You’re staring at your car, fresh from the body shop. It looks good as new, but you know it’s not worth the same anymore. You’re right—and a diminished value calculator is often the first step to understanding how much your car’s value has dropped.

This guide explains how these calculators work, what they get right, what they miss, and how to use that initial estimate to build a strong insurance claim backed by real evidence.

What Is a Diminished Value Calculator?

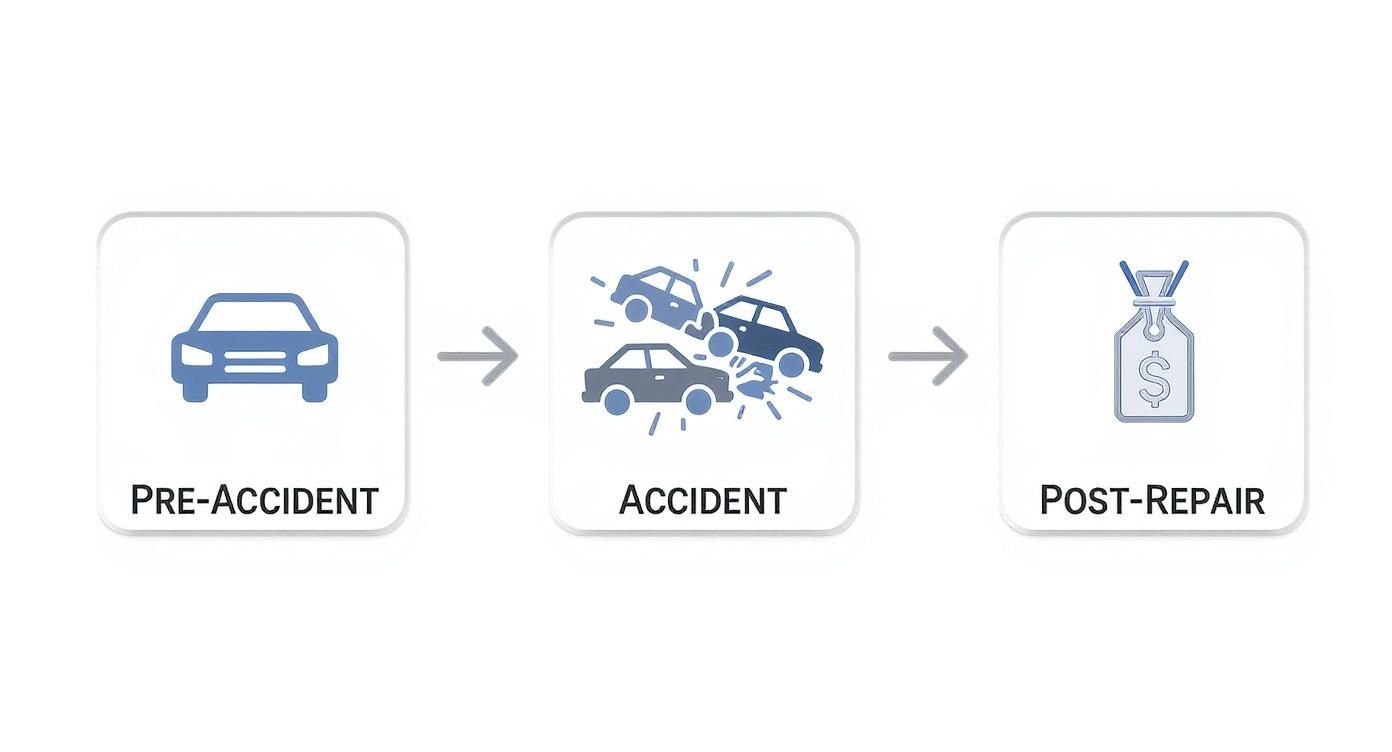

Even with perfect repairs, a vehicle with an accident on its record is worth less than one without. This loss in resale value is called diminished value. A diminished value calculator is an online tool that gives you a quick, ballpark estimate of this financial loss.

It’s like the real estate market. Imagine two identical houses side-by-side. One is perfect, but the other had major foundation damage that was expertly repaired. Which one would you pay full price for? Buyers will always demand a discount for the property with a damage history, and cars are no different.

It’s All About “Inherent” Diminished Value

The most common type of loss is inherent diminished value. This is the automatic drop in value that occurs the moment an accident is reported, even if repairs are flawless. It’s a permanent stigma on your vehicle’s history report (like CARFAX or AutoCheck) that makes future buyers hesitant.

Industry data consistently shows that even perfectly repaired cars take a serious financial hit. For example, a 3-year-old SUV worth $32,000 before a collision might only fetch $28,400 after repairs. That’s a $3,600 loss you’re expected to swallow unless you file a claim.

How These Calculators Estimate Your Loss

A good diminished value calculator isn’t just pulling numbers from thin air. It uses a simplified formula based on key information you provide. While it’s not detailed enough to win an insurance negotiation on its own, it’s the perfect first step to confirm you’ve suffered a loss worth pursuing.

These tools typically ask for:

- Vehicle Details: Make, model, year, and trim level.

- Pre-Accident Condition: Mileage and overall condition before the crash.

- Damage Severity: A simple choice of minor, moderate, or severe.

Plugging in these details gives you a preliminary number. This figure is your starting point—the proof you need to confidently move forward with a formal diminished value claim against the at-fault insurance company.

Calculator Formulas vs. Professional Appraisals

Not all diminished value calculations are created equal. When you file a claim, the insurance company will likely use a self-serving formula to produce a lowball offer. Understanding their method is the key to fighting back with credible, market-based evidence.

The Insurance Company’s Favorite Trick: Rule 17c

Many insurers rely on a formula called Rule 17c. It sounds official, but it’s a shortcut they love because it consistently spits out low figures that minimize their payouts.

The Rule 17c method came from a single Georgia court case and was never intended to be a national standard. However, insurers adopted it widely because it works in their favor. It’s a rigid, three-step process that often ignores what’s actually happening in the used car market.

Here’s a quick breakdown of how they use it to undervalue your claim.

The Rule 17c Formula: How It Works Against You

This formula is designed to shrink your claim at every step. Here’s a look at how the math plays out.

| Step | How It Reduces Your Claim | Example Calculation |

|---|---|---|

| 1. The 10% Cap | The formula starts by capping your maximum possible loss at just 10% of your car’s pre-accident value (using NADA guides, not Kelley Blue Book). | A $30,000 car is immediately capped at a maximum diminished value of $3,000, regardless of the damage. |

| 2. Damage Multiplier | Next, they apply a subjective damage multiplier. “Moderate” damage often gets a 0.50 multiplier, cutting the value in half. | The potential $3,000 claim is instantly reduced to $1,500. |

| 3. Mileage Multiplier | Finally, they slash the number again with a mileage adjustment. A car with 60,000 miles might get hit with a 0.40 multiplier. | The remaining $1,500 is multiplied by 0.40, leaving a final offer of just $600. |

See the problem? A legitimate, multi-thousand-dollar loss is whittled down to a fraction of its true value. For a deeper dive into this flawed formula, you can learn more about the 17c calculation method and why it’s so problematic.

The Professional Standard: Market-Based Analysis

A certified appraisal from SnapClaim throws rigid formulas out the window. Instead, we use a market-based analysis—the method trusted by courts and industry experts because it answers one simple question: What are buyers in the real world willing to pay for a wrecked-then-repaired car like yours?

An expert appraiser doesn’t rely on a generic diminished value calculator. They perform detailed research and dig into real-world data to pinpoint your car’s true post-repair value.

This professional approach involves:

- Analyzing Real Sales Data: We pull sales records for vehicles identical to yours, comparing the selling price of accident-free models to those with a similar damage history.

- Consulting Industry Experts: We contact dealership managers and wholesalers to get boots-on-the-ground insights into how an accident history impacts your specific make and model.

- Reviewing Auction Results: Major auto auctions provide a goldmine of data, showing exactly what cars with repaired damage sell for every day.

This is how you build a real case. Our comprehensive, evidence-based approach replaces the insurer’s lowball formula with verifiable proof, arming you with the documentation you need to demand a fair settlement.

Why a Diminished Value Calculator Isn’t Enough

A basic diminished value calculator is a great starting point, but it can’t grasp the critical nuances that determine your car’s actual loss. Your vehicle type, brand reputation, and current market trends play a huge role in your final claim amount.

Think about it: a buyer looking at a five-year-old family sedan expects some wear and tear. An accident history isn’t ideal, but it may not be a deal-breaker. Now, picture someone shopping for a two-year-old luxury sports car. That buyer is paying a premium for perfection. An accident history on that car is a massive red flag, causing a much steeper drop in its car value after an accident.

Key Factors Calculators Can’t Measure

An online calculator uses a generic algorithm that misses these crucial details:

- Brand Reputation: Luxury and performance brands like BMW, Porsche, and Tesla attract picky buyers. An accident history undermines the prestige these brands are built on, leading to a larger diminished value loss.

- Vehicle Age and Mileage: A newer, low-mileage car will take a bigger financial hit than an older, high-mileage vehicle. Buyers pay a premium for “like-new” condition, and an accident record shatters that appeal.

- Market Trends: Economic factors, inventory shortages, and consumer demand all affect how quickly a vehicle depreciates. This baseline depreciation impacts the starting value used in any calculation. For example, current depreciation trends show that Prestige Luxury Cars are depreciating much faster than Small Pickups, which affects the overall loss.

This is why a professional appraisal is so critical. A certified appraiser from SnapClaim digs into real-time market data for your exact vehicle. This provides the hard evidence needed to build a specific, data-backed case—the kind of proof you need to negotiate fairly.

Online Calculator vs. Certified Appraisal

Think of a diminished value calculator as a symptom checker—it tells you there might be a problem. A certified appraisal is the doctor’s official diagnosis. An insurance adjuster will not take a printout from a free online tool seriously. They require verifiable, expert-backed evidence to approve a diminished value claim.

| Feature | Online Calculator | Certified Appraisal |

|---|---|---|

| Methodology | Generic algorithm (e.g., Rule 17c) | Multi-point market analysis & comparable sales data |

| Accuracy | Low; provides a rough ballpark only | High; reflects specific market conditions and vehicle details |

| Credibility | Very Low; rejected by insurers as proof | High; accepted as verifiable, expert-backed evidence |

| Use Case | Quick check to see if you have a claim | Formal demand for negotiation, arbitration, or court |

While a calculator is a great first step, a certified appraisal from SnapClaim provides the power to secure a fair settlement. Our reports are built using a transparent and industry-accepted process. To learn more, our guide on how to read an appraisal report breaks down what makes a report credible.

How to Strengthen Your Claim with an Appraisal Report

Once you have a certified appraisal in hand, the negotiation dynamic changes. You are no longer just asking for compensation—you are presenting a data-backed demand. Verifiable market evidence replaces the insurer’s lowball formulas, putting you in the driver’s seat.

The first step is to formally submit your diminished value claim by sending a demand letter and a full copy of your SnapClaim appraisal to the at-fault driver’s insurance company.

Tips for Negotiating with the Insurance Adjuster

Your certified report is your most powerful tool. Learning how to negotiate with an insurance adjuster helps you use it effectively.

- Be Professional and Persistent: Keep all communication polite and focused. Follow up regularly and keep detailed records of every conversation.

- Stick to the Evidence: Constantly refer back to your appraisal report. Use phrases like, “As the market analysis in my certified report demonstrates…” to ground the discussion in facts.

- Shift the Burden of Proof: If the adjuster makes a low offer, ask them to provide their own detailed report with verifiable market data to justify it. A generic formula is not credible evidence.

Our Guarantee Ensures a Risk-Free Process

Taking on an insurance company can feel daunting. That’s why SnapClaim offers a simple Money-Back Guarantee: if your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee—guaranteed.

This promise removes the financial risk, allowing you to confidently arm yourself with the powerful evidence needed to fight for the compensation you rightfully deserve.

Understanding State Laws for Diminished Value

Your ability to recover diminished value depends heavily on state laws. The rules can change from one state to the next, so it’s important to understand your rights before negotiating. A key concept is the difference between “first-party” and “third-party” claims.

- First-Party Claim: A claim against your own insurance company.

- Third-Party Claim: A claim against the at-fault driver’s insurance company.

In almost every state, you can only file a third-party claim for diminished value. Your own insurance policy is a contract to repair your vehicle, not to guarantee its resale value. The at-fault party’s insurance, however, is responsible for making you “whole” again, which includes compensating you for the loss in market value.

Your right to recover this loss hinges on the laws in your state. Some states have clear-cut court cases backing it up, while others are less defined. This is why knowing how diminished value claims are handled by state is so important.

A certified appraisal report from SnapClaim provides the legally sound documentation you need. It uses a defensible methodology and verifiable market data to build a case that stands up to scrutiny in any state.

Frequently Asked Questions (FAQ)

Can I claim diminished value if the accident was my fault?

No, in nearly all cases. Diminished value claims can only be filed against the at-fault driver’s insurance policy (a third-party claim). Your own insurance covers repairs but not the subsequent loss in your car’s market value.

How long do I have to file a diminished value claim?

Every state has a time limit, known as the statute of limitations, for filing property damage claims. This deadline typically ranges from two to four years from the date of the accident. It is always best to start the process as soon as repairs are complete.

Will an insurance company accept my online calculator result?

No. While a diminished value calculator is a useful starting point, insurers do not accept its results as proof of loss. They require a detailed appraisal report from a certified expert that uses verifiable market data to justify the claim amount.

Can I make a claim if the at-fault driver was uninsured?

It depends. If you have Uninsured/Underinsured Motorist (UIM) property damage coverage, you may be able to file a diminished value claim with your own insurer. Review your policy or contact your agent to see if this applies in your state.

Take the Next Step with Confidence

An online diminished value calculator is a great way to start, but a certified appraisal is what you need to get paid fairly. A SnapClaim report provides the data-backed proof you need to negotiate effectively and recover the money you are owed.

Get your free estimate today or order a certified appraisal report to strengthen your insurance claim.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes.

Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step.

Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.

👉 Try free diminished value calculator