The moment your car is in an accident, it loses value. It doesn’t matter how perfectly it’s repaired—that collision is now a permanent part of its history, and that history costs you money. This drop in your vehicle value after accident is called diminished value, and it’s a real financial loss insurance companies often hope you’ll overlook.

Think about it from a buyer’s perspective. If you were looking at two identical used cars, but one had a clean record and the other had a reported accident, which one would you pay more for? You’d naturally offer less for the one with a collision history. That price difference is the very real, often hidden, financial loss you’ve just suffered.

Understanding the Drop in Your Vehicle Value After an Accident

An accident permanently taints your vehicle’s history report, which directly impacts its fair market value. Even the most skilled body shop can’t erase the stigma that comes with a collision in the eyes of a future buyer. This loss is entirely separate from the physical damage, and it’s a detail insurance companies often conveniently ignore. Their job is to fix the damage, not to compensate you for the resulting loss in resale value.

This isn’t just normal depreciation. Sure, all cars lose value over time, but an accident throws that process into overdrive. A new car might lose 20% of its value in the first year alone, but an accident can pile on an extra loss of 10-30% on top of that. Discover more about how accidents accelerate car depreciation and see how quickly this hidden cost can stack up.

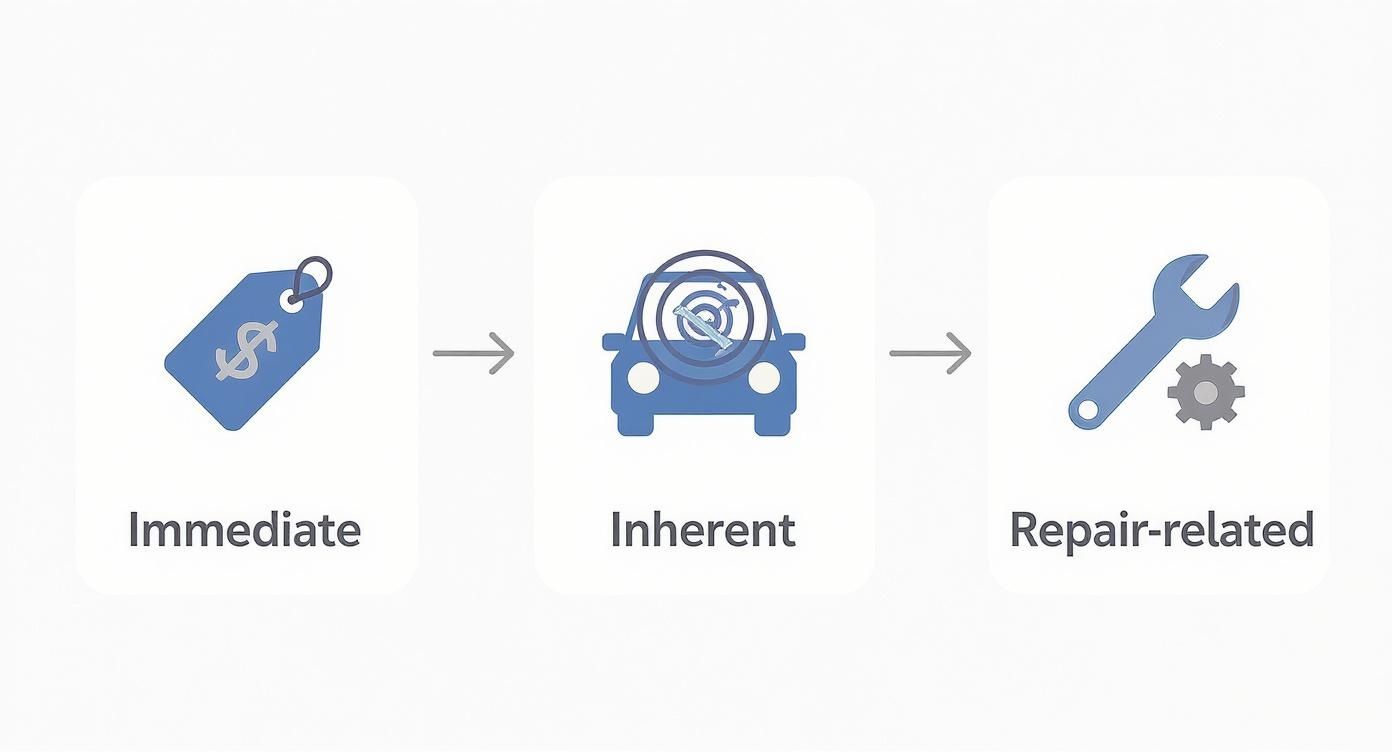

The Three Types of Diminished Value

To get a grip on the change in your vehicle value after an accident, it helps to know that diminished value comes in three forms. Each one represents a different stage of your financial loss.

- Immediate Diminished Value: This is the value your car loses the second the collision happens, before any repairs are made. It’s the difference between what your car was worth moments before the crash and what it’s worth sitting there, damaged.

- Inherent Diminished Value: This is the most common type of claim. It’s the loss in value that sticks around after your car has been perfectly repaired. Why? Because it now has an accident history, making it less appealing to buyers. This is the loss a certified appraisal report from SnapClaim is built to prove.

- Repair-Related Diminished Value: This happens when the repairs are subpar. Maybe the body shop used cheap aftermarket parts, the paint doesn’t match, or the work is just sloppy. These shoddy repairs drag your car’s value down even further.

Knowing which category your loss falls into is the first step in building a solid case. The check your insurance company cuts for repairs only covers the cost of fixing what’s broken—it does nothing to pay you back for the inherent loss in market value.

How Much Value Does a Car Lose After a Crash?

Trying to pin down the exact drop in your vehicle value after an accident is tricky. There’s no single formula, because a handful of key factors always come into play. The single biggest driver is the severity of the damage. A minor fender-bender won’t have the same financial sting as a collision that causes serious frame damage.

Beyond the repairs, your car’s own story matters. Newer cars with low mileage and a pristine pre-accident history tend to lose a bigger chunk of their value. Why? Because buyers in that market expect a clean bill of health, and any accident report is a major red flag. On the other hand, an older commuter car with existing wear and tear won’t see such a dramatic drop.

Key Factors Influencing Value Loss

The final diminished value amount comes down to a few key details that paint the full picture of what your vehicle has been through.

- Severity of Damage: Was it a simple cosmetic scrape or a major wreck that needed structural repairs? The more work it needed, the bigger the hit to its value.

- Vehicle Age and Mileage: A one-year-old luxury SUV with only 10,000 miles will lose a lot more than a ten-year-old sedan with 150,000 miles on the clock.

- Pre-Accident Condition: A car that was meticulously maintained started at a higher value, which means it simply has more value to lose.

- Quality of Repairs: This one is huge. Using certified technicians and Original Equipment Manufacturer (OEM) parts makes a world of difference. Shoddy repairs with cheap, aftermarket parts will only make the value loss worse.

This infographic breaks down exactly how an accident chips away at your vehicle’s worth from different angles.

As you can see, the value loss isn’t just a one-time event. It happens immediately, sticks around because of the accident stigma (inherent diminished value), and can be made even worse by poor-quality repair work.

Putting Numbers to the Damage

So, what kind of numbers are we actually talking about? Generally speaking, a vehicle loses between 10% and 15% of its value for minor damage. For a more significant accident, you can expect that number to jump to around 15% to 30%.

The drop is even steeper for luxury vehicles, which can lose anywhere from 25% to 55% of their value after a serious collision.

How Accident Severity Impacts Diminished Value

This table illustrates the potential percentage of value loss based on the severity of the accident and the type of vehicle, helping you quickly gauge your situation.

| Accident Severity | Economy Vehicle Value Loss | Luxury Vehicle Value Loss |

|---|---|---|

| Minor (Cosmetic) | 10% – 15% | 15% – 25% |

| Moderate | 15% – 25% | 25% – 40% |

| Severe (Structural) | 25% – 35% | 40% – 55% |

These percentages provide a solid starting point for understanding your potential loss. This is exactly why getting a professional, data-backed assessment from SnapClaim is so important. A certified appraisal gives you the hard evidence you need to prove that loss to the insurance company.

For a closer look at different scenarios, you can learn more about how much an accident devalues a car in our complete guide.

Decoding the Insurance Company’s Valuation Methods

When you file an accident claim, the insurance company kicks off its own process to figure out what your car is worth. It’s critical to understand that their goal is the opposite of yours. You want to be made whole for your loss; their primary objective is to minimize how much they have to pay you.

This creates an immediate conflict of interest. The adjuster isn’t a neutral party—they work for the insurance company, and their job is to protect its bottom line. That first offer they give you is almost never their best one. Think of it as a starting point for negotiation, one that’s heavily tilted in their favor.

The Problem with Insurer Valuations

Insurance companies lean on proprietary software and third-party valuation services like CCC ONE or Mitchell to come up with a number for your vehicle’s value. The problem is, these systems are often programmed to produce lowball figures. They do this by cherry-picking the cheapest “comparable” vehicles from their databases—some of which might be in rough shape or located hundreds of miles away.

They might also ask for quotes from a few hand-picked dealerships with whom they have long-standing relationships. This whole process is anything but transparent and is built to justify the lowest possible payout, whether you’re dealing with a diminished value claim or a total loss.

Key Takeaway: An insurance company’s valuation isn’t an unbiased assessment of your car’s worth. It’s a calculated figure designed to serve their financial interests by paying you as little as possible.

Understanding Actual Cash Value (ACV)

You’ll hear the term Actual Cash Value (ACV) a lot. In simple terms, this is what your vehicle was worth the moment before the accident happened. It’s supposed to be the replacement cost minus depreciation.

But the insurer’s calculation of ACV is where things get messy. They control the data and the formula, which gives them a massive upper hand. Their ACV number is often way lower than what an independent appraiser would find using real, current market data for similar cars in your local area.

Statistical analyses show that depreciation is a huge hidden cost after a wreck. You can read new data on vehicle depreciation rates to get the full picture. Their methods often fail to capture your true financial loss. For instance, the infamous “17c” formula, used by some insurers in states like Georgia, is widely criticized for spitting out ridiculously low diminished value figures. You can explore how a 17c diminished value calculator works to see for yourself how these formulas can shortchange your claim.

Challenging their initial number with your own proof isn’t just your right—it’s the only way to make sure you get paid what you’re actually owed.

Building Your Case for a Fair Payout

Knowing the insurer’s playbook is only half the battle. The other half is fighting back with undeniable proof. To successfully challenge a lowball settlement, you need to build a rock-solid case that proves your vehicle’s true financial loss.

It’s time to shift from just understanding the problem to actively gathering the evidence you need to solve it. An organized file of documents is the foundation of any strong diminished value claim. Simply saying your car is worth less isn’t enough—you have to show it.

Your Essential Documentation Checklist

Before you can demand what you’re owed, you need to collect all the relevant paperwork. Think of each document as a chapter in your vehicle’s story, from its pristine pre-accident condition to the final repair invoice.

Start by gathering these key items:

- The Police Report: The official record of the accident, establishing key details and often, who was at fault.

- Pre-Accident Photos: Pictures of your car in excellent condition before the crash are pure gold.

- Maintenance Records: A consistent service history shows you took great care of your vehicle, which supports a higher pre-accident value.

- The Final Repair Invoice: This critical document details every part that was replaced and all labor performed, painting a clear picture of the damage’s severity.

To build the strongest possible case, it’s also smart to understand all the different types of damages you can claim.

The Power of an Independent Appraisal

While the documents above are crucial, the single most powerful tool in your arsenal is a certified, independent appraisal report. The insurance company has its own valuation methods designed to save them money. Your appraisal is the unbiased, data-backed counter-argument that proves the real-world drop in your vehicle value after accident.

A professional appraisal from a trusted source like SnapClaim isn’t just an opinion—it’s market-driven proof. It uses real-time sales data for comparable vehicles in your area to calculate a fair and defensible diminished value figure.

This report transforms your claim from a simple request into a formal, evidence-backed demand. It gives you the independent verification you need to level the playing field and supports your case with certified data.

Negotiating with a Certified Appraisal Report

Once you have the evidence, you’re ready to turn that paperwork into payment. An independent appraisal report is the single most powerful tool you have. Why? Because it replaces the insurance company’s opinion with objective, verifiable market data. This is how you level the playing field.

Unlike the adjuster’s internal calculations, a certified report from SnapClaim is transparent and grounded in real-world data. Our experts analyze recent sales of cars just like yours in your area and use court-accepted methodologies to pinpoint the exact drop in your vehicle value after accident. This professional analysis provides the proof you need to negotiate fairly.

Submitting Your Claim with Confidence

With your certified appraisal in hand, the next move is to officially submit it to the insurance adjuster. The best way to do this is with a formal demand letter—a clear, professional document that lays out your case and what you’re owed.

Your demand letter doesn’t need to be complicated. Just keep it straightforward and include:

- A direct statement that you’re filing a diminished value claim.

- The final repair invoice showing the full extent of the damages.

- Your certified appraisal report as proof of your financial loss.

This simple step completely changes the conversation. You’re no longer just asking for more money; you’re presenting a data-backed case that the insurer is legally obligated to address.

A professional appraisal report flips the script. It forces the insurance company to either pay your documented loss or come up with concrete evidence to dispute it—something they rarely can.

Sample Language for Your Demand Letter

When writing to the adjuster, skip the complicated legal jargon. Be simple and direct. For instance, you could say something like this:

“Enclosed you will find a certified appraisal report from SnapClaim detailing the inherent diminished value to my vehicle following the accident. The report calculates a loss of value totaling [$ Amount]. Please process this first-party diminished value claim and issue payment for this amount.”

That clear, confident language, backed by a professional car appraisal after an accident, makes your position solid and very hard to ignore.

A Risk-Free Path to Fair Compensation

We understand that taking on a massive insurance company can feel intimidating. That’s why we stand behind our work with SnapClaim’s Money-Back Guarantee: If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee — guaranteed.

This makes ordering a report a completely risk-free step toward getting the money you rightfully deserve. It gives you the proof you need to negotiate fairly, ensuring you have the strongest case possible to recover every dollar of your vehicle’s lost value.

Navigating a Total Loss Insurance Claim

Sometimes, the damage to a car is just too severe. When the cost to fix it outweighs its value, the insurance company will declare it a total loss. This isn’t an emotional decision; it’s pure math. An insurer “totals” a car when repair costs hit a certain percentage of its pre-accident value, or its Actual Cash Value (ACV). That threshold usually sits between 70% and 80%, though it varies by state.

The Problem with Total Loss Payouts

Once your vehicle is declared a total loss, the insurance company is supposed to cut you a check for its ACV. The problem is that their valuation methods are built to protect their profits, not to make you whole.

Adjusters often rely on biased software or cherry-pick low-priced “comparable” vehicles to justify the lowest possible insurance total loss payout. This leaves you with a settlement that’s nowhere near enough to buy a truly similar replacement.

Why an Independent Appraisal Is Crucial

This is where you push back. Just like with diminished value claims, an independent appraisal is your most effective tool for fighting a lowball total loss offer. A certified total loss appraisal from SnapClaim gives you an unbiased, data-backed assessment of what your vehicle was really worth right before the crash.

A professional total loss report replaces the insurer’s lowball estimate with real-world market evidence. It provides the proof you need to negotiate for a higher, fairer settlement that accurately reflects what your vehicle was worth.

Armed with an evidence-based report, you can confidently challenge the insurer’s number and demand the compensation you need to buy a genuinely comparable replacement. Don’t just take their first offer. Fight for a payout that actually makes you financially whole again.

FAQs: Vehicle Value After an Accident

Here are straightforward answers to the most common concerns we hear from vehicle owners about diminished value and total loss claims.

Can I claim diminished value if the accident wasn’t my fault?

Yes, absolutely. A diminished value claim is filed against the at-fault driver’s insurance policy. Because their client’s negligence caused your vehicle to lose value, their insurance is responsible for making you financially whole again. This includes compensating you for the loss in resale value, which is proven with a certified diminished value appraisal.

How long do I have to file a diminished value claim?

Every state has a time limit, known as the statute of limitations, for filing property damage claims. These deadlines typically range from two to six years from the date of the accident. However, it’s best not to wait. The ideal time to start your claim is right after repairs are completed, while the primary accident claim is still open. Waiting too long could risk losing your right to compensation.

Is a diminished value claim worth it for an older car?

It depends on the car’s market value right before the crash. While newer, low-mileage vehicles typically see the largest diminished value amounts (since they have more value to lose), older cars aren’t automatically out of the running. A well-maintained classic, a rare model, or any older car with high market value can still suffer a significant financial hit from an accident. The key is the dollar difference between its pre-accident value and post-repair value, which a professional appraisal can determine.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes. Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step. Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.