If another driver hit your car, their insurance is responsible for the repairs. But what about the permanent dent in your car’s resale value? That drop, known as diminished value, is a real financial loss that State Farm may owe you, and knowing how to file a diminished value claim with State Farm is the key to getting fair compensation.

Understanding Diminished Value and Your Rights

When someone else causes an accident, your vehicle suffers two types of losses. The first is obvious: the cost to fix the physical damage. The at-fault driver’s insurance—in this case, State Farm—is responsible for covering those repair costs.

The second loss is the permanent drop in your car’s market value. This is called inherent diminished value. Even with flawless repairs that make your car look perfect, it now has an accident history. That history is a red flag for savvy buyers and vehicle history reports like Carfax. No informed buyer will pay the same price for a car with a collision record as they would for an identical one with a clean history.

This difference in value is a measurable financial loss you’ve suffered through no fault of your own. You have a legal right to be “made whole,” which includes being compensated for this loss in your car value after an accident.

A Real-World Example of Diminished Value

Imagine you own a two-year-old SUV with a pre-accident value of $30,000. Another driver runs a red light, causing $7,000 in damage. The body shop does an excellent job, and the vehicle looks good as new.

A year later, you decide to trade it in. The dealership’s offer is thousands less than you expected. When you ask why, they point to the “moderate structural damage” now listed on its vehicle history report. That gap between its repaired value and the value it should have had is your diminished value. In this common scenario, that loss could easily be $4,000 or more.

Why You Can’t Trust the Insurer’s Formula

Before you file, it’s important to understand how State Farm calculates these claims and why your independent documentation is so critical.

| Key Component | What You Need to Know | Why It Matters |

|---|---|---|

| Eligibility | You must be the not-at-fault party in most states. | The at-fault driver’s State Farm policy is responsible for your losses. |

| Initial Offer | Often based on a generic internal formula like “17c.” | These formulas are designed to minimize payouts, not reflect real market loss. |

| Required Proof | A demand letter and an independent appraisal are crucial. | Your evidence must prove the actual market value loss, not what their formula says. |

| Negotiation | The first offer is a starting point, not the final word. | You need strong, data-backed evidence to counter their lowball number. |

Insurance companies like State Farm often use internal formulas to calculate diminished value. The most well-known is the “17c formula”, which originated from a Georgia court case. This formula typically starts with 10% of the vehicle’s pre-accident value and then applies arbitrary deductions for mileage and damage severity.

The problem? These formulas are engineered to minimize what the insurer pays, not to reflect what’s actually happening in the used car market. They consistently undervalue claims. Relying on State Farm’s calculation is a sure way to leave money on the table. The only way to counter their lowball offer is with independent, data-backed proof of your actual loss. This is where a certified appraisal from SnapClaim becomes your most powerful tool.

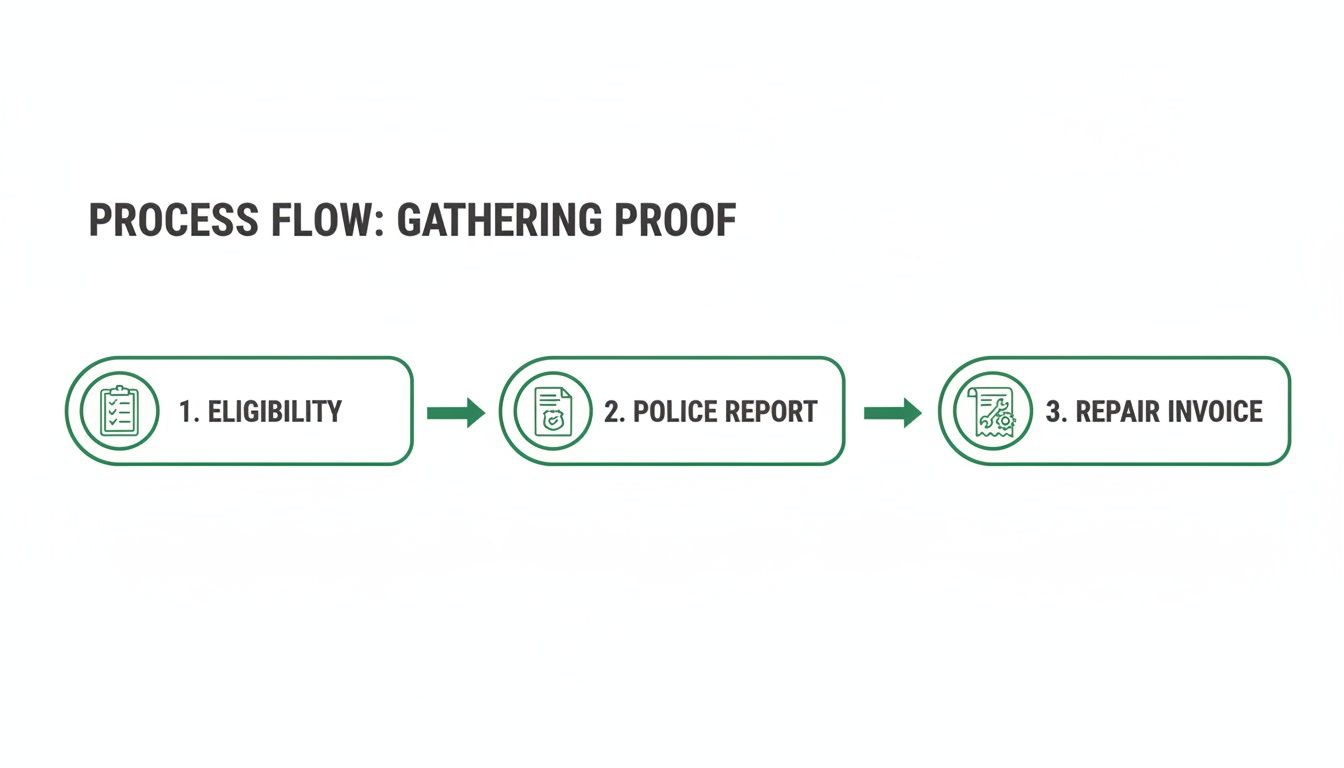

Step 1: Confirm Your Eligibility and Gather Proof

Before you can figure out how to file a diminished value claim with State Farm, you must confirm you have a solid case. The most important factor is determining who was at fault for the accident.

In nearly every state, you can only pursue a diminished value claim from the at-fault driver’s insurance company. This is called a third-party claim. If a State Farm driver hit you, you have the right to seek compensation for your car’s loss in value. They are responsible for making you “whole” again, which includes both the repairs and the hit to your car’s market price.

First-Party vs. Third-Party Claims

What if you were at fault? That’s when you would file a first-party claim with your own insurance. Unfortunately, most standard auto policies explicitly exclude coverage for diminished value in first-party claims. The one major exception is Georgia, where drivers can file a diminished value claim against their own insurer. For everyone else, your claim depends on proving the other driver was at fault.

Building Your Case with Essential Paperwork

Once you’ve confirmed you have a valid third-party claim, it’s time to gather your proof. Presenting a State Farm adjuster with an organized file shows you are serious and prepared.

Here is the essential documentation you will need:

- The Police Report: This document officially identifies who was at fault and provides a narrative of the accident.

- The Final Repair Invoice: The detailed, itemized bill from the body shop shows the full extent of the damage and repairs.

- Photos: Pictures of your car before the accident, the damage after, and even during the repair process create a powerful visual record.

- Vehicle History Reports: Reports from services like Carfax or AutoCheck show your car’s clean record before the collision and will eventually flag the accident for future buyers.

Having these documents ready before you contact State Farm changes the dynamic. You aren’t just asking for money; you are presenting a case built on facts. For a full breakdown of what to do, check out our guide on the steps to take after a car accident.

Step 2: Calculate Your Loss and Submit Your Claim

You’ve confirmed your eligibility and gathered your proof. Now it’s time to put a real number on your loss and formally present it to State Farm.

State Farm will likely start with a lowball offer based on their “17c formula.” This formula is notorious for producing small settlement amounts that don’t reflect your car’s actual drop in market value. Do not accept their first offer. Think of it as an opening bid, not the final word.

The Power of an Independent Appraisal Report

This is why an independent, certified appraisal is essential. It is the most effective tool for a successful diminished value claim. An appraisal replaces State Farm’s self-serving formula with an objective, data-backed analysis of your vehicle’s true loss in value. A report from a trusted provider like SnapClaim isn’t just an opinion—it’s a professional valuation grounded in real-world market data.

Our appraisers analyze key factors to determine your actual loss:

- Vehicle Profile: Year, make, model, mileage, and pre-accident condition.

- Damage Severity: A detailed review of the final repair bill to understand if damage was cosmetic or structural.

- Local Market Data: Sales data for vehicles like yours in your area, comparing those with and without accident histories.

This methodical approach provides the hard proof needed to justify your claim and shifts the conversation from their formula to the facts. To learn more about what goes into these reports, see our guide on how to read a professional appraisal report.

How to Submit Your Claim to State Farm

With your professional appraisal in hand, it’s time to officially submit your demand.

- Online Portal: Uploading your demand letter, appraisal, and other evidence through State Farm’s claims portal creates a clear digital record.

- Email: Sending everything directly to the adjuster keeps all communication in writing. Ask for confirmation that they received it.

- Certified Mail: This formal approach provides undeniable proof of receipt and is a good option if the adjuster is slow to respond.

Writing a Simple and Effective Demand Letter

You don’t need a lawyer to write a strong demand letter. Keep it simple, professional, and factual.

Here’s a straightforward template you can adapt:

[Your Name]

[Your Address]

[Your Phone Number & Email][Date]

State Farm Insurance

[Adjuster’s Name, if known]

[Claims Department Address]RE: Demand for Diminished Value

Claim Number: [Your Claim Number]

Date of Loss: [Date of Accident]

At-Fault Party: [Name of the At-Fault Driver]Dear [Adjuster’s Name],

This letter is my formal demand for compensation for the inherent diminished value of my vehicle, a [Year, Make, Model, VIN], following the accident on [Date of Loss]. The collision was a direct result of the negligence of your insured, [At-Fault Driver’s Name].

Due to the accident history now attached to my vehicle’s record, its fair market value has been significantly reduced. I have enclosed a certified appraisal report from SnapClaim, which concludes my vehicle has lost $[Amount from Appraisal] in value.

To support my claim, I have also attached the following documents:

- The final, itemized repair invoice

- The official police report

- Photos of the vehicle damage

Please review the enclosed report and documentation. I expect a fair settlement of $[Amount from Appraisal] and look forward to your prompt response.

Sincerely,

[Your Signature]

[Your Printed Name]

Submitting this complete package positions you as a claimant who has done their homework, strengthening your claim from the start.

Step 3: Negotiate Your Settlement with the Adjuster

After you’ve sent your demand letter and appraisal, the negotiation begins. The State Farm adjuster’s goal is to close your claim for as little money as possible. Your goal is to be paid what you are rightfully owed. This process is not about arguing; it’s about presenting your case with calm confidence.

Your certified appraisal is the anchor of this conversation. Treat every interaction with the adjuster like a professional business discussion, and keep bringing the focus back to the market data proving your car value after the accident.

Common Adjuster Tactics and How to Respond

Adjusters are trained negotiators. Knowing their common tactics will help you prepare your responses.

Tactic:“Our high-quality repairs restored your vehicle to its pre-accident condition.”

- Your Response: “I appreciate the quality of the repairs, but that is a separate issue from the vehicle’s market value. The permanent accident history caused the financial loss, and my appraisal documents this specific market loss.”

Tactic:“We don’t pay for diminished value,” or “That’s not a covered loss.”

- Your Response: “My understanding of [Your State]’s law is that the at-fault party is responsible for making me whole, which includes the documented loss in my vehicle’s resale value. Are you stating that State Farm’s official position is to deny legally recognized property damage claims?”

Tactic:“Your appraisal is just an opinion. We use our own formula.”

- Your Response: “My appraisal is a certified report based on verifiable market data from my local area. Can you please provide a copy of your valuation, including the specific market comparables you used to arrive at your offer?”

By calmly steering the conversation back to your evidence, you remain in control. For more tips, check out this guide on how to negotiate with an insurance adjuster.

Document Everything

Document every interaction with the State Farm adjuster. After each phone call, send a brief follow-up email summarizing what was discussed. This creates a paper trail that prevents any “he said, she said” arguments later.

This documentation is priceless if you need to escalate your claim, as it shows you are serious and ensures nothing gets lost in the process. Your SnapClaim report provides the proof you need to negotiate fairly and confidently.

What to Do If State Farm Denies Your Claim

If State Farm denies your diminished value claim, don’t get discouraged. A denial is often an opening negotiation tactic, not the final word.

Your first step is to get the denial in writing. A written denial forces them to state their exact reason, giving you a specific point to argue against. Once you have it, it’s time to escalate.

Escalate to a Claims Manager

Arguing with the same adjuster who denied you is often unproductive. Instead, ask to speak with their direct supervisor or a claims manager. A fresh set of eyes on your file can make all the difference.

When you call, be direct and professional:

- State your purpose: “I’m calling to request a manager review my diminished value claim, which was denied. I have professional documentation that I believe was overlooked.”

- Mention your proof: “My claim is supported by a certified appraisal from SnapClaim, which uses local market data to show the exact loss in value.”

- Make your request: “Could you please personally review my appraisal report? I’m confident the evidence supports my claim.”

File a Complaint with Your State’s Department of Insurance

If the manager doesn’t resolve the issue, your next step is to file a complaint with your state’s Department of Insurance (DOI). This is a powerful, free tool for consumers. The DOI will launch a formal investigation and require State Farm to provide a written explanation for their denial. Insurers often become much more reasonable when a government regulator gets involved.

You can find your state’s DOI on the National Association of Insurance Commissioners (NAIC) website.

Consider Small Claims Court

As a last resort, you can take your case to small claims court. The process is designed to be straightforward and doesn’t typically require a lawyer. Your SnapClaim appraisal report serves as expert evidence, clearly showing the judge your financial damages. It transforms the case from your opinion versus theirs into a matter of documented facts.

Frequently Asked Questions (FAQ)

Can I claim diminished value if the accident wasn’t my fault?

Yes, absolutely. A diminished value claim is specifically for situations where another driver was at fault. You are filing a third-party claim against their insurance policy (in this case, State Farm) to be compensated for the loss in your vehicle’s resale value caused by their insured’s negligence.

How much does diminished value typically pay?

Payouts vary widely based on the vehicle’s value, the severity of the damage, and state laws. While some claims are a few hundred dollars, others can be several thousand. A professional appraisal is the only way to determine the specific loss for your vehicle. SnapClaim’s Money-Back Guarantee ensures you have nothing to lose: if your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee.

How long do I have to file a diminished value claim?

This is determined by your state’s statute of limitations for property damage, which is typically two to three years from the date of the accident. However, it is always best to file as soon as your vehicle’s repairs are complete to create a clear link between the accident and your car’s lower market value. You can find the deadline for your area in our state-by-state diminished value law guides.

Will filing a diminished value claim make my insurance rates go up?

No. Because you are filing a third-party claim against the at-fault driver’s State Farm policy, it has no impact on your own insurance premiums. The claim is attached to their driving record, not yours.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes. Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step. Get your free estimate today or order a certified appraisal report to strengthen your insurance claim.