When your insurance adjuster tells you your car is “totaled,” it’s easy to picture a mangled wreck. But the reality is purely financial. Understanding what a car totaled insurance declaration means is the first step toward getting the fair compensation you deserve.

A “total loss” declaration simply means the estimated cost to fix your vehicle is more than its value right before the crash (minus its salvage value). This isn’t the final word—it’s the starting line for your settlement negotiation.

What a Total Loss Really Means for You

Hearing your car is a “total loss” can be jarring, but it’s an economic decision, not a statement on the severity of the damage. Insurance companies use a simple cost-benefit analysis: if the repair bill is higher than the car’s pre-accident value, they declare it a total loss and pay you out instead.

The Total Loss Threshold

Every state has a rule called the Total Loss Threshold (TLT). This is a set percentage of the car’s value. If repair costs exceed that percentage, the insurer must declare it a total loss. This rule prevents an insurance company from spending $10,000 to fix a car that was only worth $8,000 before the accident.

With the rising cost of parts and labor for modern vehicles, total loss declarations are more common than ever. Even moderate damage can trigger a total loss if the vehicle is packed with expensive sensors and electronics.

Why This Matters for Your Car Totaled Insurance Claim

Understanding this process is your best defense against a low settlement. When an insurer declares a total loss, they begin calculating your vehicle’s Actual Cash Value (ACV)—what it was worth the moment before the accident. That number becomes the foundation for your entire insurance total loss payout.

Here’s what you need to remember:

- A “totaled” car is about the math, not just the physical damage.

- The insurance company’s initial valuation is an opening offer, and it is almost always negotiable.

- This declaration is just the first step toward getting the fair compensation you’re rightfully owed.

How Insurers Calculate Your Settlement Offer

When dealing with a car totaled insurance claim, the settlement hinges on one key term: Actual Cash Value (ACV). This isn’t what you paid for the car or what you owe on your loan. ACV is what your specific vehicle was worth in your local market just moments before the crash.

The insurance adjuster’s job is to determine that number, typically by finding “comparables”—similar vehicles that have recently sold nearby. Unfortunately, this is where the process often works against you.

The Problem with Insurer Valuations

The first offer you get is built on the comps the adjuster chooses, and their selections can dramatically lower your payout. It’s a common tactic used to save the insurance company money.

For instance, an adjuster might use comps that:

- Have significantly more miles than your vehicle.

- Are a base model, lacking your car’s premium features or trim package.

- Are listed in a lower condition class (e.g., “fair” when yours was “excellent”).

- Come from a different, less expensive geographic market.

They may also apply unfair “condition adjustments,” deducting hundreds of dollars for minor, pre-existing scuffs or normal wear that had little impact on your car’s real-world value. The valuation report they provide might come from a third-party company known to favor insurers, producing a lower ACV that comes directly out of your pocket.

Decoding Your Car’s Actual Cash Value (ACV)

To protect yourself, you must carefully review the adjuster’s valuation report. Don’t just accept their number. Understanding the complete total loss calculation process for your vehicle is the most important first step you can take.

The table below breaks down key factors that determine your vehicle’s value and what to double-check.

| Factor | How Insurers Might Undervalue It | How to Verify Its True Worth |

|---|---|---|

| Mileage | Using comps with much higher mileage than your car. | Provide maintenance records or a recent inspection report showing your vehicle’s exact mileage. |

| Condition | Classifying your car’s condition as “average” or “fair” without justification. | Gather pre-accident photos, service history, and receipts for recent work (like new tires) to prove its excellent condition. |

| Options & Trim | Overlooking valuable factory options like a sunroof, premium sound system, or advanced safety features. | Provide your car’s original window sticker or use a VIN decoder to list all factory options accurately. |

| Location | Citing comparable vehicles from a different, lower-cost region to justify a lower value. | Research local listings on sites like Kelley Blue Book to find comps sold in your immediate market area. |

Knowing how to effectively deal with insurance adjusters is crucial. When you arm yourself with your own evidence, you shift the power dynamic and significantly improve your chances of getting a fair settlement.

Your Action Plan After a Total Loss Declaration

When the insurance company says your car is a total loss, it’s easy to feel pressured. This is the moment to slow down. A calm, strategic approach can make a thousands-of-dollars difference in your final insurance total loss payout.

The most important rule is to never accept the first settlement offer on the spot. That number is their opening bid. Politely thank the adjuster and tell them you need time to review the valuation report in detail.

Your Immediate Next Steps

Your first move is to request the insurer’s complete valuation report in writing. This document shows exactly how they calculated their offer. Once you have it, go through it line by line.

You are hunting for common errors that unfairly reduce your vehicle’s value. Look for:

- Incorrect Mileage: Is the reported mileage higher than what was on your odometer?

- Missing Features: Did they leave out your sunroof, premium sound system, or upgraded trim package?

- Wrongful Condition Rating: Did they label your well-maintained car as “average” or “fair” without justification?

- Poor Comps: Are their “comparable” vehicles from a cheaper market, or do they have accident histories?

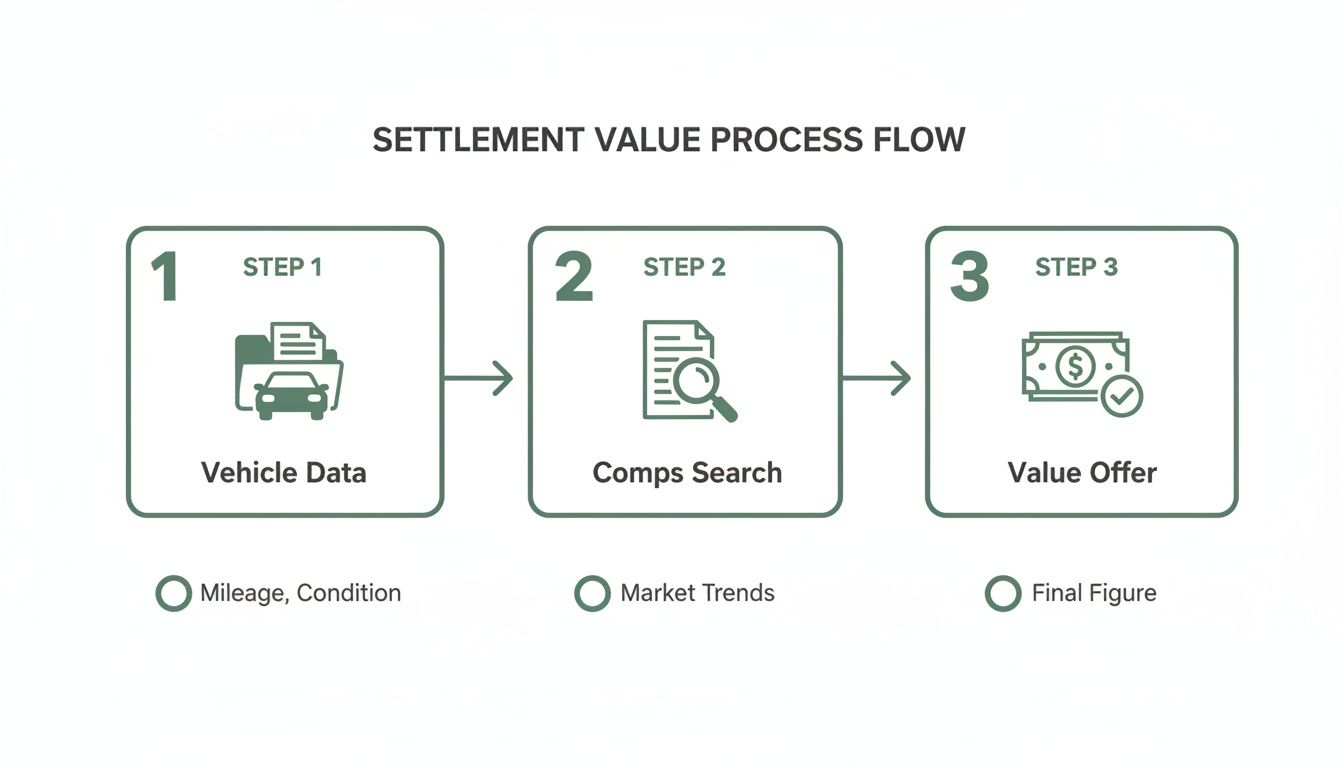

This flowchart breaks down the typical process insurers use to generate their offer.

As you can see, the final number is based entirely on the data they use—and that’s where mistakes frequently happen.

Gather Your Own Evidence

While the insurer builds a case for a low number, you must build yours for the right one. Gather real-world evidence to prove your car’s true pre-accident worth.

Collect documentation that demonstrates your vehicle’s value and excellent condition. This includes recent maintenance records, receipts for new tires or brakes, and any photos of your car taken shortly before the accident. This paperwork is your best weapon against lowball tactics.

By taking these steps, you are no longer passively accepting their offer. You are actively negotiating, armed with objective proof to challenge their numbers and secure the fair market value you are owed.

How to Dispute an Unfair Total Loss Offer

When a lowball settlement offer from your insurance company arrives, it’s easy to feel frustrated. But their first offer is just an opening move, not the final word. That number is almost always negotiable.

The key is to approach the dispute professionally and with solid evidence. This isn’t about emotion; it’s about building a factual, business-like case to prove your car’s actual pre-accident worth. Your goal is to shift the conversation from a simple disagreement to a data-driven negotiation.

Building Your Counter-Offer

A formal dispute begins with a well-structured counter-offer. This should be a clear, evidence-based document that systematically dismantles the flaws in the insurer’s valuation.

Your counter-offer should include:

- A Clear Statement of Dispute: State that you are rejecting their offer because it does not reflect your vehicle’s fair market value.

- Corrections to Their Report: List every error you found, from the wrong trim level to an unfair condition rating.

- Your Own Comparable Vehicles: Provide links to at least three to five local listings for cars that closely match your vehicle’s make, model, year, mileage, and features.

- Documentation of Value: Attach maintenance records, receipts for recent upgrades, and pre-accident photos to prove your car’s excellent condition.

The Power of an Independent Appraisal

While your own research is a critical first step, an independent, certified appraisal from a company like SnapClaim completely changes the dynamic. It provides the proof you need to negotiate fairly.

Instead of an argument based on your research versus theirs, you are presenting them with an objective, court-ready report from a qualified expert. A professional appraisal forces the adjuster to justify their lowball offer against industry-standard, verifiable data. It supports your case with certified data and strengthens your position immensely.

If you believe your claim has been wrongfully denied, it’s also important to understand how to appeal a denied insurance claim. For a detailed walkthrough on challenging an insurer’s numbers, see our complete guide on disputing a total loss offer.

Deciding What to Do with Your Totaled Car

Once you and the insurance company agree on a fair settlement, you have one last decision: what to do with the car. You have two main options, and each has very different outcomes.

The most common option is to surrender the vehicle to the insurance company. They pay you the full Actual Cash Value (ACV) you negotiated, and in return, they take possession of the car to sell at a salvage auction.

Keeping Your Totaled Vehicle

Your second option is “owner retention,” where you decide to keep the totaled car. In this case, the insurance company pays you the agreed-upon ACV, but first, they deduct the vehicle’s salavage value from the check.

Salvage value is the amount the insurer estimates they would have received for the car from a salvage yard. For example, if your car’s ACV is $15,000 and its salvage value is $2,500, your insurance payout would be $12,500. You get a smaller check, but you get to keep the car.

The Reality of a Salvage Title

The moment you keep your totaled vehicle, the state DMV brands it with a salvage title. This is a permanent red flag on the car’s history, indicating it was once declared a total loss. A car with a salvage title cannot be legally driven on public roads.

To get it road-legal again, you must:

- Complete all necessary repairs to meet strict state safety standards.

- Pass a rigorous state inspection to verify the repairs are sound.

- Apply for a “rebuilt” title only after passing the inspection.

This process is expensive and time-consuming. Even with a rebuilt title, you will face major headaches. Many insurers refuse to offer full coverage for rebuilt vehicles, and the car’s resale value will be permanently crushed—a clear case of diminished value. For most people, surrendering the vehicle is the cleanest and most financially sound decision.

Strengthen Your Car Totaled Insurance Claim with a Certified Appraisal

Insurance companies are businesses focused on minimizing payouts. When your car is totaled, the adjuster’s goal is to close your claim for the lowest amount possible. This puts you at a disadvantage, but you don’t have to accept their first offer.

A certified appraisal is the single most powerful tool for leveling the playing field. It shifts the conversation from your opinion versus theirs to a factual discussion based on hard data from an unbiased expert.

Why a Professional Report Works

A SnapClaim Total Loss Appraisal isn’t just a second opinion—it’s a data-backed, court-ready report built on the same industry standards that insurers are legally required to follow. Our certified methodology delivers the concrete proof needed to challenge an unfair offer with confidence. Instead of just saying, “I think my car is worth more,” you can provide an objective analysis that pinpoints exactly where their valuation went wrong.

This professional documentation helps strengthen your claim with certified data, forcing the adjuster to justify their lowball number against a report from a neutral, expert source. An independent appraisal is the definitive way to prove your vehicle’s true market value and ensure you get the full compensation you are rightfully owed.

A Risk-Free Way to Secure Your Payout

Dealing with a total loss is stressful enough. That’s why we stand behind our reports with SnapClaim’s Money-Back Guarantee. If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee—guaranteed.

By ordering a certified total loss car appraisal, you get the leverage you need to negotiate fairly, without the financial risk.

Frequently Asked Questions

What happens if I still owe money on my totaled car?

If your insurance settlement is less than your auto loan balance, you are responsible for paying the difference. This is often called being “upside down.” If you have Gap (Guaranteed Asset Protection) insurance, it will cover that gap. Otherwise, the remaining loan balance must be paid out of pocket after the insurance check is applied.

Can I negotiate the salvage value if I keep my car?

Yes. Just like the car’s Actual Cash Value, the salvage value is often negotiable. The insurer gets quotes from local salvage yards to determine this number, but those can vary. If you feel the salvage deduction is too high, research what similar wrecked vehicles are selling for at local auctions and present that data to your adjuster to negotiate a lower deduction.

Does my policy cover a rental car after a total loss?

This depends on your specific policy. If you have rental reimbursement coverage, it typically pays for a rental up to a daily limit for a set number of days. However, this coverage usually ends the moment the insurance company makes a formal settlement offer on your totaled car. Confirm the exact cutoff date with your adjuster to avoid an unexpected bill.

Can I claim diminished value on a totaled car?

No, a diminished value claim applies only to vehicles that have been repaired after an accident. Since a totaled car is not repaired, its value loss is covered by the Actual Cash Value (ACV) settlement. If your car is repaired, you can learn more from our Diminished Value guides.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes. Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step. Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.