Total Loss Appraisal in Missouri

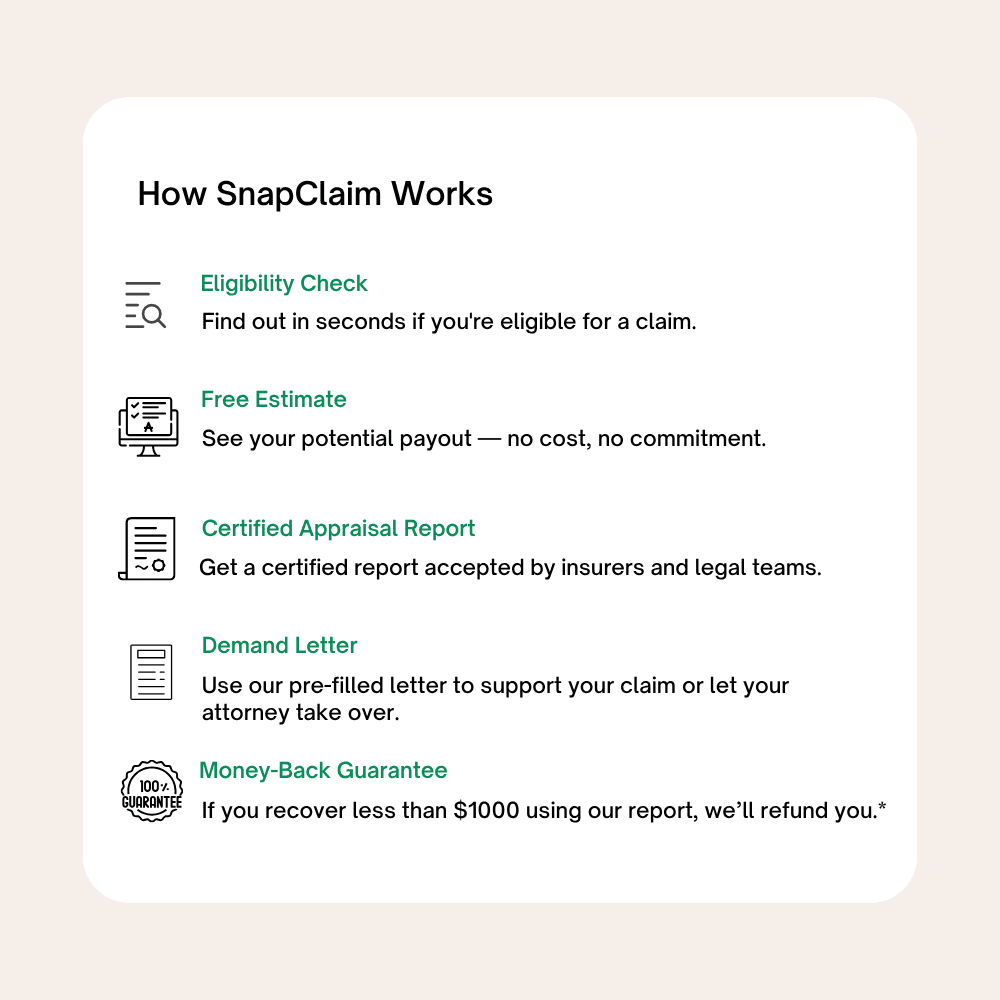

Get Your Free Estimate in minutes.

If your car was declared a total loss and you’re not happy with the insurance payout, you have the right to request a Missouri total loss appraisal. SnapClaim helps you dispute unfair insurance valuations with certified, data-backed reports that show your vehicle’s true fair market value.

No credit card required [Takes less than 30 second]

Total Loss Appraisal in Missouri: What You Need to Know

Missouri Total Loss Appraisal — Dispute a Low ACV Offer & Get a Fair Settlement

If your vehicle was declared a total loss in Missouri and the insurance offer doesn’t reflect what it would actually cost to replace your car, you can challenge that valuation with an independent Missouri total loss appraisal.

From Kansas City, St. Louis, Springfield to Columbia, Independence, Lee’s Summit and communities statewide, SnapClaim helps Missouri drivers and attorneys push back against inaccurate insurance valuations using local, defensible market data.

Our certified total loss appraisal reports are data-driven, USPAP-aware, and insurer-ready — frequently used in negotiations, appraisal clause disputes, and small-claims proceedings across Missouri.

Why Get a Total Loss Appraisal in Missouri?

Missouri vehicle pricing varies significantly between major metro areas and smaller regional markets. Automated valuation tools often miss these differences, especially when they rely on broad regional averages or incorrect vehicle data.

- Meaningful pricing gaps between Kansas City / St. Louis and smaller Missouri cities

- High demand for reliable commuters, family SUVs, and pickup trucks

- Urban vs. suburban market differences often ignored by valuation software

- Trim levels and option packages frequently miscoded in CCC or Mitchell reports

CCC, Mitchell, or Audatex valuations may underprice Missouri vehicles by using distant comparables, applying unsupported condition deductions, or overlooking equipment that materially impacts value. A SnapClaim appraisal focuses on Missouri-relevant comparables and transparent adjustments.

Common Reasons to Question a Missouri Total Loss Offer

- Incorrect trim, drivetrain, or factory options listed on the valuation

- Comparables sourced from cheaper or non-representative markets

- Large condition deductions without photos or repair documentation

- Mileage adjustments that don’t match local driving patterns

- Pickups, SUVs, or premium trims valued like base models

What’s Included in Your Missouri Total Loss Appraisal Report

- Full VIN-decoded analysis confirming trim, drivetrain, and installed features

- Comparable listings sourced from Missouri and nearby regional markets

- A clearly supported pre-loss fair market value (ACV)

- Adjustments for mileage, features, upgrades, and overall condition

- Documentation to support invoking the appraisal clause under your policy

- Optional expert support if the dispute escalates or involves legal counsel

Most Missouri total loss appraisals are completed in about 1 hour and can be sent directly to the insurance adjuster.

Missouri Total Loss Disputes & Appraisal Rights

Many Missouri auto insurance policies contain an appraisal clause allowing either party to dispute a vehicle’s value using independent appraisers. If the appraisers cannot agree, a neutral umpire may determine the final value.

How to Dispute a Total Loss Offer in Missouri

- Request the insurer’s valuation report (CCC, Mitchell, or Audatex).

- Review the report carefully for errors in trim, mileage, or condition.

- Order a SnapClaim total loss appraisal to establish true ACV.

- Invoke the appraisal clause if the insurer’s offer is unsupported.

- Negotiate using documented market evidence to support a higher settlement.

Missouri Market Insights

- Metro-area pricing often exceeds statewide averages used by insurers.

- High-mileage vehicles may be undervalued by generic valuation formulas.

- Pickups and family SUVs frequently command higher local demand.

- Suburban markets can show stronger pricing than nearby urban cores.

Example Missouri Case Study

Vehicle: 2021 Honda CR-V EX-L

Insurance Offer: $26,300

SnapClaim Appraisal: $30,800

Outcome: Settlement increased after submitting the independent appraisal

Helpful Missouri Resources

- Missouri Insurance — Consumer Resources

- Missouri Courts — Small Claims

- Missouri Department of Revenue

- NHTSA — Vehicle History Search

Ready to Get Your Missouri Total Loss Appraisal?

- No upfront payment required

- Most reports completed in about 1 hour

- Insurer-ready documentation with market-backed ACV

Related Missouri Locations

Click a pin to open the city’s total loss page.

Find your Missouri city below to order your Total Loss Appraisal.

Order Your Total Loss Appraisal

Get Your Appraisal Report and Demand Letter Now!

Free Estimate, no credit card required.

Dispute an Unfair Total Loss Offer in Missouri

If your car was declared a total loss in Missouri but the insurance payout seems too low, you don’t have to accept it. Under your policy’s appraisal clause, you can request an independent Missouri total loss appraisal to verify your vehicle’s true fair market value. SnapClaim makes it simple — get a certified total loss report, invoke your appraisal rights, and negotiate a higher settlement — all within minutes.

“After my sedan was declared a total loss following a multi-vehicle accident in Lee’s Summit, the insurance company’s offer came in far below what similar cars were selling for across Missouri. I ordered a SnapClaim appraisal, and their report clearly documented the true market value using regional comps. Once I submitted it, the insurer increased my settlement by more than $3,000.”

Hannah P.,

Lee’s Summit, MO

Missouri Total Loss – Frequently Asked Questions

When is a vehicle considered a total loss in Missouri?

Missouri total loss decisions are commonly handled using a Total Loss Formula (TLF) approach. A vehicle is generally treated as a total loss when the insurer decides it is not economical to repair because the cost of repairs plus salvage value approaches or exceeds the vehicle’s Actual Cash Value (ACV) immediately before the crash. See how Missouri compares to other states here: total loss laws by state.

What does Actual Cash Value (ACV) mean on a Missouri total loss claim?

ACV is your vehicle’s fair market value right before the accident. It should be supported by real Missouri listings and local pricing—markets can differ across the state (for example St. Louis, Kansas City, Springfield, Columbia, Independence, Lee’s Summit, O’Fallon, St. Joseph, and nearby areas)—then adjusted for year, trim, mileage, options, and condition. Learn how ACV should be calculated: Fair Market Value & ACV.

The Missouri total loss offer seems low — what should I review in the valuation?

Ask for the insurer’s full valuation report (CCC, Mitchell, Audatex, etc.) and check for: incorrect trim, missing packages/options, mileage errors, condition deductions that don’t match photos, or comps from cheaper out-of-area markets (including listings outside your Missouri region). Many drivers and law firms use an independent SnapClaim Missouri total loss appraisal to support a higher, data-backed ACV: order a Missouri total loss appraisal.

Should my Missouri valuation use St. Louis comps if I live near Kansas City (or vice versa)?

Not necessarily. St. Louis and Kansas City often price vehicles differently, and rural Missouri markets can differ again. If the insurer’s comps come from a region that doesn’t match where you would realistically buy a replacement vehicle, the ACV can be distorted. A Missouri-focused appraisal helps tie the value to the right local market: Missouri total loss appraisals.

Does Missouri use a fixed percentage threshold to total a car?

Missouri is often handled using the Total Loss Formula rather than a single published percentage. That means the decision often turns on whether repair costs plus salvage value are close to or greater than the vehicle’s ACV. Insurers may also declare an economic total loss based on safety and repair feasibility.

What happens to my title if my car is totaled in Missouri?

When a vehicle is processed as a total loss in Missouri, it is typically issued a salvage/branded title (or salvage documentation). If the vehicle is repaired, Missouri may require inspections and documentation before it can be titled and registered again. Salvage history can affect resale value and insurance options.

Can I keep my totaled vehicle in Missouri and repair it?

Often, yes. If you choose to retain the salvage, the insurer typically reduces your payout by the vehicle’s estimated salvage value. You keep the vehicle and then follow Missouri’s rebuild and inspection requirements before it can be legally driven again. A proper appraisal helps confirm ACV and salvage deductions are fair: talk to our Missouri appraisal team.

What if the salvage value deduction is too high?

Salvage value can vary depending on demand and how the insurer estimates it (auction bids, vendor tools, or generic tables). If you’re keeping the vehicle, ask for the supporting documentation behind the salvage number. An inflated salvage deduction can shrink your settlement, and an independent appraisal can help you dispute it: Missouri total loss appraisals.

Will my Missouri total loss payout include sales tax and DMV fees?

Some total loss settlements include applicable taxes and certain title/registration fees needed to replace the vehicle, but practices vary by insurer and policy. Always request an itemized breakdown showing ACV, taxes, fees, and deductions so you can verify accuracy.

The valuation says my Missouri car was in “poor condition” — how do I push back?

Condition adjustments should be supported by evidence. If the report applies heavy deductions for wear, prior damage, or missing features, ask the insurer to show the photos, inspection notes, and the exact line-item deductions. You can provide maintenance records, pre-loss photos, and dealership service history to correct the condition rating.

How long do I have to pursue a property damage or total loss claim in Missouri?

Missouri has statutes of limitations that set deadlines for property damage and injury claims. The applicable deadline depends on your facts and can change over time. Missing a deadline can affect your rights, so consult a Missouri attorney if timing may be an issue. SnapClaim supports negotiations with valuation reports: see how our Missouri reports are used.

Does my Missouri auto policy have an appraisal clause for ACV disputes?

Many auto policies used in Missouri include an appraisal clause for disputes over vehicle value (ACV). Typically, each side selects an appraiser; if they can’t agree, a neutral umpire helps decide the amount. This process is most commonly used when the claim is under your own coverage. A detailed valuation can strengthen your position: Missouri total loss appraisals.

Does SnapClaim work statewide in Missouri, including smaller towns?

Yes. SnapClaim supports valuations across all of Missouri—metro areas and rural communities. Our reports use hyper-local comparable vehicles so the valuation reflects real Missouri pricing instead of generic national averages. Start here: SnapClaim Missouri hub.