Total Loss Appraisal in

Iowa

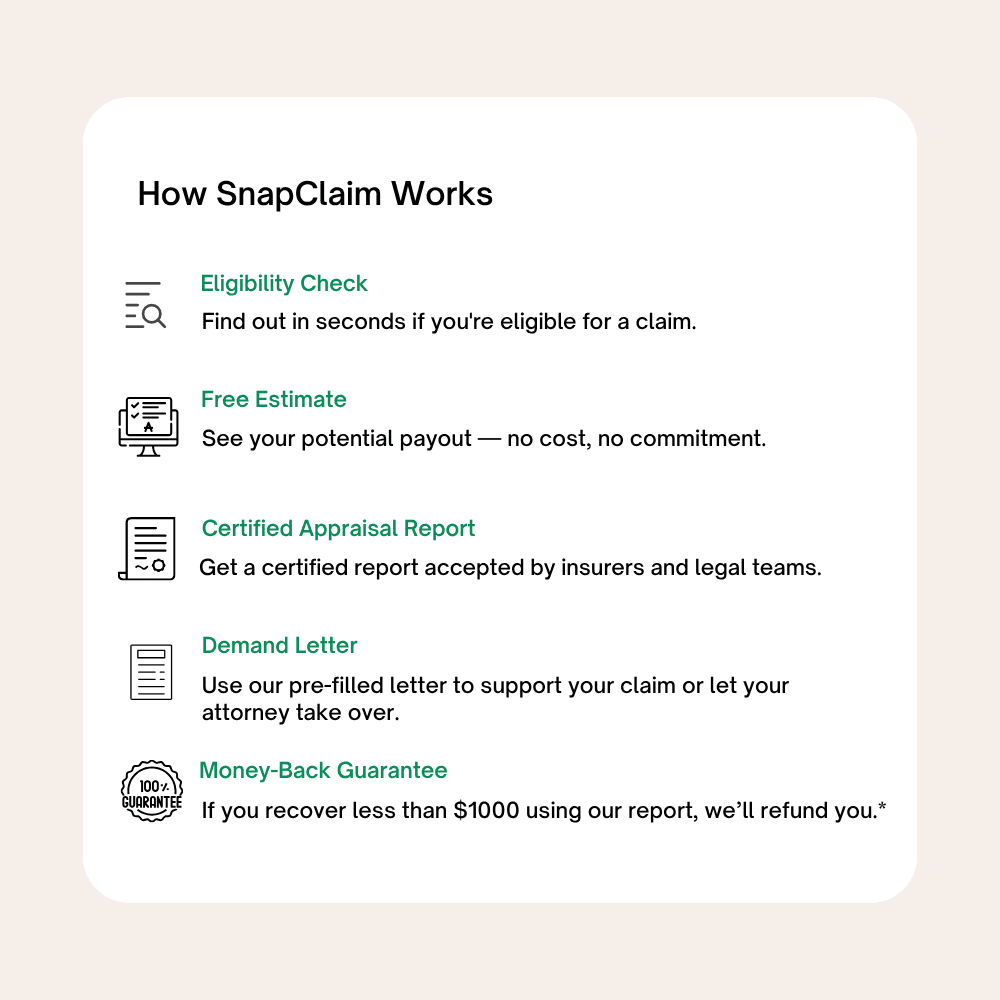

Get Your Free Estimate in a Minute!

If your car was declared a total loss and you’re not happy with the insurance payout, you have the right to request a Iowa total loss appraisal. SnapClaim helps you dispute unfair insurance valuations with certified, data-backed reports that show your vehicle’s true fair market value.

No credit card required [Takes less than 30 second]

Total Loss Appraisal in Iowa: What You Need to Know

Iowa Total Loss Appraisal — Get the Full Value of Your Totaled Vehicle

If your vehicle was declared a total loss and the insurance payout seems too low, you have the right to obtain an independent Iowa total loss appraisal. Whether the collision happened in Des Moines, Cedar Rapids, Davenport, Sioux City, Iowa City, Waterloo, or anywhere across the state, SnapClaim helps Iowa drivers recover their vehicle’s true fair market value (ACV) and secure a fair settlement. Our certified total loss appraisal reports are data-driven, USPAP-aware, and accepted by insurers, arbitrators, and small-claims courts across Iowa.Why Get a Total Loss Appraisal in Iowa?

Insurance valuation systems like CCC and Mitchell often undervalue Iowa vehicles, especially in urban and growing markets where replacement costs are significantly higher than rural averages. An Iowa appraisal ensures your ACV reflects real local resale pricing—not outdated or mismatched comps pulled from lower-value counties.Common Reasons to Dispute a Total Loss Offer

- Incorrect trim, equipment, mileage, or optional packages listed in CCC/Mitchell

- Comparables pulled from low-value rural markets or entirely different states

- Unreasonable deductions or incorrect condition adjustments

- Price premiums ignored for trucks, SUVs, AWD, EVs, and commuter vehicles

What’s Included in Your Iowa Total Loss Appraisal Report

- Complete VIN-based vehicle analysis (trim, options, mileage, condition)

- Verified local comparable listings from Iowa and surrounding markets

- Accurate pre-loss fair market value calculation

- Transparent adjustment tables for features, mileage, and condition

- Documentation to invoke your appraisal clause

- Optional expert witness support for arbitration or litigation

Iowa Total Loss Laws & Appraisal Rights

Iowa drivers are protected under the state’s Unfair Insurance Practices Act. You may dispute an insurance company’s ACV determination by invoking the appraisal clause in your auto policy. If the appraisers disagree, a neutral umpire makes the final determination. Useful Iowa resources:- Iowa Insurance Division — Auto Insurance

- File a Complaint — Iowa Insurance Division

- Iowa Judiciary — Small Claims

How to Dispute a Total Loss Offer in Iowa

- Request your CCC, Mitchell, or insurer valuation report.

- Order a SnapClaim appraisal to establish your true pre-loss ACV.

- Invoke your appraisal clause if the insurer will not adjust their offer.

- Submit your SnapClaim report directly to your adjuster.

- Negotiate or escalate—many Iowa drivers recover thousands more.

Iowa Market Trends & Local Insight

- Trucks, work vehicles, and AWD SUVs carry higher premiums due to weather and agricultural demand.

- College towns (Ames, Iowa City) typically show elevated values due to limited inventory.

- Growing suburban markets (Ankeny, Urbandale, West Des Moines) often outpace statewide averages.

- Border cities like Council Bluffs and Sioux City show cross-state pricing influences.

Example Iowa Case Study

Vehicle: 2018 Ford F-150 XLT 4×4 Insurance Offer (CCC): $21,300 SnapClaim Appraisal: $26,450 Final Settlement: $26,000 after invoking the appraisal clauseHelpful Iowa Resources

Ready to Get Your Iowa Total Loss Appraisal?

- No upfront cost

- Delivered in about 1 hour

- Insurer-ready fair-market-value documentation included

Related Iowa Locations

Click a pin to open the city’s total loss page.

Find your Iowa city below to order your Total Loss Appraisal.

Order Your Total Loss Appraisal

Get Your Appraisal Report and Demand Letter Now!

Free Estimate, no credit card required.

Dispute an Unfair Total Loss Offer in Iowa

If your car was declared a total loss in Iowa but the insurance payout seems too low, you don’t have to accept it. Under your policy’s appraisal clause, you can request an independent Iowa total loss appraisal to verify your vehicle’s true fair market value. SnapClaim makes it simple — get a certified total loss report, invoke your appraisal rights, and negotiate a higher settlement — all within minutes.

“After my SUV was totaled in a storm-related crash outside Des Moines, the insurance offer came in way under what vehicles were actually selling for across Iowa. SnapClaim pulled real comps from Des Moines, West Des Moines, and Ames. Their appraisal shifted the entire negotiation — I recovered an extra $3,450 beyond the original payout.”

Kelly H.,

Des Moines, IA

Frequently Asked Questions

When is a car considered a total loss in Iowa?

An insurer may declare a total loss when repairing the vehicle no longer makes economic sense compared with its Actual Cash Value (ACV) before the crash. They compare estimated repair costs (including potential supplements) and salvage value to your car’s pre-accident value to decide if it’s “totaled.” You can see general rules by state here: total loss state laws.

What does Actual Cash Value (ACV) mean in Iowa?

ACV is your car’s fair market value immediately before the accident—what a willing buyer would have paid for it in the Iowa market. It considers year, make, model, trim, options, mileage, condition, and local comps across Des Moines, Cedar Rapids, Davenport, Sioux City, Iowa City, Waterloo, Ames, West Des Moines, and surrounding areas. Learn more about how ACV is calculated: Fair Market Value.

My car still drives, but the insurer says it’s a total loss. What now?

A vehicle can be “totaled” on paper and still feel perfectly drivable. You can:

• Ask how the adjuster calculated ACV and repair costs

• Review the valuation report and comps they used

• Ask about owner retention so you can keep the vehicle with a reduced payout

• Get an independent Iowa total loss appraisal from SnapClaim before signing any release:

Iowa Total Loss Appraisals.

Why do Iowa market conditions matter for my total loss value?

Iowa’s market ranges from metro areas like Des Moines and Cedar Rapids to college towns and rural farming regions. Trucks, SUVs, and reliable commuter cars can command different premiums depending on the area, mileage, and condition. A valuation built on out-of-state comps or lower-value markets may understate your ACV. SnapClaim uses Iowa-focused data and verified local listings so your value reflects what a similar vehicle actually sells for in your part of Iowa.

How much should insurance pay if my car is totaled in Iowa?

In a total loss, insurers generally owe your vehicle’s fair market value at the time of loss (its ACV), plus applicable taxes and certain fees. If you use your own collision or comprehensive coverage, your deductible may apply. If the at-fault driver’s insurer pays, there’s typically no deductible.

What if I still owe on a loan or lease in Iowa?

The insurer pays up to the car’s ACV to you or directly to your lender/lease company. If your payoff is higher than the total loss settlement, you’re responsible for the difference unless you have GAP coverage or special lease protections. A fair, data-backed ACV from an independent Iowa appraisal can reduce how much negative equity you’re left with.

What happens to my title after a total loss in Iowa?

When a vehicle is declared a total loss, it will generally be branded with a salvage title. If the vehicle is later repaired, Iowa has a salvage-to-rebuilt title process and inspections that must be completed through the Iowa Department of Transportation (DOT) before the vehicle can legally return to the road. Check the latest Iowa DOT guidance for the current requirements.

Can I keep my totaled vehicle in Iowa (and still get paid)?

In many cases, yes. This is called retaining the salvage. Typically:

• You keep the vehicle

• Your cash settlement is reduced by the agreed salvage value

• You must follow Iowa’s salvage/rebuilt title rules and pass inspections if you plan to repair and drive it again

Are taxes and fees included in an Iowa total loss settlement?

Total loss settlements may include applicable sales tax, title, and registration fees depending on Iowa rules and how your claim is handled. Always ask your adjuster for a line-by-line, itemized breakdown of ACV, taxes, and fees so you know exactly what’s being paid. Learn more about line items: ACV & line items.

What if my Iowa total loss offer seems too low?

Start by requesting the full valuation report (CCC, Mitchell, etc.) and checking for:

• Comps from cheaper out-of-state markets

• Missing trim level, packages, or technology options

• Incorrect mileage, condition, or equipment

If the number still looks off, a certified Iowa appraisal from SnapClaim can give you a

market-backed value to negotiate with:

Start your appraisal.

How long do I have to deal with a total loss claim in Iowa?

Iowa law sets deadlines (statutes of limitations) for bringing property damage claims after a crash. The exact time limits can depend on your situation and who you’re making a claim against. Because missing a deadline can seriously affect your rights, it’s important to talk with an Iowa attorney about the specific time limits that apply to your case. This is general information, not legal advice.

Can the appraisal clause in my policy help if I disagree on value?

Many Iowa auto policies include an appraisal clause. If you and the insurer can’t agree on ACV:

• Each side hires an appraiser

• The two appraisers try to agree on value

• If they can’t, a neutral umpire reviews both positions and sets the value

A detailed, data-driven SnapClaim appraisal can strengthen your position during this process.

Can I use a SnapClaim appraisal in Iowa court or arbitration?

Yes. SnapClaim’s certified, USPAP-aware reports are designed to be used in small claims court, arbitration, or mediation to support the value you’re claiming. We also work with attorneys handling total loss and property damage disputes for Iowa drivers.

How does SnapClaim help Iowa drivers with total loss claims?

We build Iowa-specific valuation files using verified listings from Des Moines, Cedar Rapids, Davenport, Sioux City, Iowa City, Waterloo, Ames, and surrounding markets. Our appraisals:

• Are based on real Iowa market data, not generic national averages

• Clearly explain every adjustment so adjusters, appraisers, and courts can follow

• Are often used to help drivers recover thousands more than the insurer’s first offer

Start your Iowa total loss appraisal.

Diminished Value & Total Loss Appraisal Reports

Instant Free Estimate

Instant diminished value and total loss appraisals — no guesswork, no delays, backed by a 100% money-back guarantee.

Free Estimate, no credit card required.