If your car was just declared a total loss, you’re about to become very familiar with the term “Actual Cash Value” or ACV. It’s the single most important phrase in your insurance claim, and understanding it is the key to getting the fair payout you deserve.

So, what exactly is it? In simple terms, ACV is your car’s fair market value the moment right before the accident. It’s not a random number—it’s a specific calculation of its worth, and knowing how it’s determined will empower you to negotiate a better settlement.

What Actual Cash Value Really Means for You

One of the biggest surprises for drivers after an accident is learning that their insurance payout isn’t based on what they originally paid for the car. It’s also not based on what a brand-new replacement would cost.

Instead, insurers use a standard called Actual Cash Value (ACV). This is the amount a willing buyer would have paid for your specific vehicle right before the collision. It’s a snapshot of your car’s worth at that moment, nothing more.

The ACV calculation isn’t arbitrary. It’s a detailed assessment based on real market data and the unique characteristics of your car.

Key Factors That Determine Your Car’s Actual Cash Value

To figure out the actual cash value of your car, an insurance adjuster looks at several key data points. Each one can either push your settlement offer up or pull it down.

Here’s a quick rundown of what they analyze:

| Factor | How It Affects Your Car’s Value |

|---|---|

| Age and Depreciation | A car’s value naturally drops over time. Newer cars almost always have a higher ACV. |

| Mileage | The more miles on the odometer, the lower the ACV, as it suggests more wear and tear. |

| Overall Condition | This covers the interior, exterior, and mechanical state of your car before the crash. Pre-existing damage will lower the value. |

| Upgrades and Features | Premium add-ons like a sunroof, leather seats, or an advanced sound system can increase the ACV. |

| Local Market Demand | ACV is tied to what similar vehicles are actually selling for in your specific geographic area. |

Each of these elements helps paint a complete picture of what your car was worth pre-accident.

Ultimately, the insurance company’s job is to pay you for the fair market value of your lost property—not the cost to buy a new one. This is a critical distinction and why, if your car’s ACV is less than your loan balance, understanding the role of Gap Insurance can be a financial lifesaver.

Knowing these components empowers you to review the insurer’s offer with a critical eye and push back if it doesn’t accurately reflect your car’s true pre-accident worth.

How Insurance Companies Calculate Your Car’s ACV

Ever wondered how an insurer lands on that specific dollar amount for your car’s value? They don’t calculate the actual cash value of your car themselves. Instead, they hire large, third-party valuation firms to do it for them.

Firms like CCC ONE or Mitchell use sophisticated software to analyze massive databases of recent vehicle sales in your area. This process generates a detailed report that provides a data-driven basis for your settlement offer.

The Role of Comparable Vehicles

At the heart of any valuation report are comparable vehicles—often just called “comps.” These are real-world examples of cars just like yours that have recently sold in your local market. The software uses these comps to establish a baseline value.

A true “comp” should be a near-perfect match to your car in a few key ways:

- Make, Model, and Year: This is the absolute minimum for a fair comparison.

- Trim Level and Packages: A base model sedan is valued differently than a fully loaded sport-trim version. The report must account for those differences.

- Geographic Location: The valuation should be based on sales in your local area, not from a dealership hundreds of miles away where prices might be completely different.

The average sale price of these similar cars creates the starting point for your car’s valuation. From there, the adjuster makes specific tweaks based on your vehicle’s unique details.

Adjustments for Mileage and Condition

Once a baseline is set using those comps, the valuation software applies a series of adjustments. These are subtractions or additions designed to close the gap between your car and the comps.

The insurer’s report will apply specific dollar deductions for things like high mileage or pre-existing cosmetic flaws. On the other hand, it should also add value for premium features, recent upgrades, and exceptionally low mileage.

This is where things often go wrong. The adjustments are frequently based on automated formulas that don’t see the whole picture. For instance, a report might make a heavy deduction for minor flaws while completely ignoring the brand-new tires you just bought.

Understanding this process of comps and adjustments is your biggest advantage. It shows you exactly where an insurer might be undervaluing your claim, giving you specific points to negotiate a better insurance total loss payout. You can get a quick feel for these factors by using an auto actual cash value calculator to see how different inputs affect the value.

The Impact of Broader Market Trends

Beyond your car’s specifics, the valuation is also shaped by larger economic forces. The global auto market is always changing, and those shifts have a direct impact on your car’s value.

For example, worldwide vehicle registrations recently hit 37.4 million units, a 5% increase from the previous year, but that growth wasn’t spread evenly. These regional differences affect the supply and demand for used cars, which in turn influences the actual cash value my car is assigned after a total loss. To see how these trends are tracked, you can read more about the latest auto industry market reports.

An insurer’s valuation system must keep up. If their data is outdated, it might not reflect a recent spike in demand for your particular model, leading to an unfair settlement offer.

Common Errors That Lead to Low Settlement Offers

An insurance company’s first settlement offer for your totaled car is rarely its best. That initial number usually comes from automated software that is notorious for common—and costly—errors that can leave thousands of dollars on the table.

Knowing what to look for is the first step in fighting back against a lowball offer. Think of the insurer’s report as a starting point for negotiation, not the final word on the actual cash value of your car.

Inaccurate or Unfair Comparable Vehicles

The entire foundation of an ACV report is its list of “comparable vehicles,” or “comps.” In theory, these are nearly identical cars that recently sold in your local area. In reality, this is where you’ll find the most frequent and significant errors.

Keep an eye out for these red flags:

- Distant Comps: The insurer pulls comps from a different city or state where cars are cheaper.

- Mismatched Trim Levels: Your top-of-the-line model is compared to a stripped-down base model, ignoring valuable features.

- Dealer vs. Private Party Sales: The report might use cheaper private-party sales data, which isn’t an accurate reflection of true retail market value.

Many of these problems come directly from the automated valuation systems insurers rely on. To learn more, see our guide on uncovering the flaws in CCC ONE Market Valuation Reports.

Overlooked Upgrades and Missed Maintenance

An automated system can’t know the real story of your car. It has no idea you just spent $2,500 on new tires or had the transmission professionally serviced last month.

An insurance valuation report is just a snapshot based on generic data. It’s up to you to provide specific proof of your car’s superior condition and recent investments to get a fair car value after accident.

For example, an adjuster might apply a standard deduction for a tiny scratch on the bumper but completely ignore the $3,000 premium sound system you had installed. Every receipt for a major repair or upgrade helps you build the case for a higher value.

Outdated Market Data

The used car market moves fast, and recent years have seen wild price swings. This means your car is likely worth more today than it was even a year ago.

The problem is, some insurance databases lag behind these trends, churning out valuations based on old, irrelevant data. If the insurer’s report is using comps that sold six months ago, it’s not reflecting today’s higher market value.

Pinpointing these errors—from bad comps to missed upgrades and stale data—is how you win. It gives you the factual arguments you need to challenge a low settlement and negotiate for the compensation you deserve.

A Step-by-Step Guide to Proving Your Car’s True Value

Feeling frustrated by a lowball settlement offer is normal, but this isn’t the end of the road. Now is the time to build your case and prove the true actual cash value of your car. With the right evidence, you can become an informed, confident negotiator.

This guide will walk you through the exact steps to gather the proof you need for a strong counter-offer.

Step 1: Collect Your Vehicle’s Paper Trail

First, gather every piece of documentation you have. This paper trail is your best line of evidence, proving your vehicle’s history, condition, and every investment you’ve made.

Start by pulling together these key documents:

- Vehicle Title: Confirms ownership and essential details.

- Service History: A complete record of routine maintenance shows you were a responsible owner.

- Repair Receipts: Receipts for major repairs prove you invested in the car’s longevity and performance.

- Upgrade Invoices: Any receipts for aftermarket additions—like a new sound system or custom wheels—add direct value.

This collection of documents tells a story that a computer-generated valuation can’t.

Step 2: Establish a Baseline with Online Tools

Next, get a general feel for your car’s market value using online valuation tools. Reputable resources like Kelley Blue Book (KBB) are a great starting point.

These sites let you enter your car’s details to generate an estimated value range. However, it’s critical to see these numbers for what they are: estimates. They often fail to account for your local market or recent upgrades, so use them as a reference point, but don’t stop here.

Step 3: Become a Local Market Detective

This is the most important step in proving the actual cash value of your car. You need to find real-world, comparable vehicles—or “comps”—listed for sale in your immediate area. An insurer’s report is only as good as its comps, and this is where they often get it wrong.

Hunt for listings on local dealership websites, AutoTrader, and Cars.com that are as close a match to yours as possible.

Pro Tip: Save screenshots and printouts of at least three to five strong comps. Your evidence should include the vehicle’s asking price, VIN, mileage, and trim level. The more similar the vehicle, the stronger your argument.

This research either confirms the insurer’s comps are fair or gives you concrete evidence to prove they are not.

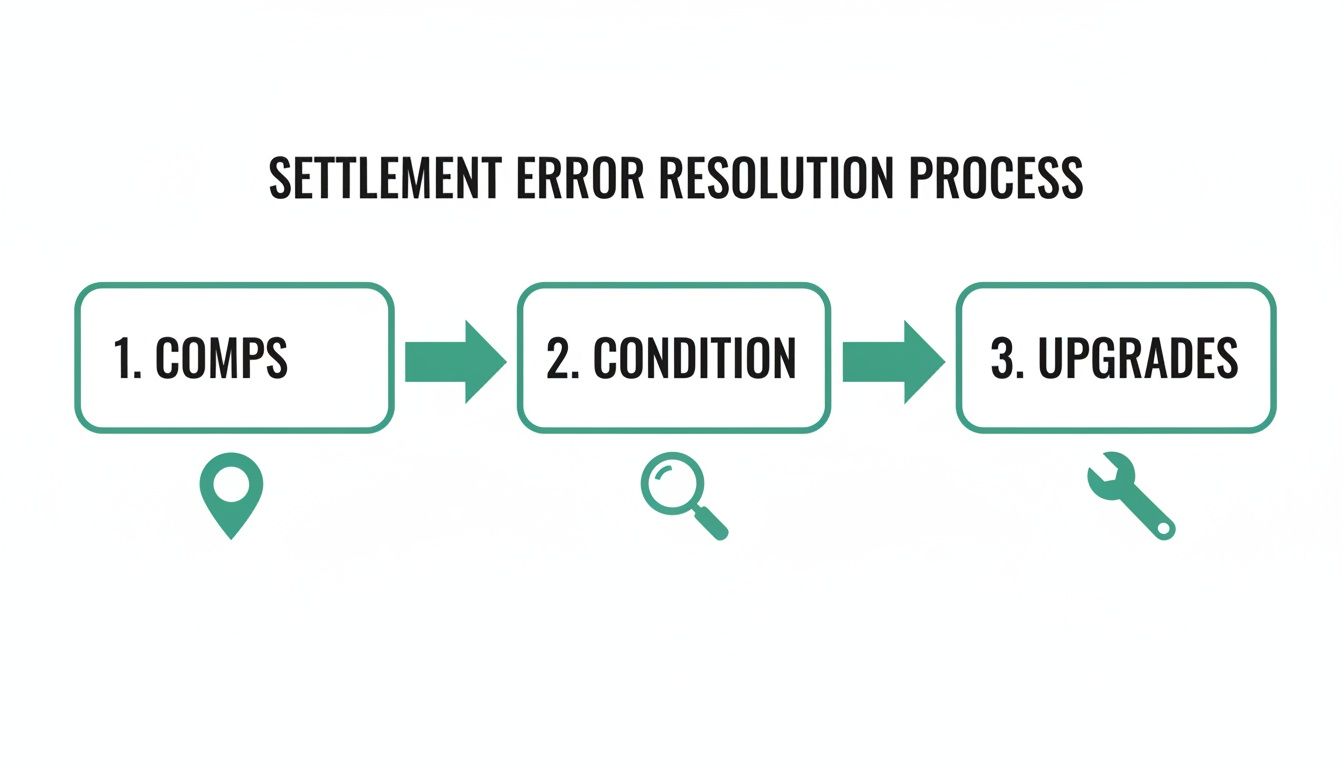

This simple flowchart shows the three key areas—comps, condition, and upgrades—where you can find and correct errors in the insurance company’s settlement offer.

Focusing on these three pillars lets you build a comprehensive case that directly challenges the most common flaws in an insurer’s valuation.

Step 4: Document Pre-Accident Condition and Present Your Case

Finally, pull all your findings together into a professional package. You aren’t just sending over random papers; you’re presenting a well-reasoned case file.

Your package should include:

- A brief, polite cover letter stating that you are disputing their initial offer.

- Copies of all your maintenance records, repair receipts, and upgrade invoices.

- The printouts of your local comparable vehicle listings.

- Any pre-accident photos you have that clearly show your car was in excellent condition.

This proactive approach turns the tables. Instead of just accepting a number, you are presenting a data-backed argument that compels the adjuster to re-evaluate their position. And remember, beyond total loss scenarios, understanding diminished value claims can also be crucial for recovering the depreciation your car suffers even after repairs—another key part of its true value.

How to Dispute a Low Total Loss Offer

So, you’ve done your homework and gathered the facts. You now have the evidence you need to push back against the insurance company’s low settlement. The next step is to present your case professionally.

Your goal is to make it easy for the adjuster to see why their first offer doesn’t line up with reality. The key is a clear, logical presentation that lets your data do the talking.

Your first move is to draft a formal counter-offer. It’s important to maintain a firm but polite tone. This isn’t about getting emotional; it’s about confidently presenting the facts.

Structuring Your Counter-Offer

Keep your communication simple and direct.

A straightforward structure works best:

- State Your Position: Open by clearly rejecting their initial offer. State that you believe the actual cash value of your car has been undervalued.

- Present Your Evidence: Lay out your findings one by one. List the comparable vehicles you found, including their prices and key features, and attach your proof.

- Include Your Documentation: Attach copies of your service records and receipts for recent major repairs or upgrades.

- Make Your Counter-Offer: End by stating the specific dollar amount you believe is fair, supported directly by your evidence.

This organized approach signals to the adjuster that you’re serious and ready to negotiate based on solid market data.

Invoking the Appraisal Clause

But what if the insurance company still won’t budge? Most auto insurance policies have a powerful tool that most people don’t know exists: the “appraisal clause.” This is a provision in your policy that outlines a dispute resolution process.

This clause gives you the right to hire your own independent appraiser when you can’t agree on your vehicle’s value. The insurer hires their own appraiser, and these two experts negotiate a fair settlement on your behalf.

If they still can’t agree, they bring in a neutral third appraiser (an umpire) who makes a final, binding decision.

The appraisal clause is your secret weapon for leveling the playing field. It takes the negotiation out of your hands and gives it to certified professionals.

Why an Expert Appraisal Is Your Strongest Asset

This is where a certified report from SnapClaim becomes your biggest advantage. While your own research is vital, a professional appraisal from SnapClaim provides undeniable, data-backed proof that an insurer simply can’t ignore.

Our reports are built to withstand scrutiny and deliver the definitive evidence needed to force a fair reassessment of your claim.

This matters now more than ever. Recent data shows that the total loss frequency in the insurance market hit a record 22%, making accurate valuations trickier and disputes more common. You can learn more about how market shifts impact total loss claims at Repairer Driven News. An expert appraisal cuts through that complexity, giving you a clear, defensible number grounded in today’s market.

Strengthen Your Claim with a Certified Appraisal

When negotiations stall, it’s time to bring in the professionals. A certified appraisal is the single most powerful tool for proving the true actual cash value of your car.

An insurer’s automated report is just that—automated. A certified appraisal, on the other hand, is a meticulous, personalized assessment of your specific vehicle. It’s built to withstand the scrutiny of claims adjusters because it speaks their language: verifiable data, transparent methods, and industry-standard analysis.

The SnapClaim Advantage

At SnapClaim, our reports are designed to be bulletproof. Our certified methodology digs into real-time market data to pinpoint your vehicle’s true, pre-accident worth.

Every report is reviewed and verified by a licensed appraiser, ensuring it meets the highest standards of accuracy. You’re no longer just disagreeing with the adjuster; you’re presenting them with professional proof that supports your case for a higher value.

A certified appraisal isn’t just a second opinion. It’s a professional valuation designed to be the final word on what your car was worth, providing the proof you need to negotiate fairly.

Our Money-Back Guarantee

We are so confident in the quality and impact of our work that we stand behind every report with a simple, no-nonsense guarantee.

Here’s our commitment to you: If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee—guaranteed.

This promise makes getting a total loss appraisal a completely risk-free step toward the fair compensation you deserve.

FAQs: Understanding the Actual Cash Value of Your Car

Dealing with a total loss claim is confusing. Here are straightforward answers to common questions about determining the actual cash value of your car.

How is ACV different from replacement cost?

Actual Cash Value (ACV) is your car’s market value right before the crash, including depreciation. Replacement Cost is an optional, extra-cost coverage that pays for a brand-new vehicle of the same make and model, with no deduction for depreciation. Standard auto policies use ACV.

Can I keep my car if it is a total loss?

Yes, in most states, you can choose to keep your vehicle in a process called “owner-retained salvage.” The insurance company will pay you the car’s ACV minus its salvage value (what they would have gotten for the wreck). Your car will then receive a salvage title, which makes it very difficult to insure or sell later.

What if I owe more than the ACV settlement?

This is called being “upside down” on your loan, and it happens when your loan balance is higher than the car’s ACV. The insurance payout goes to your lender first, and you are responsible for the remaining loan balance. This is the exact situation that GAP insurance is designed to cover.

Can I claim diminished value if the accident wasn’t my fault?

Yes. If the accident wasn’t your fault, you may be able to file a diminished value claim against the at-fault driver’s insurance. This claim is designed to compensate you for the loss in your vehicle’s resale value that occurs simply because it now has an accident history, even after perfect repairs. SnapClaim can help you determine if you have a valid claim.

Get your free estimate today or order a certified appraisal report to strengthen your insurance claim.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes.

Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step.

Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.

👉 Get your appraisal report today