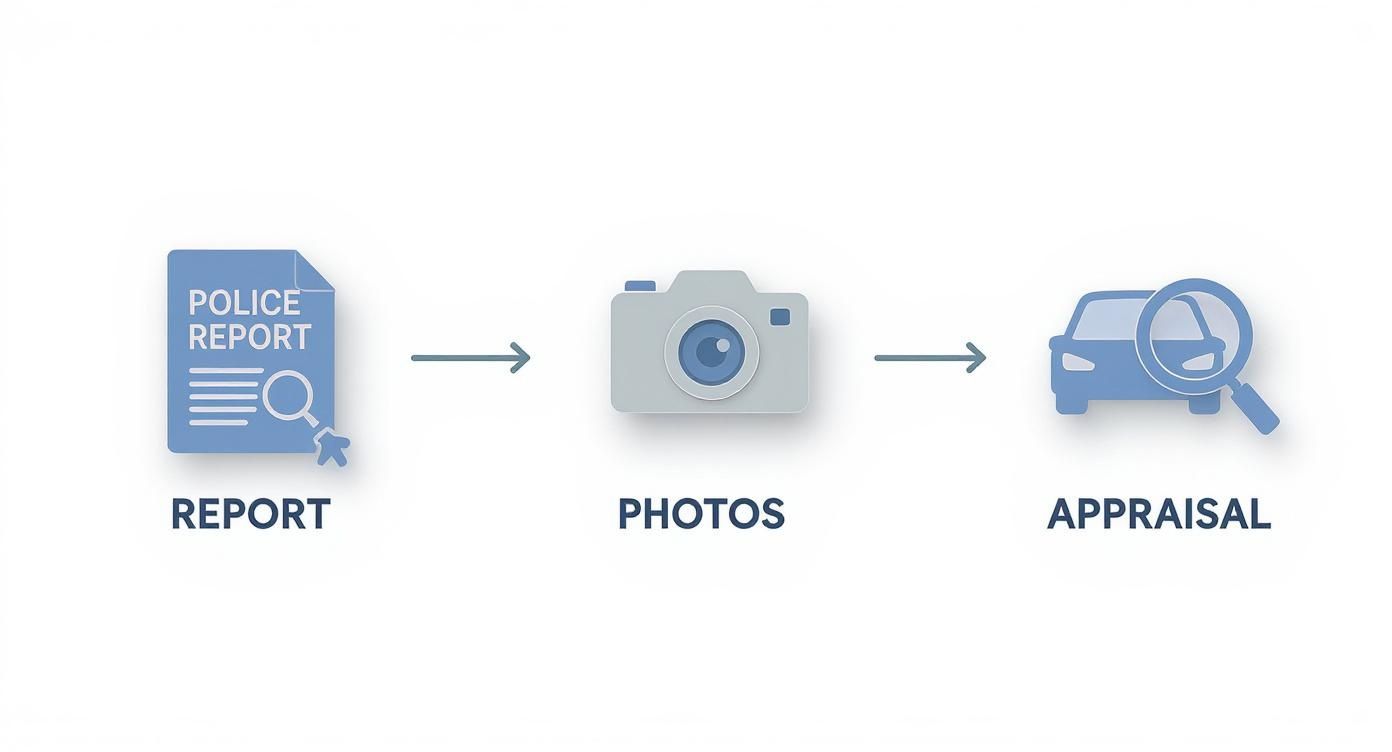

Organizing your paperwork from the start makes the entire process smoother and more effective. Each document helps tell the full story of your vehicle’s damage and its resulting loss in value.

Here are the essential documents you’ll need:

- The Official Police Report: This establishes the facts of the accident, most importantly identifying the at-fault driver.

- Detailed Photographs: Before repairs begin, take clear photos of the damage from multiple angles. This visual proof is crucial for showing the severity of the impact.

- The Final Repair Invoice: This is more than just a bill; it’s a detailed breakdown of every part replaced and every hour of labor performed. It provides concrete proof of how extensive the repairs were. Highlight any mention of structural work or frame damage, as these have the biggest impact on resale value.

While these documents build your foundation, they don’t assign a specific dollar amount to your loss. For that, you need a more powerful tool.

The Power of an Independent Appraisal

The single most important piece of evidence you can provide is a professional, third-party diminished value appraisal. This isn’t just another opinion; it’s an expert report that moves the conversation away from USAA’s generic formula and toward a data-driven valuation of your specific vehicle.

A certified appraisal report from SnapClaim is the definitive proof of your vehicle’s true lost value. It grounds the negotiation in verifiable market data rather than the insurer’s self-serving 17c formula.

A SnapClaim report accomplishes several key goals:

- Provides Unbiased Proof: The report comes from an impartial expert, giving it far more credibility than any valuation from you or the insurer.

- Uses Real Market Data: Our reports analyze comparable vehicle sales, auction data, and dealership insights to calculate the actual drop in your car’s market value.

- Is Defensible and Court-Ready: Every report is prepared to stand up to scrutiny from insurance adjusters and is formatted to be admissible in court if necessary.

When you present a USAA adjuster with a certified appraisal, the dynamic of the negotiation changes. You are no longer just disagreeing with their number; you are challenging their entire method with a superior, evidence-backed analysis.

Why USAA Adjusters Take Appraisals Seriously

Insurance companies operate on documentation. While they may initially push back, a professional report from a reputable source like SnapClaim is difficult to ignore. Adjusters know these reports can become the foundation for legal action if a fair settlement isn’t reached.

By investing in a certified appraisal, you signal that you are serious about your claim and have the evidence to prove it. This one proactive step can often prevent a long, drawn-out dispute. You can use our free diminished value 17c calculator to get an initial estimate before ordering a full report.

How to Negotiate Your USAA Diminished Value Claim

Once you’ve gathered your evidence, it’s time to formally present your USAA diminished value claim. Approach this as a business negotiation where you are presenting a clear, fact-based argument supported by your certified appraisal.

Your primary goal is to shift the adjuster’s focus from USAA’s internal formulas to the real-world market data you have collected. A professional, well-documented approach makes it difficult for an adjuster to dismiss your claim.

This workflow ensures every part of your claim is supported by credible, third-party evidence that an adjuster must consider.

Crafting a Professional Demand Letter

Your first step is to send a formal demand letter. This is a professional communication that lays out the facts and clearly states the compensation you are seeking.

A strong demand letter should include:

- Your Information: Your full name, contact information, and the USAA claim number.

- Accident Details: A brief summary of the accident date, confirming their insured was at fault and referencing the police report number.

- Vehicle Information: Your car’s year, make, model, and VIN.

- Your Demand: The exact diminished value amount you are claiming, which should match the figure from your independent appraisal.

- Supporting Documents: Attach copies of the police report, the final repair invoice, and your certified diminished value appraisal.

Handling Common Adjuster Objections

After the adjuster receives your demand, expect a phone call. Be prepared for pushback. Their job is to minimize payouts, and they often rely on a script of common objections. Your role is to remain calm and steer the conversation back to your evidence.

Here are common objections and how to respond:

- “We don’t accept third-party appraisals.” Respond politely but firmly: “This report was prepared by a certified, independent appraiser using verifiable market data. It’s a more accurate reflection of my car’s loss in value than a generic formula. Can you point to any specific errors in the data or methodology?”

- “Our calculation shows the value is only $X.” This indicates they are relying on the 17c formula. Highlight its weaknesses: “The 17c formula is a one-size-fits-all calculation that doesn’t account for my vehicle’s specific condition or our local market. My appraisal is based on actual market evidence for my exact car.”

- “That appraisal amount is too high.” Don’t get defensive. Ask them to justify their position with facts: “On what basis do you believe it’s too high? Please provide the comparable sales data you used to determine that my appraiser’s valuation is incorrect.”

The key is to never let the negotiation become a battle of opinions. When an adjuster offers an opinion, you counter with a fact from your report. This keeps the focus on the evidence, where you hold the advantage.

State Laws and Your Claim

The success of your USAA diminished value claim heavily depends on the specific laws in your state. There is no federal standard for diminished value, which means every state has its own rules, deadlines, and legal precedents.

Knowing these local rules is essential. They dictate if you are eligible, how long you have to file, and the strategy you should use. Filing a claim without this knowledge is a common reason why valid claims are denied.

First-Party vs. Third-Party Claims

Understanding the difference between a first-party and a third-party claim is critical.

- First-Party Claim: This is when you file against your own insurance policy. In most states, you cannot claim diminished value from your own insurer.

- Third-Party Claim: This is when you file against the at-fault driver’s insurance policy. This is where almost all diminished value claims are made.

The Statute of Limitations

Every state has a strict time limit for filing a claim for property damage, known as the statute of limitations. If you miss this deadline, you lose your right to seek compensation permanently. This deadline can vary significantly by state. For example, some states give you only two years to file. To learn more about specific state laws, you can read expert guides like this one on Texas law from Thomas J. Henry Law.

Because these laws are complex, it’s vital to have accurate and current information. A certified appraisal report from SnapClaim is prepared with state-specific requirements in mind, ensuring your documentation aligns with local laws. For instance, our guide on how diminished value works in California details the unique rules for that state.

Frequently Asked Questions About a USAA Diminished Value Claim

Here are answers to some of the most common questions about filing a USAA diminished value claim.

Can I claim diminished value if the accident was my fault?

No, you generally cannot. Diminished value is almost exclusively a third-party claim, meaning you can only recover it from the at-fault driver’s insurance company. Your own policy typically covers repairs but not the loss in your vehicle’s resale value.

How long do I have to file a USAA diminished value claim?

The deadline is determined by your state’s statute of limitations for property damage, not by USAA’s internal policies. This window is typically between two and four years from the date of the accident. It is crucial to know your state’s deadline, as missing it will prevent you from recovering compensation.

Does USAA pay diminished value claims without being asked?

No. Like all insurance companies, USAA will not voluntarily offer to pay for your car’s lost value. The responsibility is on you, the vehicle owner, to prove your loss and formally demand compensation. If you don’t file a claim, you will not get paid.

What if USAA rejects my independent appraisal?

This is a common tactic. Do not panic. Politely ask the adjuster to provide a detailed rebuttal in writing that explains exactly why they are rejecting it. A vague statement like “it’s too high” is an opinion, not a valid reason. A high-quality, data-driven report from SnapClaim is built on verifiable market analysis, making it very difficult for an adjuster to dispute without providing their own evidence.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes. Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

SnapClaim provides the certified proof you need to strengthen your claim and negotiate from a position of authority. With our Money-Back Guarantee, you can pursue your claim with confidence. If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee — guaranteed.

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step. Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.