If another driver caused an accident that damaged your vehicle in California and you want file diminished Value in California, you’re likely facing a hidden financial loss—even after the repairs are done. Fortunately, you can file a diminished value claim in California. The law allows you to pursue compensation for the difference between your car’s pre-accident value and its lower post-repair value, ensuring you’re compensated for the full financial damage caused by the at-fault driver. learn more and find diminished value appraiser in California.

What Is a Diminished Value Claim?

Imagine two identical cars for sale. One has a perfect vehicle history, while the other was in a collision last year. Even with flawless repairs, which one would a buyer pay more for? The one with the clean record, every time.

That difference in price is the diminished value. It’s the permanent drop in your car’s market value caused by its new accident history, regardless of how well it was repaired.

Your Right to Compensation in California

California law recognizes this loss and gives you the right to recover it from the at-fault driver’s insurance company. The process of seeking this compensation is called a diminished value claim. It is designed to make you financially whole after someone else’s mistake damages your property.

However, insurance companies rarely volunteer a fair payout. Their goal is to minimize what they pay on claims. They often use confusing formulas or delay tactics, hoping you’ll get frustrated and accept a low offer or give up entirely.

Proving Your Loss Is Key

The responsibility to prove your car’s loss in value falls on you. A successful claim requires clear, data-driven evidence that justifies the compensation you are demanding.

You have three years from the date of the accident to file your claim, which aligns with California’s statute of limitations for property damage. For more details on the legal side, you can explore California diminished value claims.

Building a strong case involves a few key steps:

- Gather Your Documents: Collect the police report, repair invoices, and photos of the damage.

- Understand the Insurer’s Tactics: Knowing how insurance companies undervalue claims helps you counter their arguments effectively.

- Get a Professional Appraisal: This is essential. A certified report from an expert like SnapClaim provides the independent, market-based proof you need to negotiate fairly.

This guide provides a clear roadmap to help you build a powerful case and recover the money you are rightfully owed.

Breaking Down the Three Types of Diminished Value

To build a solid diminished value in California claim, it’s helpful to understand the different types of loss you can claim. Think of them as different ways to measure the financial impact of an accident on your vehicle.

Each category identifies a specific loss that occurs at a different stage, from the moment of impact to long after the repairs are complete.

Inherent Diminished Value

This is the most common and unavoidable type of loss. Inherent Diminished Value is the automatic drop in your car’s resale value simply because it now has an accident on its permanent vehicle history report.

Even with perfect repairs, a savvy buyer will always pay less for a vehicle with a collision history. The accident creates a stigma that hurts its market appeal, and this is the loss most diminished value claims aim to recover.

Repair-Related Diminished Value

Sometimes, the repairs themselves can cause further loss. Repair-Related Diminished Value occurs when the body shop’s work is subpar, dragging your car’s value down even more.

Signs of poor repairs include:

- Mismatched Paint: The new paint doesn’t blend with the original factory finish.

- Aftermarket Parts: The insurer may have insisted on cheaper, non-original parts that don’t fit or perform correctly.

- Lingering Problems: You may notice new noises, alignment issues, or visible gaps in body panels.

If you can prove the repairs were substandard, you can claim this additional loss on top of the inherent loss.

Immediate Diminished Value

This type is more technical. Immediate Diminished Value is the difference between your car’s value right before the accident and its value immediately after the impact, but before any repairs are made.

Essentially, it’s what your damaged, unrepaired car was worth. This is less common in claims because once the vehicle is fixed, the focus shifts to the loss caused by its accident history (inherent) and the quality of the repairs (repair-related).

Comparing the Three Types of Diminished Value

Here’s how these concepts compare. Each type of diminished value applies at a different point in your vehicle’s post-accident timeline.

| Type of Diminished Value | When It Occurs | What It Covers |

|---|---|---|

| Inherent | After perfect repairs are complete | The loss in value due to the vehicle’s new accident history. |

| Repair-Related | After poor-quality repairs are done | The additional loss caused by substandard work or cheap parts. |

| Immediate | The moment the accident happens | The drop in value before any repairs have even started. |

For most drivers in California, the primary goal is to prove Inherent Diminished Value. This represents the most significant and lasting financial damage to your car. A professional appraisal report from SnapClaim delivers the hard market data needed to show an insurance adjuster exactly what you’ve lost.

How Insurers Calculate (and Undervalue) Your Claim

If you’ve received a settlement offer that feels low, you’re probably wondering how the adjuster arrived at that number. Insurers often rely on an internal formula designed to minimize their payout on your diminished value in California claim.

This method is commonly known as the “17c Formula.” Understanding how it works is the first step toward fighting back with facts.

The Infamous 17c Formula Explained

The 17c Formula is not a law in California. It’s an internal calculation that became popular with insurers after a Georgia court case. Its purpose is to standardize payouts by capping your potential recovery from the start.

Though it has no basis in California’s vehicle market, adjusters use it frequently. The process is simple but deeply flawed.

Here’s a breakdown:

- Step 1: The 10% Cap: The formula starts by taking your car’s pre-accident value (often from a source like Kelley Blue Book) and applying a 10% cap on the maximum possible diminished value. For a $50,000 vehicle, the most you could ever get is $5,000—before deductions.

- Step 2: The Damage Multiplier: Next, they apply a subjective “damage multiplier” based on the severity of the damage. This reduces the capped amount even further.

- Step 3: The Mileage Multiplier: Finally, they apply another penalty based on your car’s mileage. A vehicle with high mileage will see its figure reduced again.

The Problem with 17c: This formula ignores real-world market data. It uses arbitrary caps and penalties that have no connection to what an actual buyer would pay for your car now that it has an accident history.

A Real-World Example of the 17c Flaw

Let’s see how this works. Imagine your car was worth $30,000 before the accident. It has 60,000 miles and suffered moderate damage.

Here’s the insurer’s typical math:

- Initial Cap: 10% of $30,000 = $3,000 (the absolute ceiling).

- Damage Adjustment: The adjuster calls the damage “moderate” and assigns a 0.75 multiplier. The value drops to $3,000 x 0.75 = $2,250.

- Mileage Adjustment: Your car’s mileage earns a 0.6 multiplier. The final offer is now just $2,250 x 0.6 = $1,350.

A true market loss of $4,000 or more is unfairly slashed to a lowball offer of $1,350. The 17c Formula is a tool that protects the insurance company’s bottom line, not your financial well-being.

You can see how this compares to reality with a professional diminished value 17c calculator. The only way to counter this flawed method is with independent evidence. A certified SnapClaim appraisal replaces their formula with hard data, showing the true car value after accident and strengthening your claim.

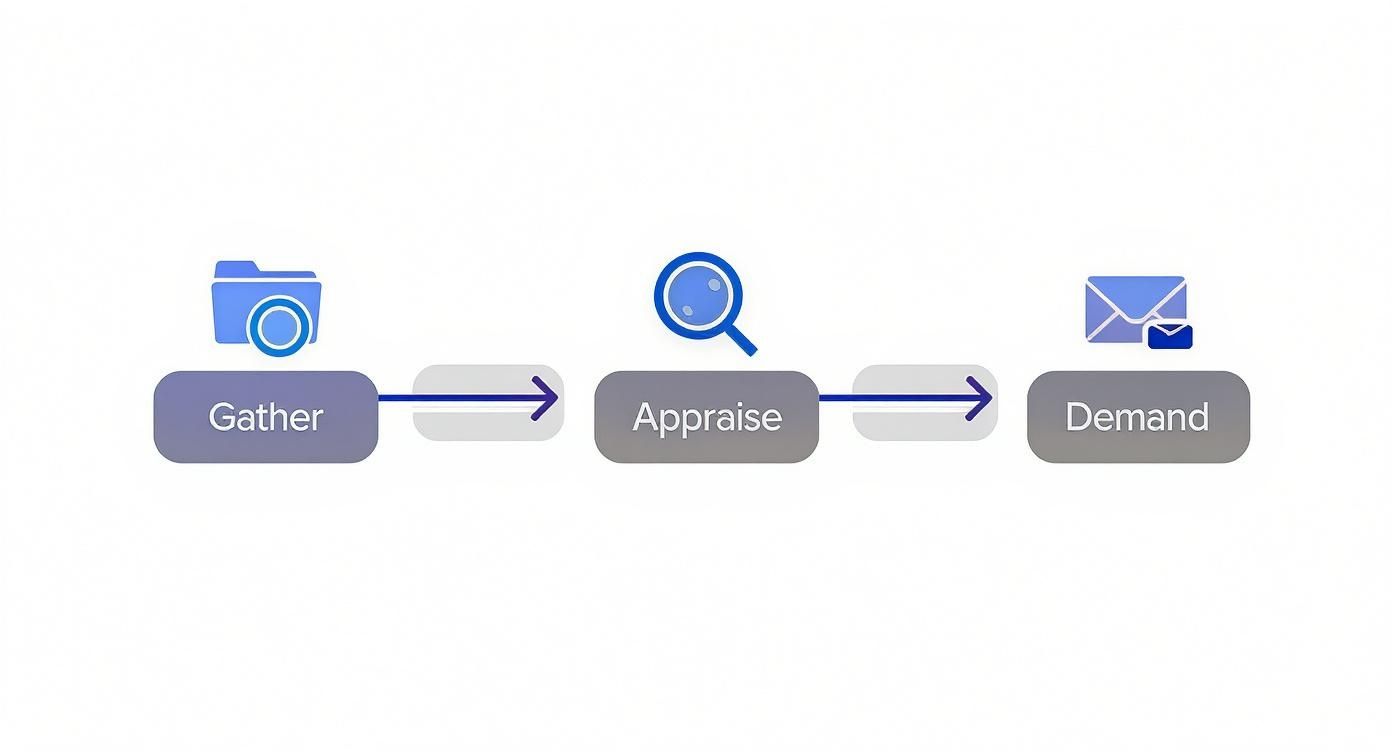

A Step-by-Step Guide to Filing Your Claim

Ready to recover the money you’re owed? Filing a diminished value claim in California can feel intimidating, but breaking it down into a clear plan makes it manageable. Follow these steps to build a solid, evidence-based case that insurance companies have to take seriously.

Step 1: Confirm Your Eligibility

First, make sure you are eligible. In California, you cannot be the at-fault driver. Your claim must be filed against the insurance policy of the person who caused the accident.

Diminished value claims are typically most successful for vehicles that are:

- Newer or have lower mileage.

- In excellent pre-accident condition.

- Free of any prior accident history.

While you can file a claim for an older car, the drop in value is usually more significant for newer models, resulting in a more substantial claim.

Step 2: Gather All Critical Documents

Your claim is only as strong as the evidence supporting it. Start by compiling a complete file that tells the story of your car’s accident and repairs.

Your evidence file should include:

- The Official Police Report: This establishes who was at fault.

- Detailed Repair Invoices: The final, itemized bill from the body shop is crucial.

- Proof of Pre-Accident Value: Use a trusted source like Kelley Blue Book to show what your car was worth before the crash.

- Photos and Videos: Collect pictures of the damage right after the accident and photos of the completed repairs.

Organizing these documents sends a clear message to the adjuster: you are serious and prepared.

Step 3: Obtain a Professional Appraisal

This is the most important step in the process. The insurance company will use its own formulas to minimize your claim. To fight back, you need an independent, certified appraisal report that shows the true car value after accident based on real market data.

A professional appraisal from a trusted source like SnapClaim is not just an opinion—it’s expert evidence. It provides a data-backed, defensible number that proves your financial loss and serves as the foundation for your demand.

An independent report from SnapClaim gives you the unbiased proof you need to negotiate from a position of strength.

Step 4: Submit a Formal Demand Letter

Once you have your appraisal and evidence, it’s time to present your claim. A demand letter is a professional document sent to the at-fault driver’s insurance adjuster that lays out your case.

Your letter should include:

- Your vehicle’s details (make, model, year, VIN).

- The date of the accident and claim number.

- A brief, factual summary of the incident.

- The specific amount of diminished value you are demanding, supported by your appraisal.

- Copies of all supporting documents.

Keep the tone professional and stick to the facts. To learn more, see our guide on how to claim diminished value.

Step 5: Navigate the Negotiation Process

Expect the insurance adjuster to return with a low counteroffer or a denial. This is a standard tactic. Your job is to stand your ground, refer back to the evidence in your certified appraisal, and negotiate confidently.

Equipping yourself with proven strategies for negotiating an insurance settlement successfully can help maximize your recovery. Be persistent, stay professional, and always get settlement offers in writing.

Common Mistakes That Can Sink Your Claim

Navigating a diminished value in California claim means avoiding common traps. Knowing what not to do is as important as knowing what to do. Insurance adjusters are trained to use your mistakes to deny or underpay your claim.

Missing the Filing Deadline

California has a strict statute of limitations for property damage, which includes diminished value. You have three years from the date of the accident to file a claim. If you miss this deadline, you lose your right to pursue compensation forever.

For example, if an accident occurred on March 15, 2024, you have until March 15, 2027, to file. It’s up to you to act promptly.

Immediately Accepting the First Offer

The first settlement offer from an insurance company is almost always a lowball figure. They are testing to see if you will accept a quick, cheap payout. Accepting it is one of the biggest financial mistakes you can make.

Key Insight: The first offer is just an opening move. Politely decline it and counter with your own evidence, starting with a certified appraisal that shows the true loss in market value.

Cashing a Check with Restrictive Language

This is a sneaky tactic that can end your claim. Before cashing any check from the insurer, read the fine print on the check and in any accompanying letters. Insurers often include language stating that cashing it constitutes a “full and final payment” for all claims related to the accident.

If you cash that check, you legally release them from further liability. Always confirm in writing that a payment is only for repairs and does not settle your separate diminished value claim.

Relying on the Insurer’s Appraiser

Never trust the insurance company’s appraiser or their valuation methods. Their job is to protect their employer’s profits, not to ensure you receive a fair settlement. They will use flawed tools like the 17c Formula to justify a low payout.

The only way to level the playing field is with your own independent evidence. A certified, unbiased report from SnapClaim provides the data-backed proof you need to challenge their numbers and fight for the compensation you deserve.

FAQs About Diminished Value in California

Here are answers to some of the most common questions about filing a diminished value in California claim.

Can I claim diminished value if the accident was my fault?

No. In California, you can only file a diminished value claim against the at-fault driver’s insurance company. It is considered a third-party claim, meaning you are seeking compensation for a loss caused by someone else’s negligence. Your own collision coverage is designed to pay for repairs, not the loss of market value.

How long do I have to file a diminished value claim?

You have three years from the date of the accident to file a property damage claim in California. This is known as the statute of limitations. If you miss this deadline, you lose your legal right to pursue compensation for your car’s lost value. It’s best to start the process soon after your vehicle repairs are completed.

Will filing this claim make my own insurance rates go up?

No. Filing a diminished value claim against the at-fault driver’s insurance policy should not affect your own insurance rates. Since you are not at fault and are not filing a claim with your own carrier, your insurance company has no basis to raise your premiums.

Do I need to hire a lawyer for my claim?

Not necessarily. Many people successfully handle their own diminished value in California claims with the right evidence. A certified appraisal report from a company like SnapClaim provides the professional proof needed to justify your claim and negotiate with the insurance adjuster.

However, consider consulting an attorney if your claim is complex, such as if the insurance company is using bad-faith tactics, your vehicle is a high-value exotic or classic car, or you were also injured in the accident.

SnapClaim’s certified appraisal reports provide the data-backed proof you need to negotiate a fair settlement. Plus, our service comes with a risk-free guarantee: if your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee.

Ready to get what you’re rightfully owed?

Get your free estimate today or order a certified appraisal report to strengthen your insurance claim.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes. Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step. Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.