That sinking feeling after a crash isn’t just about the crumpled metal—it’s the knowledge that your car, even after perfect repairs, will never be worth what it once was. This hidden financial loss is called diminished value, and you have the right to claim it.

To recover what you’re owed, you need a diminished value appraisal. This certified report is the single most powerful tool for proving your car’s drop in value and getting fair compensation from the at-fault insurance company. This guide explains how to get a diminished value appraisal and use it to strengthen your claim.

Understanding Your Car’s Hidden Loss After an Accident

After a collision, your first thought is getting the car fixed. But once the dents are gone and the paint is new, a bigger problem remains: your car now has an accident on its permanent record. That blemish on its vehicle history report crushes its resale value, a loss known as inherent diminished value.

Think about it from a buyer’s perspective. Given two identical cars, a smart shopper will always choose the one with a clean history over one that’s been in a wreck—unless you knock thousands off the price.

That discount is your financial loss, and the at-fault driver’s insurance company should cover it.

A Real-World Example of Diminished Value

Let’s say you own a newer SUV worth $45,000. Someone rear-ends you, causing $11,000 in damages. The body shop does a fantastic job, and your SUV looks and drives like new. But the accident is now permanently logged on its vehicle history report.

- Pre-Accident Value: $45,000

- Post-Repair Value: $38,500

- Diminished Value Loss: $6,500

A year later, you go to trade it in. The dealer sees the accident on the report and immediately offers you thousands less than an identical, accident-free model. That $6,500 difference is your diminished value—a real, out-of-pocket loss. To dig deeper into how these claims work, it’s helpful to understand the framework of Ontario’s Car Accident Law.

This guide will give you the clear, actionable steps to get a certified diminished value appraisal and the data-backed proof you need to negotiate for the money you’re rightfully owed.

Is a Diminished Value Claim Worth Your Time?

Before getting an appraisal, first figure out if you have a strong case. Not every accident qualifies for a diminished value claim, and knowing where you stand will save you time and energy.

The biggest factor is who was at fault. In most states, you can only file a diminished value claim if another driver was responsible for the crash. This is a “third-party” claim, meaning you’re pursuing their insurance company for your losses, not your own.

The Makings of a Strong Claim

Insurance companies look for specific factors when you file a diminished value claim. Your vehicle is more likely to have a significant loss in value if it checks these boxes:

- It’s a newer model. A one-year-old car will lose more value than a ten-year-old one.

- It has low mileage. Fewer miles means a higher pre-accident value and a bigger drop after a wreck.

- It had a clean history. A car with no prior accidents will take a much bigger hit to its value.

- The damage was serious. Repairs to the frame, unibody, or core support structures cause the highest levels of diminished value.

A claim probably isn’t worth pursuing for an older, high-mileage car with minor cosmetic damage. Get a quick idea of your potential loss by using a free diminished value estimate.

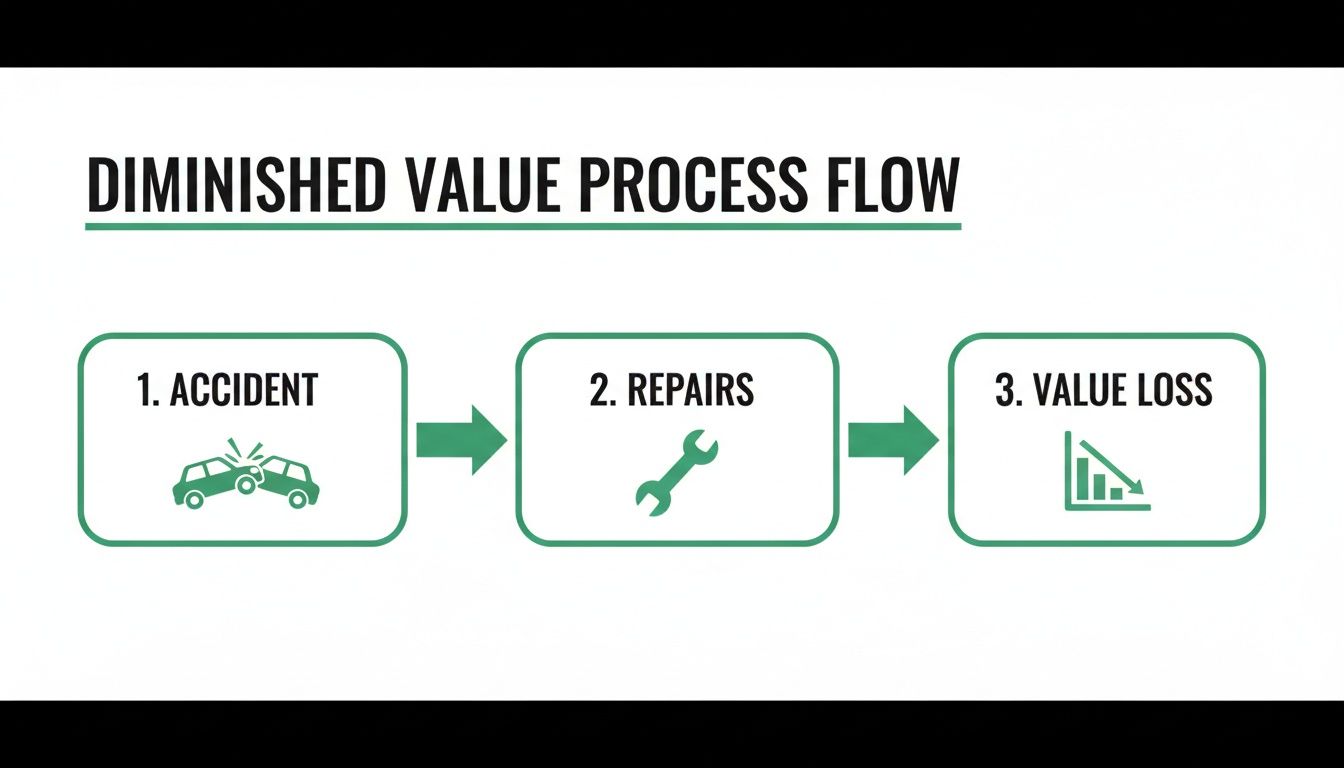

This flowchart shows that even with perfect repairs, an accident history creates a financial loss—and that’s what a diminished value claim is all about.

Why You Can’t Trust the Insurance Company’s Numbers

Many vehicle owners who are owed compensation never pursue a claim because insurers have become very good at shutting them down.

They often use internal formulas, like the notorious “17c method,” which can arbitrarily cap your payout at just 10% of your car’s pre-accident value. These formulas aren’t designed to be fair; they’re designed to save the insurance company money.

Your strongest move is to counter their formula with undeniable proof. A certified, data-driven appraisal from SnapClaim provides the market-based evidence needed to challenge a lowball offer and negotiate for a fair settlement.

How to Get the Proof for Your Diminished Value Appraisal

A powerful appraisal is built on a foundation of solid evidence. Before any appraiser can calculate your car value after an accident, you need to gather the right documents. The more complete your file is, the harder it is for an insurance adjuster to dispute your claim.

Your goal is to arm your appraiser with a complete, undeniable picture of the accident, the repairs, and your vehicle’s history. This allows them to create an accurate, defensible report that proves your financial loss.

Your Essential Documentation Checklist

Start by rounding up the core documents that establish what happened and what was fixed. The more detailed your records are, the stronger your position will be at the negotiation table.

Use this checklist to gather the necessary documents for a strong diminished value claim:

| Document or Evidence | Why It Strengthens Your Claim |

|---|---|

| Official Police/Accident Report | This is non-negotiable. It officially establishes fault, which is the cornerstone of any third-party claim. |

| Insurance Company’s Estimate of Record | This initial assessment shows what the insurer first agreed to cover, serving as a baseline for the scope of the damage. |

| Final, Itemized Repair Invoice | This is the most critical piece of evidence. It details every part replaced and every hour of labor, proving the severity and extent of the repairs. |

| Pre-Accident Vehicle History Report | A clean history from a source like CarFax proves your vehicle had no prior damage, which maximizes its pre-loss value and strengthens your DV argument. |

Getting these four documents is your first and most important step.

Telling the Story with Photos

Paperwork provides facts, but photos provide visual proof that documents can’t match. They show the real-world impact of the collision and help justify the loss in market value in a way that’s instantly understandable.

Make sure you collect:

- “Before” photos of your car to establish its prior condition.

- Clear photos of the damage from multiple angles.

- “After” photos showing the finished repairs from the same angles.

This visual timeline gives your appraiser—and the insurance adjuster—a clear before-and-after comparison. It transforms your claim from numbers on a page into a tangible story of loss.

How to Choose a Credible Diminished Value Appraiser

Not all diminished value appraisals are created equal. Your choice of appraiser can make or break your claim. A strong report is a powerful tool, filled with data-backed proof of your loss. A weak one will be dismissed by an insurance adjuster as “just an opinion.”

The best modern appraisals are built on massive, real-time market data—not just one person’s local experience. This is what makes them so effective.

Traditional Appraisers vs. Modern Platforms

Understanding the difference between the old way and the new way is key. While both have their place, data-driven platforms produce a far more robust and defensible report.

- Local Appraisers: These are professionals who conduct an in-person inspection. While this sounds thorough, their final number is often subjective and based on a limited view of the local market. The process is also slower and more expensive.

- Online Platforms (like SnapClaim): Instead of one person’s opinion, these services analyze huge databases of real-world sales data, auction results, and dealer analytics. This creates an objective, verifiable calculation of your diminished value that is much harder for an insurer to dispute.

It’s data versus opinion. An insurance company can argue with an opinion all day long. It’s much harder for them to argue with thousands of data points proving your financial loss.

Questions to Ask Any Appraiser

Before hiring an appraiser, ask a few sharp questions to determine if their report will be a powerful tool or a waste of money.

Here are the non-negotiable questions to ask:

- What specific market data do you use? A credible appraiser should cite sources like dealer sales data, auction results (like Manheim), and industry valuation guides.

- Are your reports regularly accepted by major insurance carriers? You want a provider with a proven track record with companies like State Farm, Geico, and Allstate.

- Is your methodology compliant with industry standards? The report needs to follow recognized appraisal practices, like the Uniform Standards of Professional Appraisal Practice (USPAP), to hold up under scrutiny.

- How fast can I get my certified report? Modern platforms like SnapClaim deliver a certified, ready-to-go report quickly, often in under an hour.

Finding the best diminished value appraisers comes down to transparency, a data-driven approach, and a history of successful claims.

Negotiating Your Settlement with the Appraisal in Hand

Your certified diminished value appraisal is the starting line for negotiations, not the finish. Now you have data-backed proof to confidently approach the at-fault driver’s insurance company and demand fair compensation. The key is to be professional, persistent, and always point back to the facts in your report.

This is your playbook for turning that appraisal into a check. Here’s how to submit your claim, handle common adjuster pushback, and stand firm on your car’s lost value.

Submitting Your Claim and Appraisal

Your first move is to formally present your case to the insurance adjuster. There’s no need to be emotional; let the data do the talking.

Your submission should include three things:

- A Clear Demand: State the exact dollar amount of diminished value you’re claiming from your appraisal.

- Attached Evidence: Attach the complete appraisal report, the final repair invoice, and the police report.

- A Professional Tone: Keep it firm but polite. You are presenting a documented financial loss.

For example: “Please find attached my certified diminished value appraisal from SnapClaim, which documents a financial loss of $5,800 to my 2023 Honda CR-V. I am formally demanding this amount as compensation for my vehicle’s loss in market value.”

Countering Common Adjuster Tactics

Insurance adjusters are trained negotiators with a playbook of tactics designed to minimize payouts. Expect to hear arguments meant to make you doubt your claim.

Here’s how to counter common lines:

- “Your report is just one person’s opinion.” A SnapClaim report isn’t an “opinion”; it’s a detailed analysis of real-world market data, sales records, and industry valuation guides.

- “We don’t pay for diminished value.” In most states, this is not true. Insurers are generally obligated to make you whole for all losses, which includes diminished value.

- “Our formula shows the loss is only $X.” Politely ask them to provide their valuation in writing. Your independent, third-party appraisal is far superior evidence to their internal formulas.

The most powerful response is to always bring the conversation back to your report. State that your claim is based on certified, market-verified data.

If an insurer refuses to negotiate in good faith, you may need to escalate. One powerful tool is knowing how to invoke the appraisal clause in an insurance policy, which can legally compel them to participate in a binding appraisal process.

Remember, an adjuster’s first offer is rarely their best. Stand your ground and trust your evidence.

Frequently Asked Questions About How to Get a Diminished Value Appraisal

Can I claim diminished value if the accident was my fault?

No, in almost all cases. A diminished value claim is a “third-party” claim filed against the at-fault driver’s insurance. Your own policy covers repairs, not the loss in your car’s market value. The only major exception is Georgia, where first-party diminished value claims are sometimes allowed.What should I do if the insurer ignores my appraisal?No, in almost all cases. A diminished value claim is a “third-party” claim filed against the at-fault driver’s insurance. Your own policy covers repairs, not the loss in your car’s market value. The only major exception is Georgia, where first-party diminished value claims are sometimes allowed.

How much does a diminished value appraisal cost?

Costs vary. A traditional, in-person appraiser can cost $300 to $500 or more and take days. Modern online services like SnapClaim use technology to generate certified reports for a fraction of that price, often in under an hour.

What should I do if the insurer ignores my appraisal?

Don’t get discouraged by this common stall tactic. If the insurer ignores or rejects your appraisal, politely ask for their reasoning and their own valuation in writing. A professional appraisal is backed by verifiable data, making it difficult for them to dismiss without a legitimate reason. If they continue to stonewall, consider filing a complaint with your state’s Department of Insurance.

Is there a time limit for filing a diminished value claim?

Yes. Every state has a legal deadline for filing property damage claims, known as the statute of limitations, which is typically two to three years from the accident date. However, you should file your diminished value claim as soon as your car’s repairs are complete to build the strongest case.

Get the Compensation You Deserve

Navigating a diminished value claim can feel overwhelming, but you don’t have to do it alone. With a certified appraisal from SnapClaim, you get the data-driven proof you need to negotiate confidently and recover the money you are rightfully owed.

We’re so confident in our reports that we offer a Money-Back Guarantee: If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee—guaranteed.

Don’t let the insurance company dictate what your car is worth.

Get your free estimate today or order a certified appraisal report to strengthen your insurance claim.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes. Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low insurance total loss payout or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step. Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.