Has your car been in an accident? If so, you’re probably wondering how much value it has lost, even after perfect repairs. A vehicle diminished value calculator is an online tool that gives you a quick estimate of that loss, helping you decide if you should pursue a formal claim.

What Exactly Is Diminished Value?

Imagine your recently repaired car looks brand new, but when you try to sell it, the dealer’s offer is thousands less than you expected. Why? Because the vehicle history report shows it’s been in an accident. That gap between its pre-accident worth and its new, lower market value is called diminished value.

Even with flawless repairs, a vehicle with an accident on its record carries a “stigma” that permanently lowers its resale value. A diminished value claim is your right to recover that lost money from the at-fault party’s insurance company.

What Does a Calculator Actually Tell You?

A vehicle diminished value calculator provides an instant snapshot of this loss. While it isn’t a formal appraisal, it helps answer the most important question: “Am I leaving money on the table?”

These free tools typically ask for basic information:

- Vehicle Info: The year, make, model, and its pre-accident value (often based on sources like Kelley Blue Book).

- Mileage: Higher mileage usually means a lower diminished value loss, as the car has already depreciated more.

- Damage Severity: The extent of the damage—from cosmetic scrapes to major structural repairs—is a key factor in the calculation.

The number it provides is your starting point. For instance, if a calculator estimates a $4,000 loss, it’s a strong signal that investing in a certified appraisal to support your diminished value claim is a wise move.

The real power of a calculator is that it makes an abstract concept like “lost value” tangible, turning it into a dollar amount you can fight for.

However, it’s crucial to understand their limitations. These tools use simplified formulas and can’t account for unique factors like local market demand or your vehicle’s specific options. A calculator is a great first step, but a data-backed, certified appraisal provides the proof needed to negotiate effectively and recover the full compensation you deserve.

Decoding The Formulas Behind Online Calculators

Ever wondered what powers a free online vehicle diminished value calculator? Most run on a simplified model that insurance companies favor called the “17c formula.” Understanding how it works reveals both its purpose and its major flaws.

The formula gives insurers a standardized way to produce a number, but it’s a blunt instrument. It ignores your car’s unique details and, more importantly, the real conditions of your local used car market—two factors essential for an accurate valuation.

Breaking Down The 17c Formula

The 17c formula is a multi-step process designed to systematically reduce a potential payout using a series of caps and multipliers. It’s less complicated than it sounds.

Here’s a quick overview of the steps:

- Start with Market Value: The calculation begins with your vehicle’s pre-accident value, typically from a guide like NADA or Kelley Blue Book.

- Apply a 10% Cap: The formula immediately caps the maximum possible diminished value at 10% of the market value. This arbitrary ceiling has little connection to real-world loss.

- Apply a Damage Multiplier: The capped amount is then reduced by a damage modifier (a number between 0.00 and 1.00) meant to reflect the severity of the damage.

- Apply a Mileage Multiplier: Finally, the result is reduced again with a mileage multiplier. The more miles on your car, the lower the final estimate.

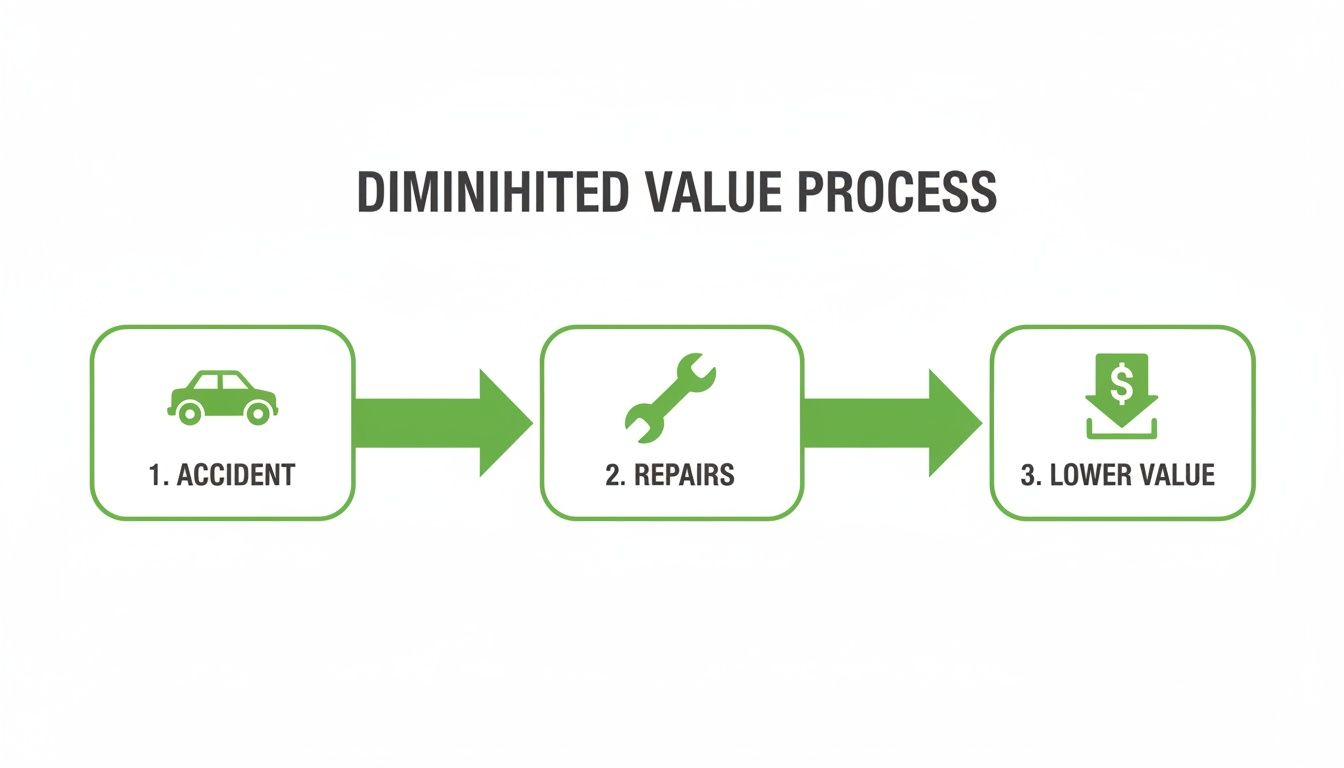

This flowchart shows how a vehicle’s value is permanently damaged after a collision, even after excellent repairs.

As you can see, the accident history remains with your vehicle, creating a permanent drop in market value that a simplistic formula cannot accurately measure.

A Real-World Example Calculation

Let’s see how this plays out. Imagine your 2021 sedan was worth $25,000 before an accident caused moderate structural damage. It has 45,000 miles.

An insurer using the 17c formula would likely calculate your diminished value claim like this:

- Step 1: Start with the $25,000 market value.

- Step 2: Apply the 10% cap to find the base loss: $25,000 x 0.10 = $2,500. This is the maximum possible payout under this formula.

- Step 3: Apply a “moderate damage” multiplier of 0.50: $2,500 x 0.50 = $1,250.

- Step 4: Reduce it with a mileage multiplier for 45,000 miles (typically around 0.60): $1,250 x 0.60 = $750.

The formula produces a diminished value of just $750—a figure that is almost certainly far below the actual financial loss you’d face when selling or trading in the car.

A Look at Standard 17c Formula Multipliers

To see how these numbers work against you, here’s a breakdown of the standard multipliers insurers often use. They are designed to systematically reduce your payout.

| Factor | Multiplier Value | How It Impacts Your Estimate |

|---|---|---|

| Damage Severity | 0.00 – 1.00 | 1.00 for severe structural damage, 0.25 for minor cosmetic issues. |

| Mileage | 0.00 – 1.00 | 1.00 for new cars, dropping to 0.00 for vehicles over 100,000 miles. |

These multipliers are the engine of the 17c formula, ensuring the final number is almost always lower than the true market loss.

The 17c formula is built for insurer convenience, not for fairness to car owners. Its arbitrary caps and generic multipliers almost always lead to lowball offers that don’t reflect actual market conditions.

The Critical Flaws Of A Simplified Approach

While the 17c formula is quick, it’s fundamentally flawed because it ignores the very factors that determine a car’s worth. Insurance adjusters rely on it for one reason: it produces consistently low, predictable payouts that save them money.

The biggest problems with this approach include:

- It Ignores Local Market Conditions: The formula doesn’t account for regional demand, the number of similar cars for sale near you, or what local buyers prefer.

- It Overlooks Vehicle Specifics: Desirable features like special trim packages, a popular color, or optional equipment that add real value are invisible to the formula.

- It Has No Basis in Real-World Data: The multipliers are arbitrary and not tied to actual sales data comparing wrecked-and-repaired cars to those with clean histories.

Because of these issues, an estimate from a basic vehicle diminished value calculator using 17c logic is easy for an insurance company to dismiss. To get a number that can stand up to scrutiny, you need to understand how to calculate diminished value using real, market-driven data—not a formula designed to shortchange you.

Why Free Calculators Often Miss the Mark

While a free online vehicle diminished value calculator provides a useful starting point, relying on its estimate alone for an insurance claim is like using a symptom checker instead of visiting a doctor. It offers a general idea but lacks the specific, verifiable evidence needed for a successful negotiation.

Insurance adjusters are trained to identify the weaknesses in these simple tools. They know that free calculators use generic formulas like the 17c method, which are designed to produce low, standardized numbers. An estimate from one of these sites is easily dismissed because it isn’t backed by real-world, market-specific data.

The Devil Is in the Details They Ignore

A basic online calculator cannot grasp the unique factors that determine your car’s actual market value. It operates in a vacuum, disconnected from the complex, ever-shifting used car market. This is where you can lose thousands without even realizing it.

Here are a few critical details most free calculators overlook:

- Local Market Dynamics: The demand for a specific truck in Texas is completely different from the demand in California. A generic formula ignores local supply, buyer preferences, and regional economic conditions that heavily impact resale value.

- Specific Vehicle Options: Did your car have a premium sound system, panoramic sunroof, or advanced safety package? These options added thousands to its value, but a free calculator has no idea they exist.

- Damage Stigma: There’s a huge difference in how buyers perceive a minor fender-bender versus an accident that caused structural damage. Most calculators use a simple “damage severity” slider that fails to capture the serious stigma attached to frame or unibody repairs.

This is precisely why an expert valuation is so critical. A professional appraiser investigates these nuances to build a credible, defensible report. While a free calculator can point you in the right direction, our detailed 17c formula analysis reveals just how skewed these formulas are in the insurer’s favor.

An online calculator gives you a number. A professional appraisal gives you proof. Insurance companies respond to proof, not to numbers from a generic online form.

Why Verifiable Data Is Non-Negotiable

Insurance negotiations are all about evidence. Without solid proof, the adjuster holds all the power. They can point to their own internal valuation—often based on a formula like 17c—and challenge you to prove it wrong. A printout from a free website won’t win that argument.

The need for precise, data-backed valuations has only grown as cars become more complex. Today’s vehicles are packed with expensive technology and advanced safety systems, making post-accident value loss a bigger financial issue than ever before.

A certified appraisal from SnapClaim provides the evidence you need. It includes a detailed market analysis comparing your repaired vehicle to actual sales data for similar cars in your area. This report transforms a generic guess into a powerful, data-driven valuation that strengthens your claim and forces the insurer to negotiate fairly.

Comparing Online Tools to Certified Appraisals

A free online vehicle diminished value calculator is an excellent starting point, giving you a quick idea of your potential loss. But to successfully file a diminished value claim, you need more than a rough estimate—you need a credible, evidence-based valuation that an insurance adjuster will take seriously.

This is where the difference between a simple calculator and a certified professional appraisal becomes clear. A calculator offers an educated guess based on a generic formula. A certified appraisal, however, is a formal valuation backed by expert analysis and verifiable market data, designed to stand up to scrutiny.

Think of it this way: a calculator is like Googling your symptoms, while a certified appraisal is like getting a diagnosis from a specialist.

Estimate Versus Evidence

The key distinction comes down to one word: evidence.

An online calculator generates a number using a preset formula like the notorious 17c method. This approach relies on arbitrary multipliers that fail to account for your specific vehicle or local market. An insurance adjuster knows this and can easily dismiss the number as unsubstantiated.

In contrast, a certified appraisal is built on a foundation of proof. A professional appraiser analyzes real-world sales data for vehicles just like yours, comparing examples with and without accident histories. This market-driven approach provides the concrete evidence needed to justify your claim for your car’s value after an accident.

A Head-to-Head Comparison

Let’s put these two tools side-by-side. When you’re trying to recover the money you’re owed, the gap in credibility and effectiveness is massive.

Online Calculator vs. Certified Appraisal

Here’s a direct comparison of what a free tool provides versus what a professional report delivers.

| Feature | Free Online Calculator | Certified Professional Appraisal |

|---|---|---|

| Methodology | Based on generic formulas like 17c, with arbitrary caps and multipliers. | Uses market-based analysis of comparable vehicle sales in your specific area. |

| Data Sources | Relies on book values (e.g., KBB) and preset, non-verifiable adjustment factors. | Pulls from real-time sales listings, auction results, and dealership data. |

| Customization | Offers limited input for make, model, and mileage; rarely accounts for options. | Analyzes your vehicle’s specific trim, options, condition, and local demand. |

| Legal Defensibility | Easily dismissed by insurers as speculative and lacking credible evidence. | Provides a court-ready, defensible document signed by a valuation expert. |

| Insurer’s View | Seen as a consumer tool with little to no weight in claim negotiations. | Acknowledged as a professional valuation requiring a serious, evidence-based response. |

As you can see, a certified report transforms your claim from a simple request into a well-supported, evidence-backed demand.

A calculator gives you a number to start the conversation. A certified appraisal gives you the evidence to finish it successfully.

Why a Professional Report Changes the Game

When you submit a certified appraisal from a trusted source like SnapClaim, the negotiation dynamic shifts. The burden of proof is no longer on you to justify a number from an online tool. Instead, the insurance company must provide equally strong evidence to dispute your professionally prepared valuation.

This expert-backed methodology gives your claim real teeth and shows you are prepared to defend your claim with facts. To learn more about this process, see how a professional car appraisal after an accident is created. This level of preparation sends a clear signal to the insurer: a lowball offer based on a flawed formula will not be accepted.

How Much Money Are You Really Leaving on the Table?

It’s one thing to hear the term “diminished value,” but another to see what it means for your wallet. The financial loss your vehicle sustains after an accident is often thousands of dollars in lost equity that you are entitled to recover. While a vehicle diminished value calculator offers a quick estimate, understanding the real-world financial stakes is what truly matters.

Even with perfect repairs, the accident is now a permanent part of your car’s history report. That history acts as a red flag for any savvy buyer, instantly reducing its market value. This isn’t just a small dip; it’s a significant financial loss.

Real-World Scenarios

Consider a popular pickup truck valued at $50,000 before a moderate rear-end collision. After repairs, it looks good as new. But its accident history means it will sell for less than an identical truck with a clean record. The same applies to a family SUV worth $30,000 that sustains damage to its side panels.

This isn’t just speculation. Across the country, vehicle owners lose thousands after a crash. Research shows that diminished value losses typically range from 10% to 20% of the vehicle’s pre-accident market value. For that $30,000 SUV, you’re looking at a loss of $3,000 to $6,000, even with flawless repairs.

Here’s how that can break down:

- A $30,000 Sedan: A 15% loss means you could be leaving $4,500 on the table.

- A $50,000 Pickup Truck: A 12% loss translates to $6,000 in unrecovered equity.

- A $70,000 Luxury SUV: A 20% loss from structural damage could mean a $14,000 hit.

This isn’t just a list of numbers—it’s your money. If you don’t file a formal claim backed by solid evidence, the at-fault party’s insurer gets to keep it.

An Investment, Not an Expense

These figures make it clear why pursuing a diminished value claim is so critical. A professional appraisal is not just another cost; it’s a small investment to recover a much larger sum. To get a better sense of your vehicle’s true worth, you can find a comprehensive guide on fair market value from a reputable source like the NHTSA, which highlights factors influencing vehicle safety and value.

A certified appraisal report from SnapClaim gives you the data-backed proof you need to negotiate from a position of strength. It turns your claim from a simple request into a well-supported demand for what you’re rightfully owed.

By using real market data and expert analysis, a certified report gives your claim the credibility to stand up to an insurer’s attempts to downplay your loss. It’s the most powerful tool you have to ensure you don’t walk away from thousands of dollars that belong to you.

Using a Certified Report to Strengthen Your Claim

Armed with a certified appraisal report, you are no longer just asking for compensation—you are presenting a formal, evidence-backed demand. While a vehicle diminished value calculator is a good starting point, a professional report is the tool you need to navigate negotiations and secure a fair settlement.

The process is straightforward and, most importantly, puts you in control.

Your first step is to send the certified report to the at-fault driver’s insurance adjuster, along with a formal demand letter. This letter should clearly state the diminished value you’re claiming and reference the appraisal as your primary evidence. This action immediately changes the dynamic of the conversation.

Shifting the Burden of Proof

Once you submit a data-driven report, the burden of proof flips. It’s no longer your responsibility to prove your loss. Instead, the insurance company must now justify its offer with equally compelling evidence.

They can’t simply dismiss your claim or hide behind a flawed formula like 17c. To counter your claim, they must produce their own appraisal that can challenge your report’s market analysis and data. This professional approach elevates your claim from a simple request to a well-supported case, signaling that you know your rights and are prepared to fight for your vehicle’s true loss in value.

The financial stakes are significant, especially with recent fluctuations in vehicle prices. Understanding the market is key to a fair insurance total loss payout or diminished value settlement.

Navigating the Negotiation with Confidence

When speaking with the adjuster, remain professional and stick to the facts presented in your report. Here’s how to handle the conversation:

- Present Your Demand: State the exact diminished value amount from your certified appraisal.

- Reference the Evidence: Point to the specific comparable vehicles and market data in the report that support your figure.

- Request Their Counter-Evidence: If they make a lower offer, ask for their detailed valuation report in writing.

SnapClaim makes this entire process risk-free with our Money-Back Guarantee. If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee. We want you to feel confident that your investment in a certified report will help you pursue the compensation you rightfully deserve.

Frequently Asked Questions (FAQ)

Here are straightforward answers to common questions from vehicle owners filing a diminished value claim for the first time.

Can I claim diminished value if the accident wasn’t my fault?

Yes, absolutely. A diminished value claim is filed against the at-fault driver’s insurance policy. Since their client’s negligence caused your property (your vehicle) to lose value, their insurance is responsible for making you whole. You generally cannot claim diminished value from your own insurance company, as standard policies cover repairs, not loss of market value.

Can I claim diminished value if the at-fault driver is uninsured?

This depends on your insurance policy and your state’s laws. In some states, like Georgia, you may be able to file a diminished value claim under your own Uninsured/Underinsured Motorist (UM/UIM) property damage coverage. It is essential to review your policy documents or consult with an expert to understand your options.

What should I do if the insurance company ignores my claim?

Don’t let them off the hook. If an adjuster is unresponsive, send a follow-up email or certified letter to create a paper trail. If they continue to ignore you or reject your certified report without providing their own evidence, you can file a formal complaint with your state’s Department of Insurance. This often prompts a response and shows the insurer you are serious about your claim.

Is there a deadline for filing a diminished value claim?

Yes. Each state has a statute of limitations for property damage claims, which sets a legal deadline for filing. This period can range from one to several years from the date of the accident. It is best to initiate your claim as soon as your vehicle repairs are complete to avoid missing this critical window and losing your right to compensation.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes.

Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step.

Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.

👉 Get your Diminished Value Appraisal Report Today