After a car accident, your focus is on getting your vehicle repaired. But even with perfect repairs, your car now has an accident history, and that history lowers its resale value. The good news is you can recover that loss by filing a Liberty Mutual diminished value claim. Learn more about the Liberty Mutual insurance claim process.

What Is a Diminished Value Claim?

Diminished value is the difference between your car’s fair market value right before an accident and its value after being repaired. It’s a simple concept: buyers pay less for a vehicle with a collision on its record.

Think of it this way: if you were shopping for a used car and saw two identical models, but one had been in a wreck, you’d expect a discount. That price difference is the diminished value. Filing a claim ensures the at-fault driver’s insurance—not you—covers this financial loss. It’s about being made whole again.

For a deeper dive, check out our complete guide on what is a diminished value claim.

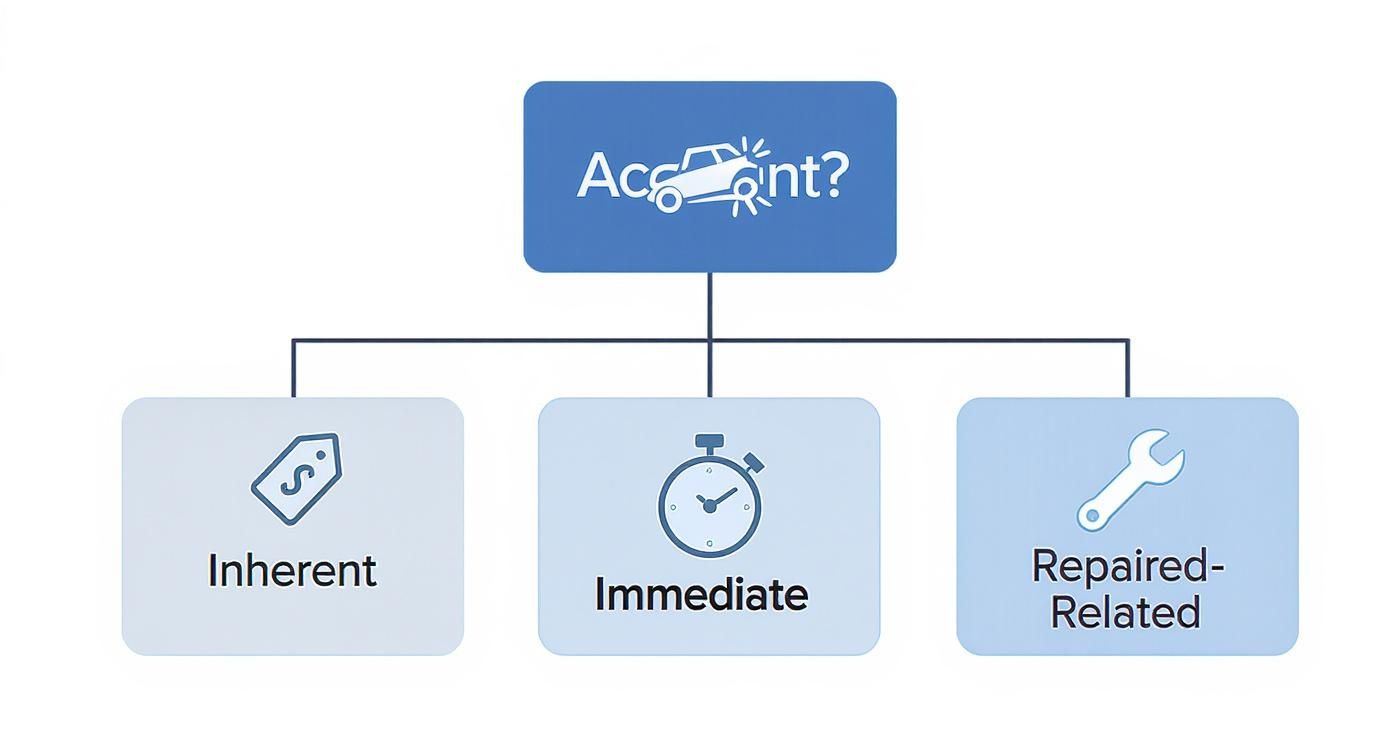

The Three Types of Diminished Value

When you file your claim, the adjuster will likely think about your loss in one of three ways. Understanding these categories helps you build a stronger case.

- Inherent Diminished Value: This is the most common type. It’s the automatic drop in your car’s value simply because it now has a permanent accident history, even if the repairs are flawless.

- Immediate Diminished Value: This refers to your vehicle’s value immediately after the accident but before repairs have been made. It’s a less common basis for a claim.

- Repair-Related Diminished Value: This occurs when the body shop performs low-quality work, like using mismatched paint or cheap parts, which further hurts your car’s value.

Most claims focus on inherent diminished value. By correctly identifying your loss, you can present your evidence more effectively.

Do You Have a Valid Claim Against Liberty Mutual?

Before you start gathering paperwork, it’s important to confirm you’re eligible. Not every accident qualifies for a diminished value payout from Liberty Mutual.

The most critical factor is fault. You can only file a diminished value claim against the at-fault driver’s insurance company. It’s paid out from their liability coverage. If you caused the accident, your own collision policy will pay for repairs, but it won’t cover your car’s lost resale value.

Key Factors That Strengthen Your Claim

Once you’ve confirmed the other driver was at fault, Liberty Mutual will look at your vehicle’s profile and the severity of the damage. A strong claim typically includes:

- A Newer Vehicle: Cars under five years old with lower mileage suffer the greatest loss in value after an accident.

- Significant Damage: Structural or frame damage carries more weight than minor cosmetic scratches. The more extensive the repairs, the stronger your case.

- A Clean Pre-Accident History: Your vehicle must not have a history of previous collisions. A prior accident makes it difficult to prove the value lost from this specific incident.

For example, a two-year-old SUV that needed frame repairs has a strong claim. A 10-year-old sedan with a scraped bumper likely does not. State laws can also affect your eligibility, so it’s wise to be aware of your local regulations.

This infographic breaks down the different types of diminished value you might be dealing with.

As you can see, the vast majority of claims are for Inherent Diminished Value. This is the automatic, unavoidable loss in value that happens simply because your vehicle now has an accident on its record—and that’s what your claim will primarily be about.

How to Prove Your Loss to Liberty Mutual

A successful Liberty Mutual diminished value claim depends entirely on the quality of your evidence. You can’t just tell an adjuster your car is worth less; you have to prove it with clear documentation.

Your goal is to build a “proof of loss” file that tells the complete story of the accident, the repairs, and the resulting drop in your car’s market value. A clear paper trail leaves no room for doubt.

What Documents Do You Need?

Start by gathering every document related to the accident and your vehicle. Each one helps validate your claim and prevents the adjuster from finding gaps to deny or delay payment.

Here’s a checklist of the essential documents for building a rock-solid case with Liberty Mutual.

| Essential Documents for Your Diminished Value Claim | Why It’s Important |

|---|---|

| Document Type | Why It’s Important |

| Official Police Report | This establishes the core facts of the accident, including who was at fault, which is mandatory for a third-party claim. |

| Photos & Videos (Pre- and Post-Accident) | Pre-accident photos prove your car was in excellent condition. Photos from the scene show the extent of the damage, creating a powerful before-and-after narrative. |

| Itemized Repair Invoice | This document details the severity of the damage by listing every part replaced and every hour of labor. It makes it hard for the insurer to downplay the repairs. |

| Proof of a “Clean” Title | A copy of your vehicle’s title or registration confirms it didn’t have a prior “salvage” brand, which is key to establishing its pre-accident fair market value. |

| Your Independent Diminished Value Appraisal | This is your most important piece of evidence. An expert report quantifies your financial loss with real market data, directly countering the insurer’s lowball formulas. This transforms your claim from an ask to a demand. |

Don’t underestimate the power of pre-accident photos. Insurers often argue that some value loss is due to “prior wear and tear.” A picture of your well-maintained car from a month before the wreck can quickly shut down that argument.

The Cornerstone of Your Claim: An Independent Appraisal

The documents above prove the accident happened and your car was repaired. However, they don’t prove the financial loss. That’s where an independent appraisal from a certified expert becomes your most powerful tool.

Liberty Mutual uses its own internal methods, like the flawed “17c” formula, to calculate diminished value. This formula is designed to produce the lowest possible payout. Accepting their number is not in your best interest.

An independent appraisal from a trusted source like SnapClaim provides the objective, data-backed evidence you need to negotiate fairly. Our reports analyze real-time market data, consider your vehicle’s specific repairs, and calculate a defensible diminished value figure. This report turns your claim into a formal, evidence-based demand. Searching for a certified diminished value appraiser near me is the best way to get started.

Submitting Your Demand to Liberty Mutual

With your evidence gathered and certified appraisal in hand, it’s time to formally demand what you’re owed. The key to this step is a professional demand letter.

Your goal is to be firm, respectful, and fact-based. Leave emotion out of it. The adjuster is just doing their job, and a logical, well-supported case makes it easier for them to approve your claim.

What Goes into an Effective Demand Letter

A strong demand letter should be concise and to the point—keep it to one page.

Here’s what you need to include:

- Your Information: Full name, address, and the Liberty Mutual claim number.

- Accident Details: Briefly mention the date of the accident and the name of their insured driver.

- Vehicle Information: Your car’s year, make, model, and VIN.

- Your Demand: Clearly state the diminished value amount you are claiming. For example: “Based on the enclosed certified appraisal from SnapClaim, my vehicle has suffered a loss in value of $4,500.”

- List of Enclosures: Itemize every document you are including, such as the police report, final repair bill, and your appraisal report.

This organized approach shows the adjuster you are serious and have done your homework.

Where and How to Send Your Demand

Send your demand letter directly to the property damage adjuster assigned to your claim. Don’t send it to a generic corporate address where it can get lost.

Pro Tip: Always send your demand letter and all supporting documents via a trackable method, like Certified Mail with a return receipt. This gives you legal proof that Liberty Mutual received your package and when, preventing them from claiming they “never got it.”

Once sent, give them a week or two to respond. If you don’t hear back, follow up with a polite phone call or email. Your professional demand has now set the stage for a successful negotiation.

Negotiating Your Liberty Mutual Diminished Value Claim

After Liberty Mutual receives your demand, prepare for their standard negotiation tactics. The first offer is almost never their best—it’s a test to see if you’ll accept a low amount and go away.

Adjusters often lead with a lowball figure based on the inaccurate “17c formula” or claim your evidence isn’t sufficient. This is a routine strategy designed to make you give up. Don’t get discouraged; stand your ground with the solid data from your appraisal.

How to Respond to a Low Offer

When you receive the first offer, respond calmly and professionally. Politely reject their offer and immediately pivot back to your evidence. Point to specific market data and comparisons in your SnapClaim appraisal that prove your claim is fair.

A professional, fact-based response might sound like this:

“Thank you for reviewing my Liberty Mutual diminished value claim. While I appreciate your initial offer of $1,200, it does not adequately cover my vehicle’s loss in market value. As shown in my certified appraisal, comparable vehicles with accident histories in my area are selling for an average of $4,800 less than those with clean records. My original demand is supported by this data.”

This approach replaces emotion with evidence, making it difficult for the adjuster to defend their low number.

Escalating Your Claim When Necessary

What if Liberty Mutual refuses to make a fair offer? If you’ve negotiated politely and they still won’t budge, you have more options.

At SnapClaim, our certified reports give you the proof you need to negotiate confidently. To make it a risk-free investment, we offer a Money-Back Guarantee. If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee — guaranteed.

Learn more on how to deal with Liberty Mutual Insurance Adjuster.

Frequently Asked Questions (FAQ)

Here are answers to some of the most common questions about filing a Liberty Mutual diminished value claim.

Can I file a diminished value claim if I was at fault?

No. Diminished value is considered a third-party liability claim, which means you must file it against the at-fault driver’s insurance policy. Your own collision coverage pays for repairs to your vehicle, but it does not cover its loss in resale value.

How long do I have to file my claim?

Every state has a deadline for filing property damage claims, known as the statute of limitations. This typically ranges from two to five years from the date of the accident. It is crucial to know your state’s deadline, but it’s always best to file your claim as soon as your repairs are complete.

What if Liberty Mutual denies my claim or offers too little?

An initial denial or a lowball offer is a common negotiation tactic. First, ask for the decision in writing with a clear explanation of their reasoning. Then, respond with a polite counter-offer that refers back to the data in your independent appraisal report. If they still refuse to negotiate fairly, you can invoke the appraisal clause or consult with an attorney.

Does my car’s age and mileage affect my claim?

Yes, absolutely. A vehicle’s pre-accident condition, age, and mileage are critical factors. A newer, low-mileage vehicle with a clean history will have a much higher diminished value than an older, high-mileage car with previous accidents. The amount of your car value after the accident is directly tied to its value before the incident. You can learn more about how companies like Liberty Mutual handle these claims and why the burden of proof is always on you.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes. Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step. Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.