Has an insurance adjuster declared your car a “total loss”? This isn’t a judgment on your vehicle; it’s a business decision that means the cost to repair it is more than its value right before the accident. Understanding this is the first step toward securing the fair insurance total loss payout you deserve. Here you learn about car appraisal for a total loss vehicle

What a “Total Loss” Declaration Really Means

Hearing your car is “totaled” can be a shock, raising more questions than answers. The core issue is a simple formula: if the repair bill is higher than the car’s Actual Cash Value (ACV), the insurer will write it off. ACV is just industry-speak for what your car was worth moments before the crash.

Here’s the problem: the insurance company’s first settlement offer is almost always just that—an offer. It’s typically low because insurers rely on automated valuation systems that don’t know about your vehicle’s excellent condition, the new tires you just bought, or what similar cars actually sell for in your area. Their goal is to close your claim quickly, which often results in a lowball payout for you.

Challenging the Initial Offer

You should treat the insurer’s number as an opening bid, not the final word. You have the right to question their valuation and present your own evidence to prove your car was worth more.

To successfully challenge a low offer, you need proof, not just a feeling. This is where an independent car appraisal for a total loss becomes your most valuable asset. It provides a detailed, data-driven report on your vehicle’s true market value, supporting your case with certified data.

An independent appraisal isn’t just a second opinion; it’s certified evidence. It replaces the insurer’s generic, computer-generated number with a professional valuation based on your car’s actual condition and real-world market data from a SnapClaim certified appraiser.

By understanding what a total loss means and preparing to counter the first offer, you can approach the process confidently and secure the settlement you’re actually owed.

How Insurers Calculate Your Car’s Value

Ever wondered how an insurance company arrives at its settlement offer? It’s a process that is often flawed and weighted in their favor, starting with something called the Total Loss Threshold.

Every state has one. It’s a specific percentage of a car’s pre-accident value, and if the repair cost exceeds that percentage, the vehicle is declared a total loss. This is why a car with seemingly moderate damage can still be “totaled.”

The Problem with Automated Valuations

To determine your car’s Actual Cash Value (ACV), insurers use third-party automated systems like CCC ONE or Mitchell. These platforms pull data from various sources to produce a quick valuation report.

However, these systems have built-in flaws that almost always result in a lowball offer. They often use outdated sales data from wholesale auctions, not what similar cars are selling for on dealer lots in your neighborhood.

This cookie-cutter approach consistently misses what makes your car valuable:

- Excellent Condition: The system might default your vehicle to “average” condition, ignoring that you kept it pristine and garage-kept.

- Recent Upgrades: New tires or a premium sound system? An automated report will almost certainly miss these valuable additions.

- Local Market Demand: A specific truck model might sell for a premium in your state, but a nationwide database won’t reflect that local market heat.

These platforms are built for speed and low cost, not accuracy. The number they generate is a starting point calculated to save the insurance company money. You can learn more about what determines the value of a totaled car and how to fight back against these undervaluation tricks.

A Growing Trend of Total Loss Claims

This reliance on flawed data is becoming more common. Total loss declarations have surged in recent years, with some reports showing over 30% of all auto insurance claims being written off. This trend is driven by skyrocketing parts and labor costs, which push repair estimates past the total loss threshold more easily.

Ultimately, the insurer’s calculation is engineered to minimize their payout. Understanding how they get their number—and its weaknesses—is the first step in building a strong case for the real compensation you deserve.

Why Total Loss Claims Are More Common Today

If you’re shocked that a seemingly minor accident totaled your car, you’re not alone. It’s happening more frequently because modern cars are incredibly complex. What used to be a simple bumper swap is now a high-tech repair job.

Today’s vehicles are packed with sophisticated technology like lane-assist cameras, parking sensors, and radar units. These components are part of your car’s Advanced Driver Assistance Systems (ADAS), and they are expensive to replace and recalibrate.

Even a fender-bender can damage sensors that cost thousands to fix. When the insurance company adds up the bill for parts, specialized labor, and calibration, the total often surpasses your car’s ACV. At that point, declaring it a total loss becomes the cheaper option for them.

The Role of Rising Repair Costs

It’s not just the tech. The cost of auto parts and labor has skyrocketed. A headlight that once cost a few hundred dollars can now easily top $2,000 if it’s an adaptive LED unit. This inflation means the bar for totaling a car is much lower than it used to be.

This isn’t just a new car problem. According to recent industry data, 74% of total loss valuations were for cars seven years old or older. As a car’s value drops with age, even a moderate repair bill can be enough to exceed its worth.

The decision to total a car is rarely about whether it can be safely driven again. It’s a purely financial calculation made by the insurer to cut their losses.

A car appraisal for a total loss is your counter-move. It ensures the value used in that calculation is accurate, helping you negotiate a fair settlement. It’s not personal; it’s business. Your job is to make sure it’s fair business.

Using an Independent Appraisal to Prove Fair Value

When facing an insurer’s lowball total loss offer, you need hard evidence. A certified, independent car appraisal for a total loss is your most powerful tool for proving your car’s true value.

An independent appraisal from SnapClaim provides a level of detail and real-world accuracy that an insurer’s automated report can’t match. It’s a deep-dive analysis of your specific vehicle, not a generic number from a national database.

What a Certified Appraisal Includes

A professional appraisal is more than just looking up your car’s make and model. A SnapClaim certified appraiser conducts a thorough investigation into what your vehicle was worth right before the accident.

This detailed process includes:

- A Meticulous Condition Review: The appraiser documents every detail that adds value, from a spotless interior to a flawless exterior, to capture its true pre-accident condition.

- Documentation of Upgrades: New tires, a premium sound system, custom features, or recent maintenance are all properly valued and factored in.

- Hyper-Local Market Analysis: Instead of broad auction data, the appraisal is built on actual sales of comparable vehicles in your specific local market, reflecting true demand.

An independent appraisal isn’t just a different number; it’s a legally defensible report built on verifiable data. It provides the concrete proof you need to challenge an insurer’s low offer and negotiate from a position of strength.

Why Local Market Data Is Critical

Value is local. A four-wheel-drive truck commands a higher price in Colorado than in Florida. Yet, the automated tools insurers use often miss these critical regional differences. An analysis of total loss trends shows how essential independent appraisals are for capturing the details that define a vehicle’s real value.

Focusing on your local market ensures the “comparable” vehicles used are actually comparable. The report you get is a data-backed argument for fair compensation. When you present that to an adjuster, you shift the conversation from a disagreement to a fact-based negotiation.

Once you have this report, it’s crucial to know how to use it. You can learn to leverage every part of the document by reading our guide on how to read an appraisal report.

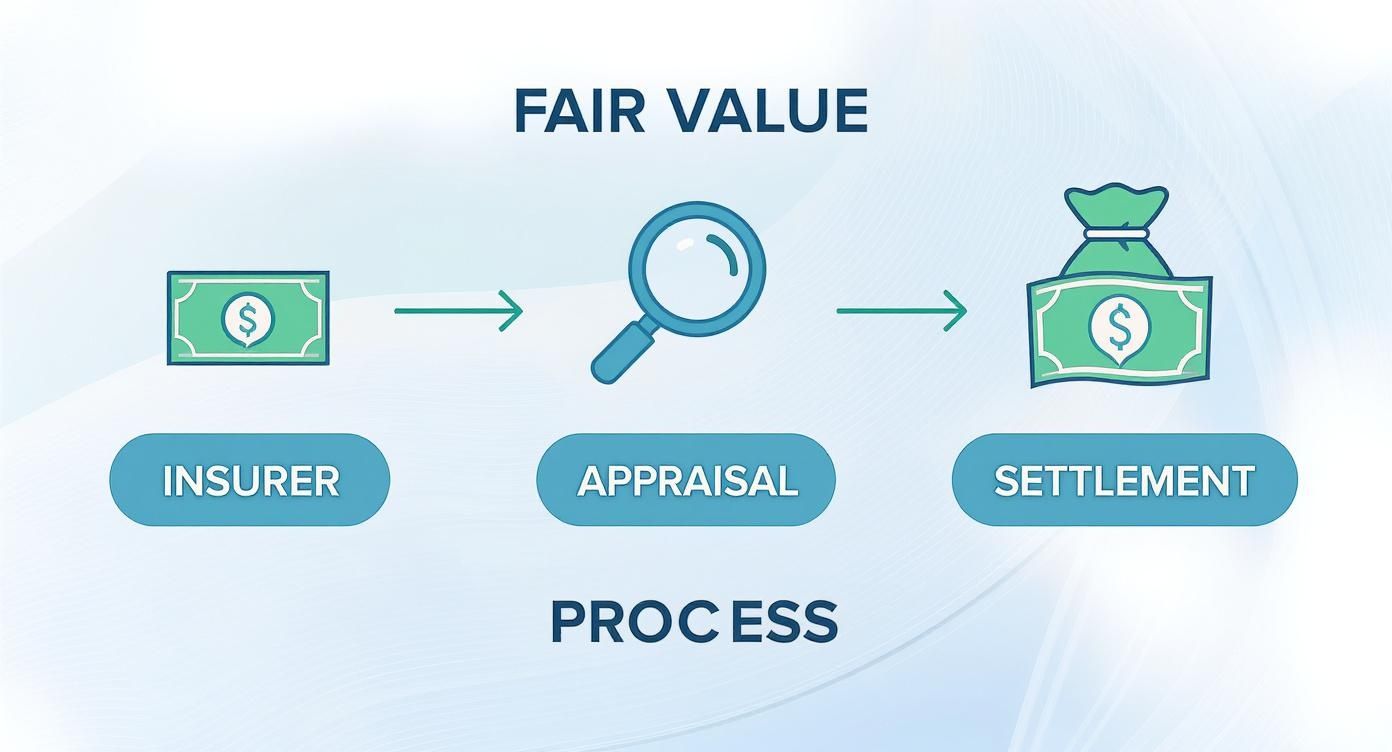

Your Step-by-Step Guide to a Fairer Settlement

Receiving a lowball settlement offer is frustrating, but it’s just their opening move. You have the right to negotiate, and with the right strategy, you can build an airtight case for the money you’re owed. The key is to be prepared with undeniable proof.

This diagram shows the journey from that initial low offer to a fair settlement, highlighting where an independent appraisal changes the game.

As you can see, a certified appraisal replaces the insurer’s opinion with a valuation grounded in real-world data, shifting the dynamic of the negotiation.

1. Politely Decline the First Offer

When the adjuster calls, don’t accept their offer. Thank them, calmly state that you believe the value is too low, and let them know you’ll be sending your own documentation for review. Keep it professional; this is a business negotiation.

2. Request the Insurer’s Valuation Report

Ask the adjuster to email you a full copy of their valuation report (often from CCC ONE or Mitchell). This document is the blueprint for their offer. You need to see which “comparable” vehicles they used to find weaknesses in their argument.

3. Gather Your Own Evidence

Now it’s time to build your case file. Pull together all proof demonstrating your vehicle’s value and pre-accident condition. Don’t leave anything out.

Essential Documents for Your Total Loss Claim

| Document Type | Why It’s Important |

|---|---|

| Maintenance & Service Records | Receipts for oil changes, new tires, and brake jobs prove the vehicle was well-maintained. |

| Original Window Sticker | If you have it, this lists every factory option and package, which all add value. |

| Recent Photos & Videos | Pre-accident images showing the car’s pristine condition counter low “condition” ratings. |

| Aftermarket Upgrade Receipts | Proof of custom wheels or stereo systems that increase the car’s value. |

| Bill of Sale | Shows your original purchase price and helps establish a baseline value. |

Having these documents ready shows the insurer you are serious and prepared.

4. Order a Certified Car Appraisal

This is your most powerful tool. A certified, independent car appraisal for a total loss from SnapClaim delivers a detailed, market-based valuation of your specific vehicle. It digs into your local market, accounts for your car’s unique condition, and provides a defensible number that stands up under pressure.

5. Submit a Formal Counteroffer

With your appraisal and supporting documents, it’s time to push back. Draft a clear, professional email that rejects their initial offer and presents your counteroffer. Reference your independent appraisal report as the basis for your new figure. If your accident also involved injuries, you might need to include this as part of a powerful personal injury demand letter template.

6. Invoke Your Policy’s Appraisal Clause

If the insurer still won’t budge, your policy likely contains an “Appraisal Clause.” This contractual right lets both you and the insurer hire your own appraisers. Those two appraisers then agree on a neutral third appraiser (an umpire) to make a final, binding decision. It’s an effective tool for breaking a stalemate.

Frequently Asked Questions (FAQ)

Can I keep my car if it’s a total loss?

Yes, in most states, you have an “owner retention” option. The insurance company will pay you the car’s actual cash value minus its salvage value. You will then receive a salvage title and be responsible for all repairs.

How long does a total loss settlement take?

The timeline varies, but a typical settlement takes 30-45 days. Disputing the insurer’s offer can slow things down. However, providing an independent car appraisal for a total loss upfront can speed up the process by providing undeniable proof of your car’s value.

What if my insurance company rejects my appraisal?

This is where the “Appraisal Clause” in your policy comes in. This clause is a contractual right allowing you and your insurer to each hire a certified appraiser. The two appraisers then select a neutral third-party appraiser (an umpire) whose decision on the value becomes binding.

Can I claim diminished value if my car is a total loss?

No. A diminished value claim applies when your car is repaired after an accident, leaving it with a lower resale value. Since a total loss vehicle is not repaired and resold in the same way, diminished value does not apply. Instead, your focus should be on getting a fair ACV settlement.

Get the Fair Settlement You Deserve

A total loss declaration doesn’t mean you have to accept a lowball offer. With the right evidence, you can successfully negotiate for the full value of your vehicle. A certified car appraisal for a total loss from SnapClaim provides the data-backed proof you need to strengthen your claim.

We are so confident in our certified methodology that we offer a Money-Back Guarantee. If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee — guaranteed.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes. Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step. Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.