When your insurance company declares your car a total loss, the next document you’ll likely receive is a valuation report generated by a system called Mitchell. It’s important to see this report for what it is: the insurer’s opening offer, not the final word on what you’re owed.

This automated assessment is designed to quickly calculate your vehicle’s pre-accident value, known as Actual Cash Value (ACV). However, its speed and convenience often come at your expense. Understanding how to challenge a Mitchell total loss report is the first step toward securing a fair settlement.

Your First Look at a Mitchell Total Loss Report

Receiving a Mitchell total loss report can be intimidating, but it helps to know what it is—and what it isn’t. Insurance companies use systems like Mitchell to streamline their workflow and process the high volume of claims they handle daily. This is part of a larger industry trend toward automated claims processing.

The problem is that this efficiency often sacrifices accuracy, leaving you with a lowball offer.

Why the Initial Offer Is Just a Starting Point

The primary flaw in a Mitchell report is its one-size-fits-all approach. The software pulls data from a vast database of vehicle listings to determine a value, but in the process, it frequently overlooks the unique details that made your car more valuable.

The entire system is designed for the insurance company’s benefit, not yours. It prioritizes speed and consistency for the insurer over a true, individualized valuation for you. This is why the initial insurance total loss payout offer rarely reflects the details that matter most:

- Recent upgrades: Did you recently install new tires or an upgraded audio system?

- Exceptional condition: Was your car garage-kept with a perfect maintenance history?

- Special packages: Did it have a desirable trim level or factory options package?

- Local market demand: Is your specific make and model in high demand in your area?

Automated systems like Mitchell and the CCC One Market Valuation Report are built to generate a baseline value, not a detailed market analysis. That’s why you should never treat the report as a final verdict. Instead, view it as the beginning of a negotiation—one where you need to arrive with your own proof.

How Mitchell Determines Your Car’s Value

So, what happens behind the scenes when a Mitchell report is generated? The software operates on a simple principle: it scans dealership listings for vehicles it considers “comparable” to yours, averages their prices to set a baseline, and then applies a few adjustments.

This process is like a real estate appraiser valuing your custom home by only looking at standard tract houses in another town. A Mitchell total loss valuation is often just as inaccurate because the system is built on a foundation of flawed data and questionable comparisons.

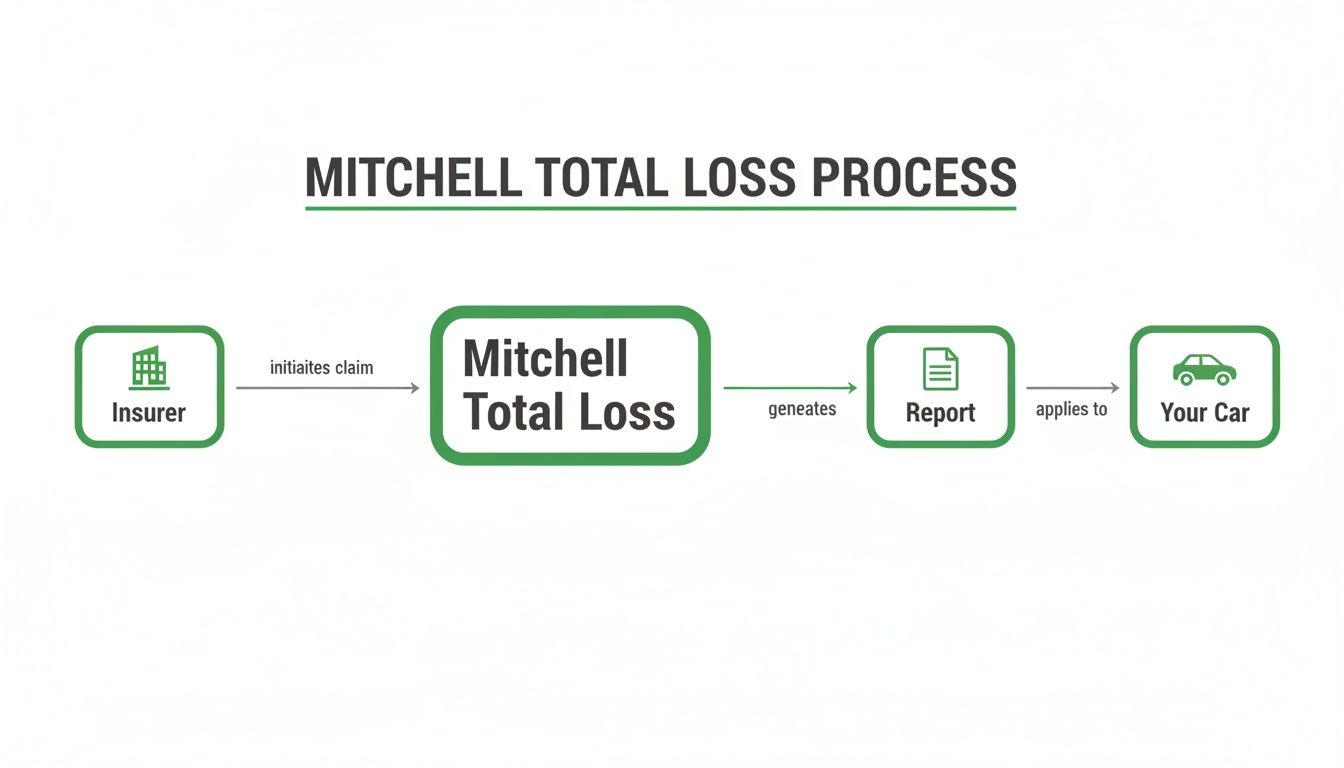

This flow chart provides a simplified view of how the process works, from the insurer’s request to the final report.

The system is designed for speed, but in its rush to standardize, it almost always fails to capture a vehicle’s true, individual market value.

Where the Automated Process Fails

The biggest issue comes down to the word “comparable.” An automated system struggles with nuance, frequently making poor matches that lead to a lower insurance total loss payout for you.

Here are the most common errors found in Mitchell reports:

- Wrong Trim Levels: The system may compare your fully-loaded, top-tier model to a basic, entry-level version, instantly dragging down its value.

- Geographic Mismatches: It might pull comparable vehicles from a completely different, cheaper market—sometimes hundreds of miles away—ignoring what cars like yours actually sell for locally.

- Poor Condition Matches: The “comparable” cars often have higher mileage or a history of accidents, which unfairly lowers the baseline value used for your well-maintained vehicle.

These aren’t minor mistakes; they can easily add up to thousands of dollars. The system is quick to deduct for mileage but often “forgets” to add value for premium features or excellent condition. With total loss declarations on the rise, this problem is more critical than ever. As you can read in this report on record total loss frequency, these lowball offers can leave drivers significantly underpaid.

Finding the Flaws in Your Valuation Report

When a Mitchell total loss report arrives, remember that it’s not a final judgment—it’s an opening offer. Your task is to act like a detective and examine every line item. These reports are often filled with errors that lead to undervalued settlements.

Don’t be intimidated by the official format. The mistakes that cost you money are usually hidden in plain sight. Once you know where to look, you can build a strong case to challenge their numbers. If you need help accessing the details, a guide on how to extract PDF data can be useful.

Scrutinize the Vehicle Options

The first place to check is the vehicle options and packages. Automated systems often get this wrong, defaulting to the base model and ignoring thousands of dollars in factory upgrades.

- Missing Features: Did your car have a sunroof, leather seats, a premium sound system, or an advanced safety package? Ensure every option is listed and valued.

- Incorrect Trim Level: This is a major error. The report must list the exact trim (e.g., LX vs. EX-L), as a higher trim can dramatically increase the car value after accident.

These details represent a significant portion of your vehicle’s worth. Highlighting these omissions is often the quickest way to prove the report is wrong. For a deeper dive, see our guide on how to read an appraisal report.

Question Every Condition Adjustment

Next, focus on “condition adjustments.” This is where insurers often make arbitrary deductions for normal wear and tear. A minor scratch on a five-year-old car should not result in a huge penalty.

A common tactic is to deduct for “dealer prep” or “reconditioning.” These are costs a dealership pays to prepare a used car for sale and have nothing to do with your vehicle’s actual cash value before the accident. Be prepared to push back on any adjustment that seems unfair.

Analyze the Comparable Vehicles

Finally, examine the foundation of the report: the “comparable vehicles” or “comps.” If the comps are flawed, the final value is guaranteed to be inaccurate.

Look for these major red flags:

- Geographic Mismatches: Are the comps from a different city or state where cars sell for less? They must be local.

- Feature Mismatches: Do the listed comps lack the premium options and packages your car had?

- Outlier Pricing: Did they include one unusually low-priced vehicle that drags down the average? Insurers often cherry-pick the cheapest examples.

This table shows how a typical Mitchell report compares to a fair appraisal.

Mitchell Report Red Flags vs. Fair Valuation Practices

| Area of Valuation | Common Mitchell Report Issue | What a Fair Appraisal Includes |

|---|---|---|

| Vehicle Trim & Options | Lists the base model, ignoring thousands in upgrades like sunroofs or tech packages. | A line-by-line inventory of every factory option and package, with value added for each. |

| Condition Adjustments | Makes large deductions for minor, normal wear-and-tear (e.g., small scratches). | Adjustments that reflect the vehicle’s actual age and mileage, ignoring trivial imperfections. |

| “Dealer Prep” Fees | Deducts for reconditioning costs that are irrelevant to the vehicle’s pre-accident value. | No deductions for dealer-related costs; value is based on private-party or retail market realities. |

| Comparable Vehicles | Pulls comps from distant, cheaper markets or uses vehicles with fewer features. | Uses recent, local sales of vehicles with the exact same trim, options, and similar mileage. |

| Valuation Method | Averages a few cherry-picked, low-priced comps to justify a lower offer. | A transparent analysis of multiple relevant comps to establish a fair and realistic market value. |

By reviewing these three areas—options, condition, and comps—you can build a powerful, evidence-based argument that the Mitchell total loss valuation is inaccurate and negotiate for the settlement you deserve.

A Step-by-Step Plan to Dispute the Offer

Now that you’ve identified the weaknesses in the Mitchell total loss report, it’s time to build your case and challenge the insurer’s low offer. A calm, professional approach armed with undeniable facts is the most effective strategy.

Follow these steps to prepare and present your counter-argument to the insurance adjuster.

Notify the Insurer and Gather Your Proof

First, inform the insurance company in writing that you dispute their valuation. A simple email stating that you have reviewed the Mitchell total loss report and found it inaccurate is sufficient for now.

Next, gather the evidence to support your counter-offer and prove your vehicle’s true worth.

- List All Errors: Go through the Mitchell report line by line and document every mistake, from missed options to unfair condition adjustments.

- Compile Vehicle History: Collect your service records, receipts for recent purchases like tires or brakes, and the original window sticker if you have it. This paperwork proves the vehicle’s condition and features.

- Find Your Own Comps: Search local online listings (e.g., AutoTrader, Cars.com) for vehicles that are a true match for yours in year, make, model, trim, options, and mileage. Save screenshots as proof.

Present Your Case and Know Your Rights

Once your evidence is organized, contact the adjuster. Frame the conversation around the facts you’ve uncovered, showing them exactly where their report is wrong and using your proof to justify a higher value.

Unfortunately, total loss claims are becoming more common. As this analysis of rising total loss claims explains, the increasing frequency of total loss declarations makes it critical for owners to have accurate valuations.

If the adjuster refuses to negotiate, remember your insurance policy contains an Appraisal Clause. This provision gives you the right to hire your own independent appraiser, forcing a resolution based on facts, not the insurer’s opinion.

Why a Certified Appraisal Is Your Best Weapon

While doing your own research is a great start, a certified appraisal is the most powerful tool for challenging a Mitchell total loss offer. It provides data-driven proof that adjusters, supervisors, and even courts respect.

Presenting a report from a certified professional changes the conversation from a frustrating debate to a fact-based discussion. It signals to the insurance company that you are serious and prepared to defend your vehicle’s true value.

Credibility That Adjusters Cannot Ignore

A SnapClaim report is backed by I-CAR and ASE-certified experts—credentials respected throughout the automotive and insurance industries. An adjuster cannot easily dismiss this level of professional validation.

Unlike a Mitchell total loss report from a generic, automated system, a SnapClaim appraisal provides a detailed analysis:

- Precise Local Market Data: We identify the actual selling prices of truly comparable vehicles in your specific area, not a vague national average.

- Accurate Vehicle Configuration: We account for every option, package, and recent upgrade to ensure nothing is overlooked.

- Certified Methodology: Our transparent process is built to withstand scrutiny in insurance negotiations and legal disputes.

An independent appraisal provides a clear, unbiased assessment of your vehicle’s Actual Cash Value (ACV). It forces the insurer to justify their lowball offer against a professional, market-verified valuation.

A Risk-Free Path to a Fairer Payout

This professional evidence is crucial for maximizing your insurance total loss payout. An independent appraisal strengthens your position to negotiate a higher settlement. You can learn more in our complete guide to getting an independent car appraisal.

We are so confident in our reports that we offer a Money-Back Guarantee: If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee—guaranteed. This makes getting the proof you need a risk-free step toward securing the compensation you rightfully deserve.

FAQ: Your Mitchell Total Loss Report Questions Answered

Dealing with a Mitchell total loss report can be confusing and frustrating. Here are answers to the most common questions we receive from vehicle owners.

Can I reject the insurance company’s first offer?

Yes, absolutely. The insurance company’s initial offer is just a starting point for negotiations. You are not obligated to accept a Mitchell total loss valuation if you believe it is unfair. The most effective way to respond is with solid evidence, including a list of their report’s errors and a certified appraisal that proves your vehicle’s true worth.

What should I do if the adjuster refuses to negotiate?

If an adjuster won’t budge, you can invoke the “Appraisal Clause” in your insurance policy. This contractual right allows you to hire an independent appraiser. Your appraiser and the insurer’s appraiser then work to agree on a fair value. If they can’t, a neutral umpire makes a final, binding decision. A professional appraisal from SnapClaim provides the credible evidence needed for this process.

Is it worth the effort to fight for a higher payout?

In most cases, yes. The difference between an automated valuation and your car’s true market value is often thousands of dollars. Systems like Mitchell are known for missing valuable options and misjudging local market conditions that affect your car value after accident. Investing in a professional appraisal typically pays for itself many times over by helping you get the money needed to buy a comparable replacement vehicle.

How is a SnapClaim appraisal different from a Mitchell report?

A Mitchell report is an automated tool created by an insurance vendor for insurance companies. Its goal is to standardize claims and control costs, often resulting in lower valuations. A SnapClaim appraisal is an independent report prepared by a certified expert for you. Our sole objective is to determine your vehicle’s true fair market value based on its unique condition, features, and local market, giving you the proof you need to negotiate confidently.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes.

Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step.

Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.

👉 Get your Total loss Appraisal Today