Total Loss Appraisal in South Carolina

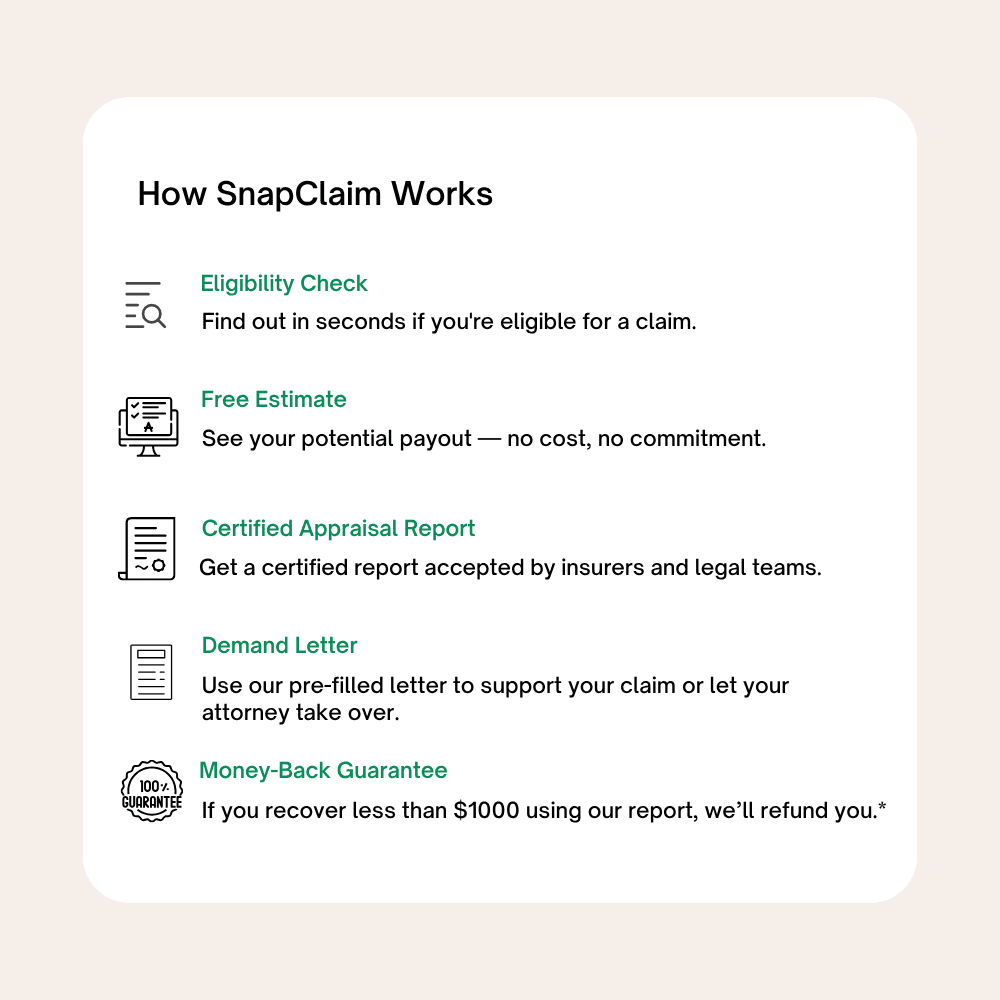

Get Your Free Estimate in minutes.

If your car was declared a total loss and you’re not happy with the insurance payout, you have the right to request a South Carolina total loss appraisal. SnapClaim helps you dispute unfair insurance valuations with certified, data-backed reports that show your vehicle’s true fair market value.

No credit card required [Takes less than 30 second]

Total Loss Appraisal in South Carolina: What You Need to Know

South Carolina Total Loss Appraisal — Get a Fair Settlement for Your Totaled Vehicle

If your vehicle was declared a total loss in South Carolina and the insurance offer feels too low, you have the right to request an independent South Carolina total loss appraisal to verify your car’s true pre-accident value. From Charleston, Columbia, North Charleston to Mount Pleasant, Rock Hill, Greenville and communities across the state, SnapClaim helps South Carolina drivers recover the fair market value (ACV) of their vehicles and challenge low or inaccurate insurance valuations. Our certified total loss appraisal reports are data-driven, USPAP-aware, and insurer-ready — frequently used by adjusters, attorneys, and small-claims courts throughout South Carolina.Why Get a Total Loss Appraisal in South Carolina?

South Carolina’s used-vehicle market varies significantly between coastal cities, fast-growing suburbs, and inland manufacturing hubs. Insurance valuation tools often fail to capture price differences tied to:- Urban vs. suburban demand

- Market premiums in coastal and high-growth regions

- Regional variations in listing supply and pricing

- High demand for trucks, SUVs, and commuter vehicles

Common Reasons to Question a South Carolina Total Loss Offer

- Incorrect trim, package, or drivetrain listed in the insurer’s report

- Comparables pulled from lower-priced regions outside South Carolina

- Improper deductions for condition or aftermarket equipment

- Trucks, SUVs, hybrids, or specialty trims undervalued

- Metro-area pricing (Charleston, Columbia, Greenville, Rock Hill) not properly reflected

What’s Included in Your South Carolina Total Loss Appraisal Report

- Full VIN-decoded breakdown confirming trim, drivetrain, and installed features

- Local comparable listings from Charleston, Columbia, Greenville, Rock Hill, and nearby regions

- Accurate pre-loss fair market value based on South Carolina market conditions

- Adjustments for mileage, features, upgrades, and vehicle condition

- Documentation to invoke the appraisal clause under your South Carolina auto policy

- Optional expert support if negotiations escalate or if an attorney becomes involved

South Carolina Total Loss Rules & Appraisal Rights

South Carolina policyholders may dispute a total loss valuation and request an independent appraisal through the appraisal clause in their policy. If the two appraisers cannot agree, a neutral umpire will decide the final value.- South Carolina Department of Insurance

- South Carolina DMV — Vehicle & Title Services

- South Carolina Courts — Small Claims Information

How to Dispute a Total Loss Offer in South Carolina

- Request the insurer’s valuation report (CCC, Mitchell, Audatex) and review for inaccuracies.

- Order a SnapClaim total loss appraisal to determine the correct ACV.

- Invoke the appraisal clause if your valuation differs significantly from theirs.

- Send the independent appraisal to your adjuster or attorney.

- Use documented market evidence — many South Carolina drivers secure thousands more than the initial offer.

South Carolina Market Insights

- Pickup trucks and SUVs retain strong value across both coastal and inland regions.

- Used-car prices in Charleston, Mount Pleasant, Greenville, and Rock Hill often exceed statewide averages.

- Tourism and port activity drive strong demand for commuter and fleet vehicles.

- Automated valuation tools may undervalue higher trims and professionally maintained vehicles.

Example South Carolina Case Study

Vehicle: 2019 Toyota Tacoma TRD SportInsurance Offer (CCC): $28,400

SnapClaim Appraisal: $33,100

Final Settlement: $32,500 after submitting our independent report under the appraisal clause

Helpful South Carolina Resources

- South Carolina Insurance Consumer Help

- Small Claims & Magistrate Court Info

- South Carolina DMV — Titles & Vehicle Info

- NHTSA — Vehicle History Search

Ready to Get Your South Carolina Total Loss Appraisal?

- No upfront payment required

- Most reports completed in about 1 hour

- Includes a fair-market-value conclusion with insurer-ready documentation

Related South Carolina Locations

Click a pin to open the city’s total loss page.

Find your South Carolina city below to order your Total Loss Appraisal.

Order Your Total Loss Appraisal

Get Your Appraisal Report and Demand Letter Now!

Free Estimate, no credit card required.

Dispute an Unfair Total Loss Offer in South Carolina

If your car was declared a total loss in South Carolina but the insurance payout seems too low, you don’t have to accept it. Under your policy’s appraisal clause, you can request an independent South Carolina total loss appraisal to verify your vehicle’s true fair market value. SnapClaim makes it simple — get a certified total loss report, invoke your appraisal rights, and negotiate a higher settlement — all within minutes.

“After my sedan was declared a total loss following a side-impact accident in Mount Pleasant, the insurance company’s offer was far below what similar cars were selling for in coastal South Carolina. I ordered a SnapClaim appraisal, and their report clearly documented the real market value using local comps. After submitting it, the insurer increased my settlement by more than $3,000.”

Natalie W.,

Mount Pleasant, SC

South Carolina Total Loss – Frequently Asked Questions

When is a vehicle considered a total loss in South Carolina?

South Carolina generally follows a Total Loss Formula (TLF) approach. A vehicle is treated as a total loss when the insurer decides it is not economical to repair because the cost of repairs plus the salvage value approaches or exceeds the vehicle’s Actual Cash Value (ACV) before the crash. You can compare South Carolina with other states here: total loss laws by state.

What does Actual Cash Value (ACV) mean on a South Carolina total loss claim?

ACV is your vehicle’s fair market value immediately before the loss. It should be based on comparable vehicles selling in South Carolina markets (for example, Columbia, Charleston, North Charleston, Mount Pleasant, Rock Hill, Greenville, and surrounding areas), adjusted for year, trim, mileage, options, and condition. For a deeper breakdown of ACV and how it should be calculated, see: Fair Market Value & ACV.

The South Carolina total loss offer seems low — what can I do?

Start by asking for the insurer’s full valuation report (CCC, Mitchell, Audatex, or similar). Review each comparable for: incorrect trim, missing options, wrong mileage, questionable condition ratings, or out-of-area vehicles that don’t reflect South Carolina prices. Many drivers and law firms rely on an independent SnapClaim South Carolina total loss appraisal to support a higher, data-backed value: order a South Carolina total loss appraisal.

Does South Carolina use a fixed percentage threshold to total a car?

South Carolina is effectively a Total Loss Formula state. Instead of a single published percentage (like 70% or 75%), insurers look at whether the repair cost plus salvage value is close to or greater than ACV. When repairs are no longer economical under that formula, the vehicle is treated as a total loss and handled under South Carolina’s salvage title rules.

What happens to my title if my car is totaled in South Carolina?

When an insurer declares a vehicle a total loss in South Carolina, the vehicle is generally treated as salvage. The original title is surrendered and a salvage or similarly branded title is issued. If the vehicle is later repaired and passes required inspections, it may qualify for a rebuilt or branded title before it can be registered and driven again. That brand remains on the title and can affect resale value.

Can I keep my totaled vehicle in South Carolina and fix it myself?

Often, yes. If you choose to retain the salvage, the insurer typically reduces your cash settlement by the vehicle’s estimated salvage value. You keep the damaged vehicle, which will be treated as salvage and must go through South Carolina’s rebuild and inspection process before it can be titled and driven again. A solid valuation helps ensure both the ACV and salvage value are fair: talk to our South Carolina appraisal team.

Will my South Carolina total loss payout include tax, title, and registration fees?

Many South Carolina total loss settlements include applicable sales tax and certain title and registration fees needed to replace your vehicle, but details can vary by insurer and policy. Always request an itemized breakdown that shows ACV, taxes, fees, and any deductions so you can verify you are being paid correctly.

What if I owe more on my auto loan than the total loss settlement in South Carolina?

If your loan payoff is higher than the total loss payment, you have negative equity. You’re typically responsible for that remaining balance unless you purchased GAP insurance or a similar add-on that can cover some or all of the shortfall. Because of this, having a properly supported ACV is critical—it can directly reduce how much you still owe after the claim.

How long do I have to pursue a property damage or total loss claim in South Carolina?

South Carolina law sets specific statutes of limitations for vehicle damage and injury claims. These deadlines can span multiple years, but the exact timeframe depends on your situation and may change if the law is updated. Missing a deadline can affect your rights, so it’s important to consult a South Carolina attorney if timing might be an issue. SnapClaim’s role is to provide a clear, data-driven valuation that your attorney or adjuster can use during negotiations: see how our South Carolina reports are used.

Does my South Carolina auto policy have an appraisal clause, and how does it work?

Many auto policies used in South Carolina include an appraisal clause for disputes over vehicle value. Typically, each side hires an appraiser; if they cannot agree, a neutral umpire reviews both positions and helps set the amount. This process usually applies when you’re making a claim under your own policy. A detailed SnapClaim report can support your position if you decide to invoke appraisal: South Carolina total loss appraisals.

Does SnapClaim work statewide in South Carolina, or just in bigger cities?

SnapClaim covers all of South Carolina—including Columbia, Charleston, North Charleston, Mount Pleasant, Rock Hill, Greenville, Summerville, and surrounding towns and rural areas. Our reports use hyper-local comparable vehicles so your valuation reflects real South Carolina market conditions, not just national averages. You can start from our South Carolina overview page: SnapClaim South Carolina hub.

How fast can I get a South Carolina total loss appraisal from SnapClaim?

Most South Carolina total loss appraisals are completed the same business day after we receive your claim information and supporting documents—often within about an hour. That speed helps you respond quickly to a low offer instead of letting the claim drag on. Get started here: request a South Carolina total loss appraisal.

How does a SnapClaim report help South Carolina drivers and law firms negotiate better payouts?

SnapClaim builds a South Carolina–specific valuation file using verified comparables, mileage and condition adjustments, options, and market corrections for your part of the state. The report explains how ACV should be calculated and highlights where the insurer’s number may be too low, giving adjusters and attorneys a clear basis for pushing for a higher settlement: learn how our fair market value reports work.

Diminished Value & Total Loss Appraisal Reports

Instant Free Estimate

Instant diminished value and total loss appraisals — no guesswork, no delays, backed by a 100% money-back guarantee.

Free Estimate, no credit card required.