Has your car been in an accident that wasn’t your fault? You may be surprised to learn that even after perfect repairs, your vehicle has lost value—and getting fair compensation from the at-fault driver’s insurer, like State Farm, requires a solid plan. While State Farm is legally required to consider your claim, their process is designed to minimize their payout, not maximize your recovery.

Successfully filing a diminished value State Farm claim hinges on providing your own independent proof of loss, and this guide will show you how to do it.

Understanding a Diminished Value Claim with State Farm

When State Farm pays to repair your car, they have only covered part of your financial loss. They fixed the physical damage, but they haven’t restored its market value. An accident history creates a permanent stigma attached to your vehicle’s VIN, meaning it will now sell for less than an identical car with a clean record.

That loss in resale value is called diminished value, and you have a right to be compensated for it. If this is a new concept, our guide on what a diminished value claim is is a great place to start.

Filing a diminished value claim with State Farm is about making them cover the entire loss you suffered—not just the body shop bill. The challenge is proving exactly how much value your vehicle has lost.

The Mabry v. State Farm Ruling You Should Know

State Farm’s obligation to pay for diminished value is not just a matter of fairness; it’s a legal precedent. A landmark Georgia Supreme Court case, Mabry v. State Farm, fundamentally changed how these claims are handled. In 2001, the court ruled that the loss in a vehicle’s market value due to its accident history is a real, recoverable damage, even if the repairs are perfect.

This decision forced State Farm to pay an estimated $150 million in settlements and establish a formal process for these claims. You can find more details on this important case from legal resources like mwl-law.com.

Despite this history, many adjusters still rely on standardized, insurer-friendly formulas like “Rule 17c” to generate a low initial offer. This one-size-fits-all approach often ignores the factors that actually determine your car’s value, such as:

- The severity of the structural damage

- Local market demand for your specific model

- Your vehicle’s make, model, trim, and unique options

Knowing this history gives you an advantage. It confirms your right to file a claim and prepares you for their likely tactics. Your goal is to counter their flawed formula with undeniable, market-based evidence.

How to Build Evidence for Your State Farm Claim

Before you begin negotiating a diminished value State Farm settlement, you need to build your case with solid proof. A successful claim isn’t based on what you feel your car has lost in value—it’s built on clear, organized evidence.

Think of it as creating a case file. Every document you add strengthens your position and makes it harder for an adjuster to dismiss your claim. For those seeking help organizing their evidence without high legal fees, using affordable paralegal services can be a smart way to get everything in order.

Your Essential Document Checklist

A disorganized stack of papers won’t be persuasive. You need a clean, professional evidence file that shows the adjuster you are serious about your claim.

Here’s what you must include:

- Official Police Report: This document establishes the facts of the accident, including who was determined to be at fault.

- Final Repair Invoice: This provides a detailed list of every part that was repaired or replaced, proving the collision was significant.

- Pre-Accident Vehicle Photos: If you have photos of your car before the crash, they help prove it was in excellent condition.

- Post-Accident and Repair Photos: Document the damage immediately after the accident and take pictures of the completed repair work to tell the full story.

Key Takeaway: Your mission is to leave no room for doubt. The evidence should clearly show three things: your car was in great shape, the accident was significant, and its market value has suffered as a result.

The single most powerful piece of evidence you can have is a professional, independent appraisal. A certified report from SnapClaim transforms your request into a data-driven demand. It calculates the exact car value after accident stigma using real, local market data—providing the proof you need to negotiate effectively. You can learn more with our guide on how to claim diminished value.

How to Write a Demand Letter That Gets Results

Your demand letter is the official start of your negotiation with State Farm. This isn’t just an email—it’s the formal presentation of your case. A well-written letter signals to the adjuster that you are serious and have a well-documented diminished value State Farm claim.

The goal is to build a logical argument that is difficult to dismiss. Avoid emotional language about the accident or your frustration. Keep it professional and stick to the facts: the at-fault accident occurred, the repairs were substantial, and your vehicle’s market value has dropped as a direct result.

Key Components of a Strong Demand Letter

To be effective, your letter must be clear, concise, and contain specific information. You are essentially creating a summary of your evidence file.

Ensure your letter includes these elements:

- Your Information and Claim Number: At the top, list your full name, address, phone number, and the State Farm claim number for easy reference.

- A Brief Accident Summary: A single sentence is all you need. State the accident date, the at-fault party, and your vehicle’s make, model, year, and VIN.

- The Specific Demand Amount: Clearly state the exact dollar amount you are demanding for your vehicle’s diminished value. This number should come directly from your certified appraisal report.

- Reference to Your Appraisal: Explicitly mention that your demand is based on a professional, independent appraisal and attach a full copy of the report.

Pro Tip: Never send a demand letter without a certified appraisal attached. The letter makes the request, but the appraisal provides the proof. Without it, your demand is just an opinion, and opinions are easy for adjusters to ignore.

Conclude the letter by stating that you expect a response within a reasonable timeframe, such as 15 business days. This sets a professional tone and helps keep the process moving forward.

Negotiating With the State Farm Adjuster Like a Pro

After you send your demand letter, a State Farm adjuster will likely call you. Their first offer will almost certainly be low—this is a standard tactic to test whether you will accept a small payout.

Your job is to remain calm, professional, and focused on the facts. The adjuster’s goal is to close your claim quickly and for the lowest possible amount. Your goal is to be compensated fairly for your vehicle’s lost value. When the conversation strays, bring it back to the data in your certified appraisal report.

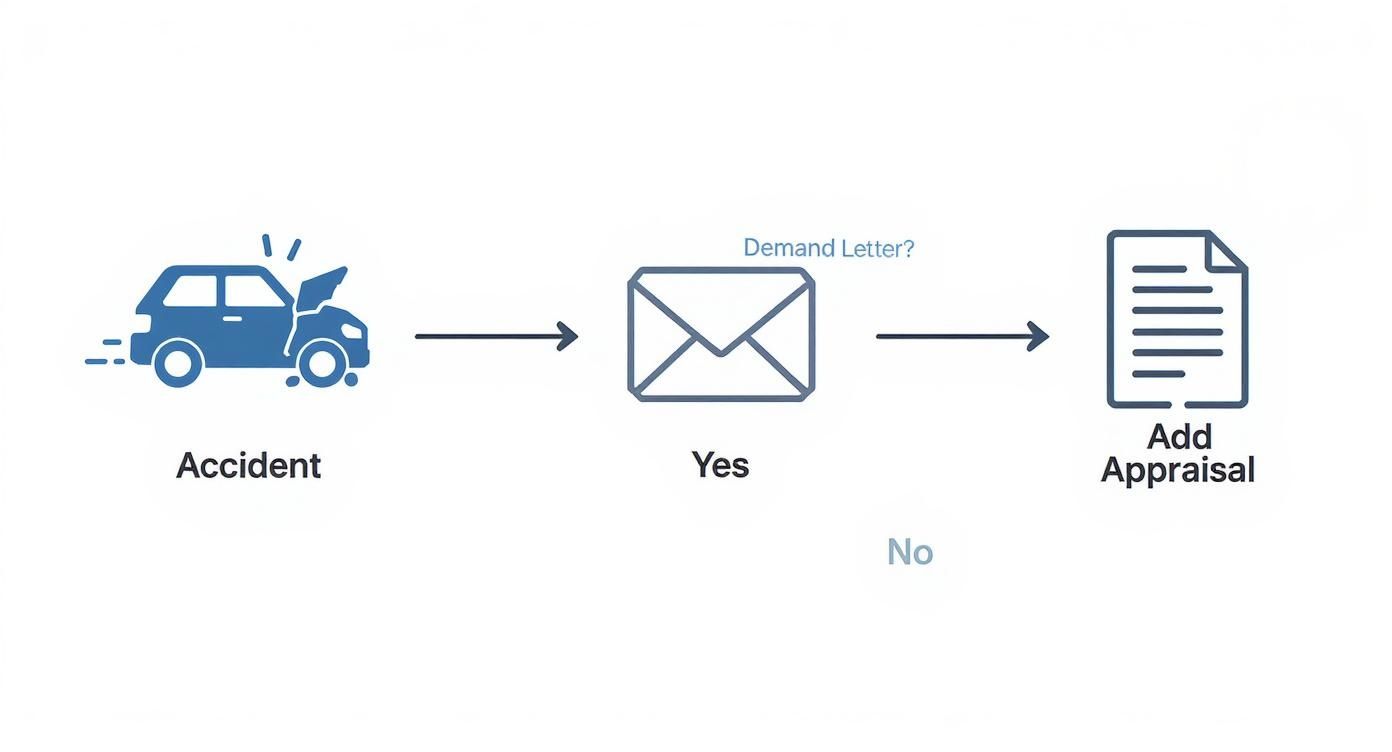

This process map shows the path to a successful claim. Notice that a professional appraisal is the engine that drives the entire process.

As you can see, without objective proof, your claim has little chance of success.

Countering Common Objections

The adjuster is trained for these conversations and will use common objections. Your best defense is to challenge them to provide market-based evidence that supports their low offer.

Here are common tactics and how you can respond effectively.

| Common State Farm Objections and Your Responses |

| :— | :— |

| State Farm’s Objection | Your Data-Backed Response |

| “Our internal 17c formula is the industry standard for this calculation.” | “Can you please provide me with comparable sold vehicles from my local market that support your valuation?” |

| “We disagree with your appraisal report’s conclusion.” | “My appraisal was conducted by a certified expert using real-time market data. Does your valuation use similar, verifiable data?” |

| “The repairs were done perfectly, so the car has been made whole.” | “The repairs addressed the physical damage, but they did not erase the accident from the vehicle’s history report, which is what impacts its market value.” |

| “We don’t pay for diminished value in this state.” | “My research indicates that [Your State] law requires the at-fault party’s insurer to compensate for loss of market value. Are you denying my claim based on a specific statute?” |

Your responses should always circle back to verifiable market data—the same data your SnapClaim report is built on.

The Bottom Line: Persistence is key. A diminished value State Farm negotiation is rarely a single conversation. Stay patient, polite, and keep referencing the proof in your appraisal.

Fortunately, precedents in some states support your claim. In Georgia, for instance, State Farm accepts a high percentage of diminished value claims, with average payouts between $2,600 and $6,900, largely due to the Mabry v. State Farm ruling.

Why an Independent Appraisal Is Your Secret Weapon

When you file a diminished value State Farm claim, you are entering a negotiation where you and the insurer have different goals. The adjuster wants to close your claim for the lowest amount possible. You want to be paid fairly for the financial loss you’ve incurred.

An independent appraisal is the tool that cuts through opinions and replaces them with facts, shifting the negotiation in your favor.

Moving Beyond Insurer Formulas

State Farm adjusters are trained to use internal formulas, like the 17c formula, which consistently produce low offers. A certified appraisal report from SnapClaim is different.

Our reports are built on real-time, local market data. We analyze what comparable vehicles are actually selling for in your area to determine your car’s true loss in value. An insurer’s generic estimate will never match this level of detail.

A certified appraiser also inspects the quality of the repairs, spotting subtle imperfections an untrained eye might miss—like paint mismatches or inconsistent panel gaps. They understand what paint correction involves and can identify when a repair isn’t up to factory standards, all of which contributes to your car’s diminished value.

This isn’t just a second opinion; it’s the leverage you need to dismantle low offers and negotiate from a position of strength.

Presenting the adjuster with objective, third-party proof forces them to defend their low number with actual market data—something their internal formulas can’t do. When you’re ready, finding a certified diminished value appraiser near you is a simple next step.

Best of all, you can get this powerful evidence without financial risk. With SnapClaim’s Money-Back Guarantee, if your insurance recovery from the claim is less than $1,000, we refund the full appraisal fee.

FAQ: Common Diminished Value State Farm Questions

Navigating a claim with a large insurer like State Farm can be daunting. Here are answers to some of the most common questions about the process.

Can I claim diminished value if the accident was my fault?

Generally, you cannot file a diminished value claim with your own insurance company (a “first-party” claim) if you caused the accident. Diminished value is designed to be paid by the at-fault driver’s insurance. If another driver hit you and they are insured by State Farm, you file the claim against their policy.

Does State Farm have to pay diminished value?

Yes. In states that recognize diminished value, State Farm is legally required to compensate you for your car’s lost market value if their insured driver was at fault. However, they often use internal formulas designed to minimize payouts, which is why your own independent evidence is so critical.

This isn’t just speculation. In a 2023 class-action lawsuit, State Farm settled for $2.09 million after being accused of systematically underpaying these exact claims. You can read more about this case and similar insurer issues to better understand what you are facing.

How long do I have to file a diminished value claim?

Your window to file a claim is based on your state’s statute of limitations for property damage, which is typically between two to five years from the accident date. It is always best to start the process as soon as your vehicle repairs are complete to avoid having your claim denied on a technicality.

What if State Farm denies my claim or makes a low offer?

A denial or a low offer is a standard negotiation tactic, not a final decision. Don’t be discouraged. This is the moment your independent appraisal report becomes your most powerful tool.

If State Farm pushes back, respond professionally by resubmitting your certified appraisal and asking them to provide their own detailed, market-based evidence to justify their position. This simple step places the burden of proof back on them.

Persistence backed by solid data is what wins these claims. And with SnapClaim’s Money-Back Guarantee, you have nothing to lose. If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee — guaranteed.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes. Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step. Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.