After an accident, your car is never quite the same. Even with perfect repairs, its resale value takes a permanent hit. This loss is called diminished value in Texas, and the good news is you can recover that money from the at-fault driver’s insurance company.

This guide will break down what diminished value means, your rights under Texas law, and how you can get the compensation you deserve.

How an Accident Tanks Your Car’s Value

Imagine you’re shopping for a used car. You find two identical models, but one has a clean history while the other has an accident on its CARFAX report. Which one would you choose? Most buyers would pick the one with no accident history or expect a steep discount on the other.

Even when a body shop does incredible work, that accident history leaves a permanent mark on the vehicle’s record. It’s a red flag for savvy buyers and dealerships, and it directly translates to a lower market value. This isn’t just a hypothetical problem—it’s real money you lose when it’s time to sell or trade in.

A Real-World Texas Example

Let’s make this simple. Imagine you own a 2022 Toyota Camry in Dallas with a pre-accident value of $25,000. Someone runs a red light and damages your rear bumper. The body shop does a fantastic job, and the car looks brand new.

But now, that Camry has an accident on its permanent record. Because of this, its market value could drop by $7,500—a significant 30% loss. This is what’s known as inherent diminished value, the automatic loss in value that occurs simply because a vehicle was in a documented collision.

This is precisely the money a diminished value claim is designed to recover. It’s not about the quality of the repairs; it’s about making you financially whole for the loss your property suffered.

Key Factors Influencing Your Texas Diminished Value Claim

Several key variables determine how much value your vehicle has lost. Understanding these factors is the first step toward building a strong claim and knowing what you’re owed.

| Factor | Why It Matters in Texas | Example |

|---|---|---|

| Vehicle Age & Mileage | Newer cars with low mileage suffer a much higher percentage loss. | A one-year-old F-150 will lose more value than a seven-year-old one. |

| Pre-Accident Condition | A pristine car takes a bigger hit than one with existing wear and tear. | If your car was already scratched up, the loss won’t be as dramatic. |

| Severity of Damage | Structural or frame damage is a major red flag for buyers. | A fender-bender causes less diminished value than a collision requiring frame straightening. |

| Vehicle Prestige | Luxury and high-end models are expected to have a flawless history. | A collision history on a Porsche will scare off buyers more than on a Kia. |

As you can see, a lot goes into the calculation, which is why you can’t just pick a number out of thin air.

The most effective way to prove your loss is with a professional, independent appraisal. It provides the hard data and expert analysis needed to counter the insurance adjuster’s inevitable lowball offer. A SnapClaim report documents your vehicle’s true loss in value, empowering you to negotiate from a position of strength.

Understanding Your Rights Under Texas Law

Knowing your rights is the first step toward getting paid what you’re owed. In Texas, the law is on your side—it recognizes that even after perfect repairs, your vehicle has lost real market value. This isn’t just about what feels fair; it’s about the compensation you are legally entitled to.

The most important thing to understand is that a diminished value in Texas claim is a “third-party” claim. This means you file it against the at-fault driver’s insurance, not your own. Your policy is designed to cover your repairs, but it almost never pays for the lost resale value.

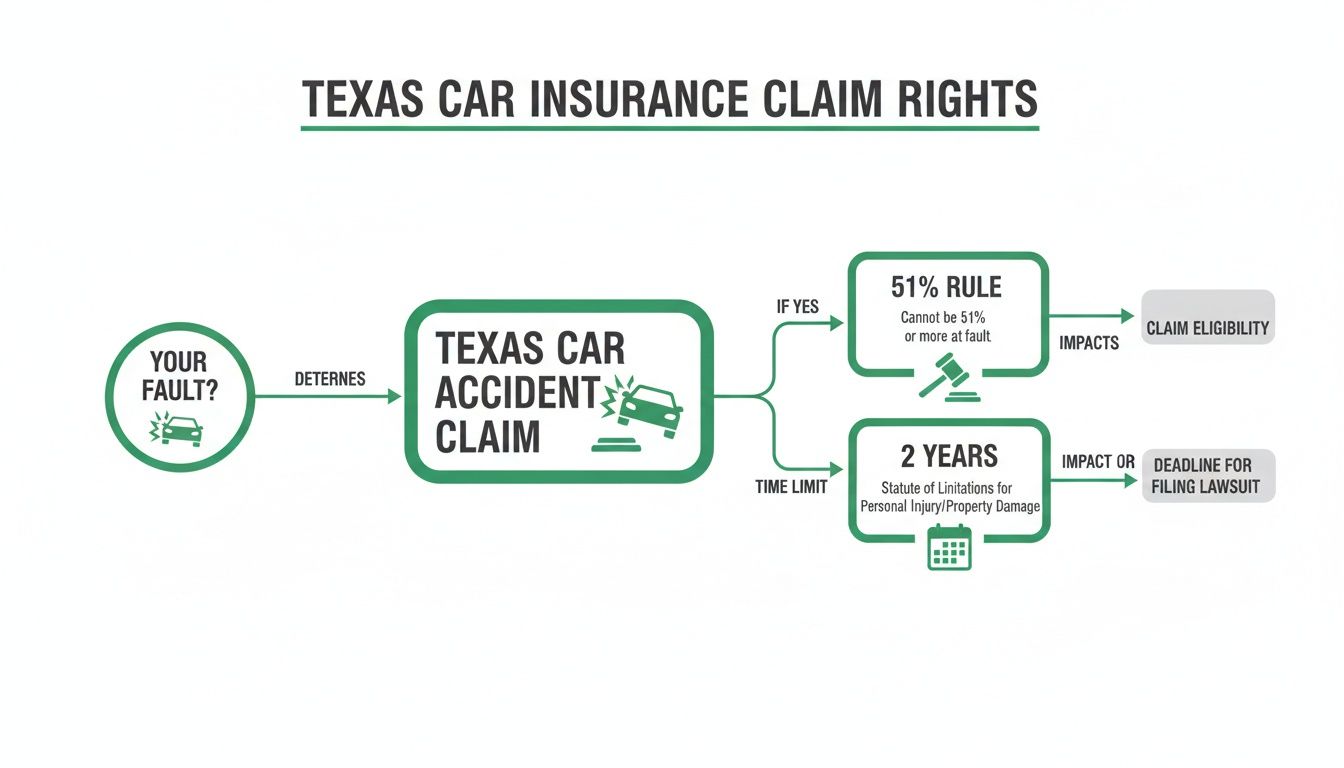

The Critical 51% Fault Rule

Texas operates on a “modified comparative fault” system, which sounds complicated but boils down to one number: 51%. This is often called the 51% Bar Rule, and it’s a critical factor for your claim.

- If you are 50% or less at fault: You can recover damages. The insurance company will simply reduce your payment by your percentage of fault.

- If you are 51% or more at fault: You get nothing.

Insurance companies use this rule to their advantage. An adjuster might try to assign a small portion of the blame to you—say, 10%—to reduce their payout. If they can successfully argue you were 51% responsible, they walk away without paying anything. This is why a clear police report and solid evidence are so important. To learn more about how market value is assessed, you can explore property value insights from Ownwell.com.

Scenario: The 51% Rule in Action

Imagine you’re driving through a green light when someone making a left turn clips your front end. The other driver’s adjuster might claim you were speeding, trying to assign you 20% of the blame.If your total diminished value was $5,000, they’d reduce your payout by your 20% fault, leaving you with a $4,000 settlement. But if they could argue you were distracted, pushing your fault to 51%, your claim would drop to $0.

The Two-Year Countdown: Statute of Limitations

Besides fault, time is also working against you. Texas law gives you a strict two-year deadline from the date of the accident to file a lawsuit for property damage, which includes diminished value. This is called the statute of limitations.

While you’ll likely file your claim long before considering a lawsuit, that two-year clock is always ticking. Insurance companies know this deadline well. If you delay, they might drag out the process, hoping time runs out. Once it does, they are no longer legally obligated to pay.

That’s why it’s best to act quickly. The ideal time to start your diminished value in Texas claim is right after your vehicle’s repairs are complete. This gives you plenty of time to gather evidence, submit the claim, and negotiate a fair settlement without a legal deadline looming.

The Three Types of Diminished Value Explained

When you file for diminished value in Texas, you are demanding compensation for a real, measurable financial loss. Understanding how your vehicle has lost value is key to building a strong claim and recovering every dollar you’re owed.

“Diminished value” is an umbrella term for three different kinds of loss. While your claim will likely focus on one or two, knowing the difference is crucial for communicating with the at-fault driver’s insurance company.

Inherent Diminished Value: The Most Common Claim

This is the most common type of claim. Inherent Diminished Value is the automatic loss in your car’s market value simply because it now has an accident on its record. Even if a top-tier shop performs flawless repairs, the vehicle history report now has a permanent black mark that deters future buyers.

Think of it this way: a buyer is looking at two identical Ford F-150s. One has a clean history. Yours has a documented collision. The clean one will always command a higher price. That price gap is your truck’s inherent diminished value.

Repair-Related Diminished Value

Sometimes, the repairs themselves are the problem. Repair-Related Diminished Value occurs when shoddy workmanship makes your car worth even less, compounding the inherent loss.

This flowchart breaks down the critical checkpoints for any Texas car accident claim, from proving fault to meeting deadlines.

As you can see, Texas law is specific. Understanding fault assessment and the strict timelines is essential for a successful claim.

Poor-quality repairs create a second layer of value loss. Common examples include:

- Mismatched paint color that is obvious in sunlight.

- Cheap, aftermarket parts used instead of factory-grade Original Equipment Manufacturer (OEM) parts.

- Uneven gaps in the body panels.

- Lingering mechanical issues that appeared after the repair work.

These flaws are tangible proof that your vehicle wasn’t restored to its pre-accident condition, giving you solid ground to demand more compensation.

Immediate Diminished Value

The third type is Immediate Diminished Value. This represents the drop in your car’s market value right after the crash but before any repairs have been made. It’s essentially what your car is worth in its damaged, unrepaired state.

While it’s a valid concept, this type of diminished value is rarely used in claims. Once the vehicle is repaired, the focus shifts to inherent and repair-related losses, which are what truly impact your long-term financial position.

Putting It All Together: A Texas Scenario

Imagine your $40,000 Ford F-150 is in an accident. After perfect repairs, its inherent diminished value is $5,000 due to the accident history. But then you notice the new tailgate doesn’t close correctly and the paint is slightly off. That poor workmanship creates another $2,500 in repair-related diminished value. Your total claim would be for $7,500.

Bad repairs can significantly decrease your car’s value. Industry data shows that shoddy work can add an extra 5-15% of value loss on top of the initial drop. You can learn more about how insurance issues are affecting Texans in this detailed report.

By identifying which types of diminished value apply to your situation, you can build a much stronger claim. A professional appraisal from SnapClaim documents both inherent and repair-related losses, giving you the hard evidence needed to negotiate effectively.

Calculating and Proving Your Claim Amount

Knowing you’re owed money is one thing, but proving it is another. When you file for diminished value in Texas, the at-fault driver’s insurance company won’t just write a check for the amount you ask for. Their first move is almost always a lowball offer generated by an internal formula designed to save them money.

Your job is to build a case so solid they can’t ignore it. It’s about dismantling their weak arguments with undeniable proof, and that requires a methodical approach.

Step 1: Gather Your Essential Documents

Before you calculate anything, you need to collect your evidence. Think of this as laying the foundation for your claim—each document helps tell the story and supports your position.

Start by gathering these items:

- The Official Police Report: This is essential. It establishes the facts of the accident, including who was at fault.

- Repair Invoices and Estimates: You need the detailed, itemized records from the body shop. These documents show every part that was replaced and the labor performed, proving the extent of the damage.

- Pre- and Post-Accident Photos: Photos of the damage before repairs and shots of the finished work are powerful visual proof of the collision’s severity.

Step 2: Avoid the Insurer’s Faulty Formulas

Insurance adjusters often use a formula known as “17c” to calculate diminished value. It originated from a Georgia court case and is known for producing extremely low numbers.

Crucial Takeaway: The 17c formula is not recognized or mandated by Texas law. You are not obligated to accept a settlement based on this or any other generic calculation the insurer uses. It’s a negotiating tactic, not a legal requirement.

When an adjuster presents a low offer based on 17c, you can confidently reject it. Your claim should be based on actual market data for your specific vehicle in your local area, not a one-size-fits-all formula.

Step 3: Commission an Independent Appraisal

This is the single most important step in succeeding with your diminished value in Texas claim. While online calculators can provide a rough estimate, they lack the credibility to stand up to an insurance company’s scrutiny. A certified, independent appraisal is your strongest piece of evidence.

Here’s what a professional appraisal report provides:

- Defensible Data: It’s built on real-time market data from your local area, comparing your vehicle to similar ones for sale.

- Expert Analysis: A certified appraiser provides a professional opinion on how the accident history impacts your car’s resale value.

- Credible Evidence: This unbiased, third-party document carries significant weight in negotiations and is admissible in court.

A professional appraisal turns your claim from a simple request into a formal, evidence-backed demand. For more on getting what you’re owed, it’s helpful to see how to extract the full value of your injury claim from established legal experts.

A SnapClaim report provides the clear, data-driven proof you need to show your vehicle’s true loss in value. When you understand https://www.snapclaim.com/calculate-diminished-value with professional tools, you gain the upper hand and can negotiate for the fair compensation you deserve.

Navigating the Insurance Claims Process

Filing the initial claim is just the beginning. The real challenge starts when it’s time to negotiate. Insurance adjusters are trained negotiators whose primary goal is to minimize company payouts.

This section provides a playbook for dealing with them, turning an intimidating conversation into a structured negotiation you can win.

Your first move is to send a formal demand letter to the other driver’s insurance company. This isn’t a quick email—it’s a professional document that outlines the facts, makes your case for diminished value in Texas, and demands fair compensation, all supported by your certified appraisal report.

For a complete walkthrough of the initial claims process, this step-by-step guide to filing an auto insurance claim is a great resource.

Your Diminished Value Demand Letter Template

A strong demand letter is clear, professional, and direct. It presents a logical argument that leaves no room for confusion.

Here’s a simple but effective template:

- Your Information: Start with your full name, address, and the date.

- Claim Details: Include the claim number, the date of the accident, and the name of their insured driver.

- Clear Statement of Purpose: State that you are making a formal demand for the inherent diminished value your vehicle suffered due to the accident.

- Present the Evidence: Briefly describe your vehicle and mention that you have enclosed an independent appraisal report. State the professionally calculated diminished value amount (e.g., “$5,700“).

- Formal Demand: Use clear language: “I hereby demand payment in the amount of [Your Claim Amount].”

- Set a Deadline: Give them a reasonable timeframe to respond, like 15 business days, to show you expect a timely answer.

- Closing: End with a professional closing and your signature. Remember to attach a full copy of your SnapClaim appraisal report.

Countering Common Adjuster Tactics

Insurance adjusters use a standard playbook to deny or lowball claims. Your certified appraisal report is the perfect tool to dismantle their arguments with data, not emotion.

Here’s how to counter their most common objections:

Tactic 1: “Our repairs made your vehicle whole again.”

- The Flaw: This argument ignores reality. Repairs fix physical damage but can’t erase the accident from a vehicle’s history report, which is what causes the value to drop.

- Your Rebuttal: “The repairs addressed the physical damage, but they did not restore my vehicle’s pre-accident market value. As my certified appraisal shows, the permanent accident history has caused a market value loss of [Your Claim Amount]. No informed buyer would pay the same for a wrecked-and-repaired vehicle as they would for one with a clean history.”

Tactic 2: “We don’t pay for diminished value in Texas.”

- The Flaw: This is incorrect. Texas courts have consistently upheld that diminished value is a recoverable part of property damage.

- Your Rebuttal: “Texas law and established case precedents confirm an owner’s right to recover for the loss in their property’s fair market value. My claim is fully supported by both legal standards and the detailed market analysis in my appraisal report.”

Expert Tip: Remain calm and professional. Stick to the facts in your appraisal. A data-driven report speaks for itself and shows the adjuster you are serious, informed, and prepared.

By anticipating these tactics and countering them with evidence-based responses, you shift the power dynamic. The conversation is no longer about their opinion versus yours; it’s about their unsupported claims versus the hard data in your certified report.

Why a Certified Appraisal Is Your Strongest Tool

After an accident, proving your car lost value can feel like an uphill battle. You know it’s worth less, but the insurance adjuster needs proof. A certified appraisal is the single most powerful tool for providing that proof and getting a fair payout for your diminished value in Texas claim.

An independent appraisal transforms your claim from a simple opinion into an evidence-backed demand. It provides a defensible, data-driven calculation of your financial loss that stands up to scrutiny.

How an Appraisal Gives You Leverage

Without solid evidence, you’re negotiating on the insurance company’s terms. They use internal formulas, like the 17c method, designed to produce the lowest possible number. A certified appraisal report flips that dynamic.

Here’s how it gives you leverage:

- It Presents Unbiased Data: A report from an independent appraiser is built on verifiable market analysis, not a self-serving formula.

- It Establishes Credibility: It signals to the adjuster that you are serious and have a professionally backed claim.

- It Speeds Up Negotiations: When adjusters see a credible, court-ready document, they are more likely to offer a fair settlement to avoid a lengthy dispute.

An appraisal isn’t just a piece of paper; it’s your negotiation power. It replaces arguments with facts, forcing the insurance company to address the real financial damage you’ve suffered.

What Makes a SnapClaim Report So Effective

Every SnapClaim appraisal is built on a methodology reviewed by licensed, I-CAR and ASE-certified appraisers. Our reports are designed to be clear and defensible, giving you the exact proof needed for a diminished value in Texas claim. You can learn more about what separates the best diminished value appraisers from the rest in our detailed guide.

Our data-driven approach analyzes your vehicle’s specific details against current, local market conditions to calculate its true loss in value. This makes it difficult for an adjuster to dismiss your claim or justify a lowball offer. With this certified evidence, you can confidently push back and demand the full amount you’re owed.

If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee — guaranteed. This is our commitment to helping you fight for a fair outcome without the risk.

Frequently Asked Questions About Diminished Value in Texas

Can I claim diminished value if the accident wasn’t my fault?

Yes, absolutely. In Texas, you can only file a diminished value claim against the at-fault driver’s insurance company. If you were not responsible for the accident, you have the right to be compensated for your vehicle’s loss in market value.

How long do I have to file a diminished value claim in Texas?

You have exactly two years from the date of the accident. This is known as the statute of limitations for property damage. It’s best to start your claim process as soon as repairs are completed to avoid any last-minute issues with the deadline.

Do I need a lawyer to file a diminished value claim?

For most standard diminished value claims, a lawyer isn’t necessary. The most important tool for a successful negotiation is a certified appraisal report. This data-backed evidence provides the leverage you need to negotiate effectively on your own.

What should I do if the insurance company denies my claim?

Don’t be discouraged. A denial is often the insurance company’s first move. Respond professionally in writing, resubmitting your certified appraisal as evidence. If they still refuse to negotiate fairly, you can file a complaint with the Texas Department of Insurance or pursue the matter in small claims court.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes.

Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step.

Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.

👉 Get your Diminished Value Appraisal Report Today