Has an insurance adjuster handed you a CCC report after a car accident? This document is the official blueprint your insurer uses to calculate repair costs or, in some cases, declare your vehicle a total loss. Understanding this report is the first step toward taking control of your claim and ensuring you receive the compensation you deserve.

Think of it as the insurance company’s playbook. Generated by software from CCC Intelligent Solutions, it details every part, labor hour, and paint material needed for the repair. Getting a handle on this document is crucial for making sure your settlement is fair.

Decoding the Insurer’s Blueprint

After an accident, an insurance adjuster’s primary goal is often to close your claim quickly and for the lowest possible cost. Their main tool for this is the CCC report. This standardized estimate, used by over 300 major auto insurers, serves as the starting point for all negotiations.

While it may look like a simple list of car parts, this report is the foundation for your entire claim. The numbers on this document determine if your car gets fixed, the quality of parts used, and the initial offer you’ll receive if it’s deemed a total loss.

Why This Report Is So Important

The CCC report has significant consequences that extend beyond the initial repair estimate. Here’s what this single report controls:

- Repair Scope and Quality: It dictates exactly which parts get repaired or replaced. Insurers often default to cheaper aftermarket or used parts instead of the Original Equipment Manufacturer (OEM) parts your car was built with.

- Total Loss Declaration: If the repair costs on the report exceed a certain percentage of your car’s pre-accident value (a threshold set by state law and your insurer), your vehicle is declared a total loss.

- Initial Settlement Offers: Whether you’re facing a total loss or a diminished value claim, the figures in this report are what the insurer uses to formulate their first lowball offer.

- Diminished Value Proof: The report provides undeniable proof that your vehicle sustained significant damage, which is essential for filing a successful diminished value claim to recover its lost resale value.

The insurer’s CCC report isn’t a neutral, fact-finding document. It’s a financial tool designed to protect their bottom line. Your job is to understand it, question it, and use it as evidence to fight for a fair outcome.

Ultimately, the CCC report is just the insurance company’s opening move. Once you learn to read between the lines, you can identify where they’ve cut corners and counter their offer with solid proof. This is where an independent appraisal from SnapClaim comes in. We help turn their document into your evidence, providing the data needed to secure the full insurance total loss payout or diminished value you are owed.

How to Read and Decode Your CCC Report

At first glance, a CCC report can seem like a confusing wall of codes and industry jargon. That’s because it’s designed for insurers and body shops, not vehicle owners. However, learning to read it is the first step toward taking control of your claim.

Think of it as a detailed blueprint for your vehicle’s repair. Each line item is a specific instruction, and every code represents a part or procedure. Understanding these instructions—and whether they specify quality materials or cheap shortcuts—is critical.

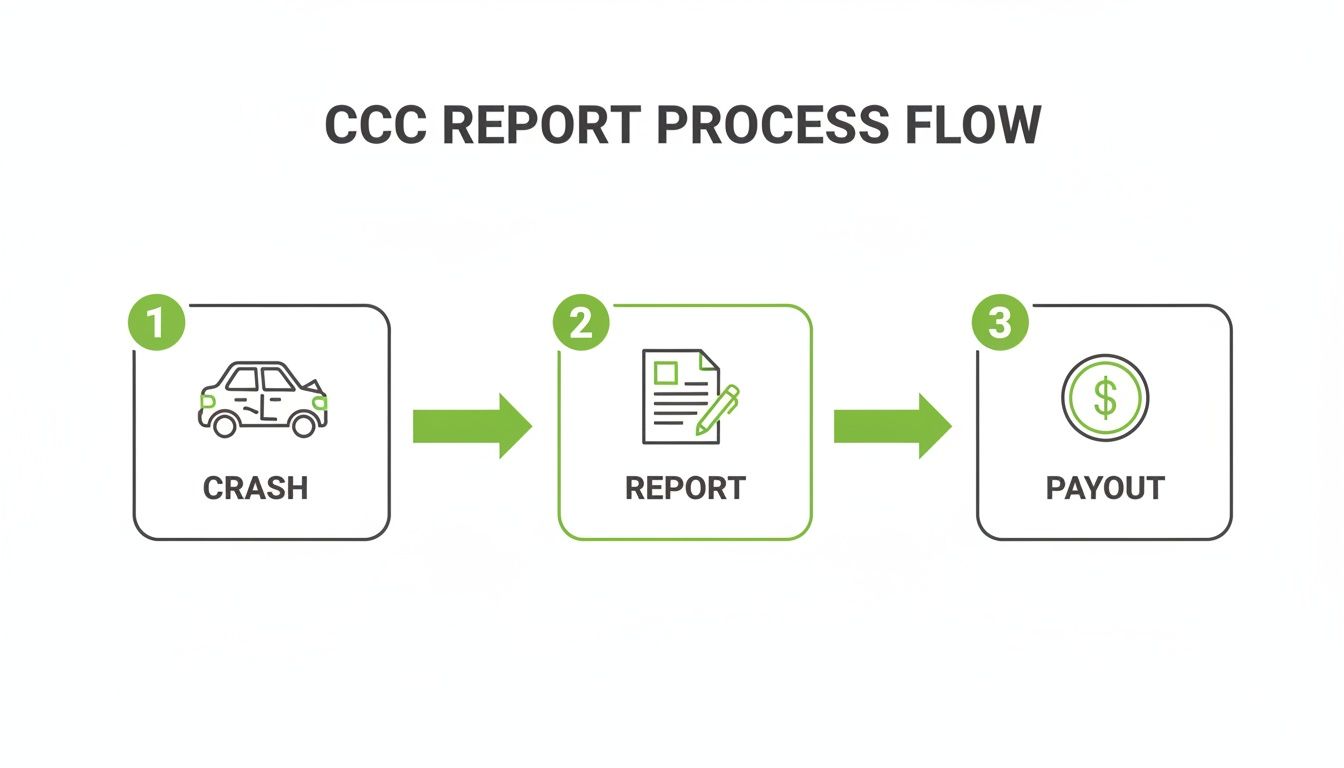

This flowchart illustrates how the CCC report fits into the larger claims process, from the crash to the final insurance payout.

As you can see, the CCC report is the central document that translates physical damage into a dollar amount, directly influencing what the insurance company agrees to pay.

Breaking Down the Key Components

Your CCC report is organized into several key sections. While the layout might vary slightly, the core information is always present.

- Header Information: At the top, you’ll find your claim number, vehicle details (VIN, year, make, model), and the date of loss. Always double-check this for accuracy.

- Estimate Line Items: This is the heart of the report. It’s a detailed, line-by-line list of every part, material, and action needed to fix your vehicle.

- Totals Summary: Located near the bottom, this section adds up the total costs for parts, labor, and paint, giving you the grand total for the repair estimate.

The table below provides a quick guide to the most important sections.

Key Sections of a CCC Report Explained

A quick reference guide to understand the most important parts of your collision repair estimate.

| Section Name | What It Means | What to Look For |

|---|---|---|

| Header | Basic claim and vehicle identification. | Verify your VIN, claim number, and date of loss are correct. Errors here can delay your claim. |

| Estimate Lines | The step-by-step repair plan. | Look for abbreviations like R&I, Repair, and Blend. Pay close attention to part types (OEM, A/M, LKQ). |

| Labor Summary | Breaks down labor hours by type (body, paint, mechanical). | Check the labor rates. Are they in line with reputable shops in your area? Low rates can signal a low-quality repair. |

| Totals Summary | The final calculation of all costs. | This is the bottom-line number the insurer wants to pay. Does it seem too low for the damage your vehicle sustained? |

Understanding these sections is your first line of defense against an insurer trying to cut corners on your repair.

Understanding the Language of Repairs

The line-item section tells the real story—and it’s where insurers often try to save money at your expense. It’s filled with abbreviations, but learning a few key terms will help you understand the proposed repair plan.

Here’s a quick translation of the most common codes:

- R&I (Remove & Install): An undamaged part is temporarily removed to access a damaged area and then reinstalled. The original part is reused.

- Repair: The shop is instructed to fix the existing damaged part rather than replace it.

- Replace: A damaged part will be swapped out. This is where you need to check what kind of part they plan to use.

- Blend: A crucial step where a painter blends new paint onto adjacent panels to ensure a perfect match. Insurers often omit this to save money, which can result in a mismatched, patchy-looking car that screams “repaired.”

A CCC report is more than just a repair list; it’s a permanent record of your vehicle’s accident history. Every line item contributes to the story that future buyers will see, directly impacting your car value after accident.

Part Types: A Critical Detail

The type of parts the insurer authorizes has a massive impact on your vehicle’s safety, reliability, and resale value. The CCC report specifies exactly what kind of parts are approved.

- OEM (Original Equipment Manufacturer): Brand-new parts made by your car’s manufacturer. They are the gold standard, guaranteeing proper fit, performance, and quality.

- A/M (Aftermarket): New parts made by third-party companies. Quality varies widely, from decent to dangerous. They often don’t fit correctly and may not meet original safety standards.

- LKQ (Like Kind and Quality): A term for a used part from a salvage vehicle. While technically an OEM part, it isn’t new, and its history and condition are unknown.

The skills needed to analyze an insurer’s estimate are the same as those for reviewing an independent appraisal. For a deeper dive, check out our guide on how to read an appraisal report. Mastering these documents gives you a significant advantage in negotiations.

The CCC Report’s Role in a Total Loss Claim

When your vehicle is declared a total loss, the process changes entirely. The initial CCC repair estimate is what triggers this decision. If repair costs exceed a certain percentage of your car’s value—a threshold that varies by state—the insurer will write it off.

At that point, the repair estimate is set aside. The focus shifts to a new document: the CCC ONE Market Valuation report. This report is the insurance company’s official calculation of your vehicle’s Actual Cash Value (ACV), or what they claim it was worth right before the accident. This valuation is the single most important factor determining your total loss payout, but it’s also where many vehicle owners are short-changed.

How Insurers Use the CCC Report to Lowball You

The CCC valuation report is supposed to determine your car’s ACV by comparing it to similar vehicles for sale in your local market. The problem is, the “comparable” vehicles are often hand-picked to justify a lower value.

This is a common tactic used to support a lowball settlement offer. Here’s how adjusters can manipulate the numbers:

- Cherry-Picking Comps: They might select vehicles with higher mileage, fewer options, or in worse condition than yours was to drag down the average value.

- Stretching the “Local” Market: If they can’t find cheap enough cars nearby, they may expand the search radius to distant markets where prices are lower, ignoring your car’s true local worth.

- Applying Unfair Adjustments: The report often deducts value with negative “condition adjustments” for minor scratches or normal wear and tear that had little impact on your car’s real-world value.

The final number they present is an opening offer, not a final decision. You have the right to question it and push back with your own evidence.

How to Fight Back Against a Low Total Loss Offer

If the insurance company’s offer feels too low, trust your gut. It probably is. To get a fair payout, you must stop arguing about the old repair estimate and focus entirely on proving your car’s true pre-accident value.

To do this, you need to build a strong counter-argument based on solid proof.

The insurer’s valuation is their opening bid in a negotiation you didn’t ask to be in. To win, you must be prepared with your own independent, data-driven proof of value.

Start by gathering all your vehicle’s paperwork: maintenance records, receipts for recent upgrades like new tires, and proof of any special features. Then, do your own research. Find comparable vehicles for sale in your area that are a true match for your car’s condition, mileage, and options.

An independent appraisal is your most powerful tool. A certified report from SnapClaim analyzes the same market data from an objective, owner-first perspective. It provides the hard evidence needed to challenge the insurer’s comps and supports your claim with a defensible, certified valuation. Learn more about how a fair total loss calculation is performed.

Presenting a professional appraisal changes the negotiation dynamic. You are no longer just a claimant complaining about a low number; you are presenting a fact-based case that the insurer must address. This dramatically improves your chances of recovering the full and fair car value after the accident.

Connecting the CCC Report to Your Diminished Value Claim

Even after flawless repairs from the best body shop, your vehicle’s history is permanently marked. An accident leaves a digital scar on vehicle history reports that every future buyer will see. That scar reduces your car’s resale value, and this financial loss is called diminished value.

The CCC report is the official, undeniable proof that your car was seriously damaged. It is the foundational document you need to launch a successful diminished value claim and recover the money you’ve lost.

From Repair List to Value Loss Evidence

Think of the CCC report as the “what” of your claim. It details what was damaged and what was repaired, but it completely ignores how much value your car has lost as a result.

That’s where an independent appraisal comes in. Your CCC report becomes the primary piece of evidence an appraiser uses to build your case. Since it’s the insurer’s own document, it becomes nearly impossible for them to dispute the severity of the damage listed in black and white.

Identifying High-Impact Repairs on the CCC Report

Not all repairs are equal when it comes to resale value. A replaced bumper cover may have a minor impact, but certain line items on a CCC report are major red flags to buyers and cause a significant drop in market price. When reviewing the report, look for these key indicators of major diminished value:

- Structural or Frame Damage: Any mention of repairs to the frame, unibody, or structural components is the single biggest driver of diminished value.

- Airbag Deployment: Deployed airbags instantly signal a serious accident to any potential buyer and can be associated with a value loss of 20% to 40%.

- Welded Panel Replacement: If the report lists replacements for “weld-on” parts like quarter panels or pillars, it indicates the damage was too extensive for simple repairs.

- Extensive Labor Hours: A high number of total labor hours clearly illustrates the complexity and severity of the repairs.

These entries are your proof that the accident was not a minor fender-bender. They are specific details that directly translate into a lower car value after an accident.

Your CCC report is the starting point, not the destination. It documents the damage, but it takes an expert appraisal to translate that damage into a specific, defensible dollar amount for your diminished value claim.

Bridging the Gap with a Certified Appraisal

Insurance companies will not volunteer to pay for your car’s diminished value. In fact, they will likely deny it even exists. To receive fair compensation, you must prove your financial loss with credible, third-party documentation.

A certified appraisal is critical for this. An expert appraiser takes the technical repair data from the CCC report and combines it with real-world market analysis. They calculate the precise difference in what a buyer would pay for your repaired vehicle compared to an undamaged one. This process transforms the insurer’s repair sheet into your most powerful negotiation tool.

SnapClaim’s certified appraisal reports provide the data-backed proof you need to build a rock-solid diminished value claim. We analyze the insurer’s own CCC report to create a defensible valuation that strengthens your case for fair compensation. To learn more about this process, explore our complete Diminished Value Guide.

Common CCC Report Inaccuracies and Insurer Tactics

Insurance companies are businesses focused on controlling costs. While a CCC report appears objective, it’s often the first tool an insurer uses to minimize what they pay on a claim.

Think of the initial CCC report as the insurer’s opening offer—one that almost always favors their bottom line. Knowing what red flags to look for is the first step toward protecting your vehicle’s value and fighting for a fair, safe repair.

Underestimating Labor Times and Rates

One of the easiest ways for an insurer to reduce an estimate is by short-changing labor costs. The CCC ONE software provides standard labor times, but these are often bare-minimums that don’t account for real-world complexities.

An insurer might approve a labor time that is too short for a proper repair or use a lower-than-average hourly rate that isn’t competitive with what reputable, certified shops in your area charge.

The Problem with Aftermarket and Used Parts

Specifying non-OEM parts is the most common cost-cutting tactic. Your car was built with high-quality OEM parts, but the insurer’s initial CCC report will likely default to cheaper alternatives.

- Aftermarket (A/M) Parts: These are generic copies from third-party companies. Their fit, finish, and safety standards can be inconsistent, potentially compromising your vehicle’s structural integrity.

- Like Kind and Quality (LKQ) Parts: This is just jargon for used parts from a salvage yard. You have no way of knowing their history—were they from a flood-damaged car? Do they have hidden stress fractures? It’s a gamble.

Using these parts not only impacts safety but also directly lowers your car value after an accident. Future buyers will spot non-original components and devalue your car accordingly. You can check with a reputable source like your state’s Department of Motor Vehicles (DMV) for regulations on non-OEM part usage.

Omissions That Compromise Safety and Quality

Sometimes, what an insurer leaves out of a CCC report is just as damaging as what they put in. These omissions are often strategic decisions designed to save money at the expense of your safety and vehicle’s value.

The most dangerous inaccuracies in a CCC report are not just the lowball numbers, but the missing procedures. Omitting a critical safety scan or a proper paint blend doesn’t just devalue your car—it can put you at risk.

Commonly omitted procedures include:

- Pre- and Post-Repair Diagnostic Scans: Modern cars are filled with sensors for safety systems. A scan is the only way to confirm these systems are recalibrated and functioning correctly after a repair, but insurers often resist paying for it.

- Paint Blending: To achieve a perfect color match, a body shop must blend new paint onto adjacent panels. Insurers frequently refuse this step to save money, leaving you with a patchwork repair.

- One-Time Use Hardware: Many manufacturers require certain bolts and clips to be replaced after removal. Reusing them can compromise structural safety, yet insurers often fail to include these necessary parts.

Here’s a quick breakdown of insurer tactics versus fair repair practices.

CCC Report Red Flags vs. Fair Practices

| Red Flag (Insurer Tactic) | What a Fair Report Includes | Impact on Your Claim |

|---|---|---|

| Using Aftermarket (A/M) Parts | Specifies Original Equipment Manufacturer (OEM) parts to maintain safety, fit, and value. | Non-OEM parts devalue your car and may compromise its structural integrity and safety systems. |

| Lowball Labor Rates | Reflects the prevailing competitive rates for certified body shops in your geographic area. | Unfair rates force good shops to refuse the work or cut corners, leading to a subpar repair. |

| Omitting Diagnostic Scans | Includes both pre- and post-repair scans to ensure all vehicle safety systems are recalibrated and working. | Missing a scan can leave critical safety features like collision avoidance or airbags disabled without warning. |

| No “Blend” Time for Paint | Adds labor time for blending new paint into adjacent panels for a seamless, undetectable color match. | Skipping this step results in a visible mismatch that tanks your car’s resale value. |

| Ignoring One-Time Use Parts | Lists all manufacturer-required one-time use bolts, clips, and fasteners for replacement. | Reusing old hardware can compromise the structural integrity of the repair, creating a safety hazard. |

The initial CCC report is just the start of the conversation. Armed with this knowledge and professional support, you can challenge their lowball estimate and fight for a fair outcome.

Turn Their Report into Your Evidence

The CCC report may be written by the insurance company, but it doesn’t have to be their weapon. With the right strategy, you can turn that document into your best piece of evidence for a fair payout. This is where you shift from defense to offense.

It begins by treating the CCC report as the undisputed foundation of your claim. A certified appraiser uses the damages listed as an admission from the insurer about the accident’s severity. That admission is the bedrock of your case.

From Repair Data to Financial Loss

So how do you connect a list of broken parts to your actual financial loss? A certified appraisal report does just that. An expert appraiser translates the technical jargon from the CCC report into a specific, defensible dollar amount for your diminished value claim or to fight a low insurance total loss payout.

The insurer’s report details the physical damage to your car. An independent appraisal calculates the financial damage to your wallet. It’s the crucial second step they hope you never take.

This isn’t guesswork; it’s a meticulous process. An appraiser focuses on high-impact repairs like structural work or airbag deployment—all detailed in the CCC document—and cross-references them with real-world market data. The final valuation proves exactly how much the car value after accident has dropped.

With a SnapClaim appraisal, you are no longer just complaining about a low offer—you are presenting a data-backed counter-offer. This professional documentation is exactly what you need to negotiate effectively or invoke your policy’s appraisal clause.

You can take this step with confidence. If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee—guaranteed.

FAQs About the CCC Report

Navigating an insurance claim can be confusing. Here are answers to some of the most common questions about the CCC report.

Can I get a copy of the CCC report from my insurer?

Yes, you are legally entitled to a copy of any repair estimate written for your vehicle. If the insurance adjuster has inspected your car, they must provide you with their CCC report. If you don’t receive it automatically, send a polite but firm request via email to create a paper trail.

What if my body shop’s estimate is higher than the insurer’s?

This is very common and expected. The insurer’s initial CCC report is often a preliminary estimate that may overlook hidden damage. A reputable body shop will conduct a thorough inspection and submit a “supplemental claim” to cover any additional necessary repairs. Your role is to ensure all required repairs for a safe and complete restoration are approved.

Can I claim diminished value if the accident wasn’t my fault?

In most states, yes. If the other driver was at fault, you can file a diminished value claim against their insurance policy to recover the loss in your vehicle’s resale value. The CCC report from the claim serves as key evidence of the damages sustained. SnapClaim can help you navigate the process for your specific state.

How does a CCC report prove my diminished value claim?

The CCC report is the insurer’s own documentation of the accident’s severity. It lists every repaired and replaced part, including high-impact items like frame damage or airbag deployment. This official record proves the vehicle has a significant accident history, which is the basis for its diminished value. A certified appraiser then uses this report to calculate the exact financial loss.

Conclusion: Take Control of Your Claim

The CCC report is more than just a piece of paper; it’s the key to unlocking a fair settlement for your vehicle. By understanding what it says, identifying potential inaccuracies, and using it as evidence, you can challenge lowball offers and ensure you are properly compensated for both repairs and lost value. Don’t let the insurance company dictate the outcome.

Get your free estimate today or order a certified appraisal report to strengthen your insurance claim.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes. Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step.

Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.