When an insurance company declares your car a “total loss,” it can feel overwhelming. But here’s the single most important thing to know: you do not have to accept the first insurance offer on your totaled car. That initial number is just their opening bid in a negotiation, not the final word on what your vehicle was actually worth.

What Happens When Your Car Is Totaled?

So, what does “total loss” mean? It’s simply insurance-speak for when the cost to repair your car is more than its value right before the accident.

That pre-accident value is called the Actual Cash Value (ACV). Instead of paying for repairs, the insurer offers a settlement based on their calculation of your car’s ACV. The problem is, their calculation is designed to protect their bottom line, which is why that first offer is often disappointingly low.

Know Your Rights vs. The Insurer’s Offer

A fair settlement starts with understanding the difference between what you’re owed and what the insurer hopes you’ll accept. This table breaks it down.

| Your Rights as a Policyholder | What the Insurer's Offer Represents |

|---|---|

| To be paid your car's true market value before the accident. | An initial valuation, often from generic, automated data. |

| To negotiate the settlement based on solid evidence. | A starting point for discussion, not a final, non-negotiable figure. |

| To provide independent proof of value, like a certified appraisal. | The lowest amount they think you might accept to close the claim quickly. |

| To take your time to review the offer before making a decision. | A number that likely overlooks your car's unique features and condition. |

Simply put, you have the right to push back with facts and documentation.

Immediate Steps to Take After a Total Loss Offer

Before you start negotiating, you need to protect your claim. The rules for declaring a car a total loss can be fuzzy. For instance, you might wonder whether a car is considered totaled when airbags deploy, as that single event can sometimes be enough to trigger it.

Here are a few things you should do right away:

- Don’t Sign Anything: Never sign documents that release the insurer from liability or transfer your car’s title until you’ve agreed on a fair settlement amount.

- Demand the Valuation Report: Ask the adjuster for a copy of the report they used to calculate your car’s ACV. This is the key to understanding—and challenging—how they arrived at their low offer.

- Review Your Policy: Pull up your insurance policy and get familiar with the section on total loss claims. Know your coverage limits and any specific rules that apply.

Taking these steps puts you in control and prepares you to build a strong case for the compensation you deserve. To dig deeper, learn more about what to do when your car is a total loss in our complete guide.

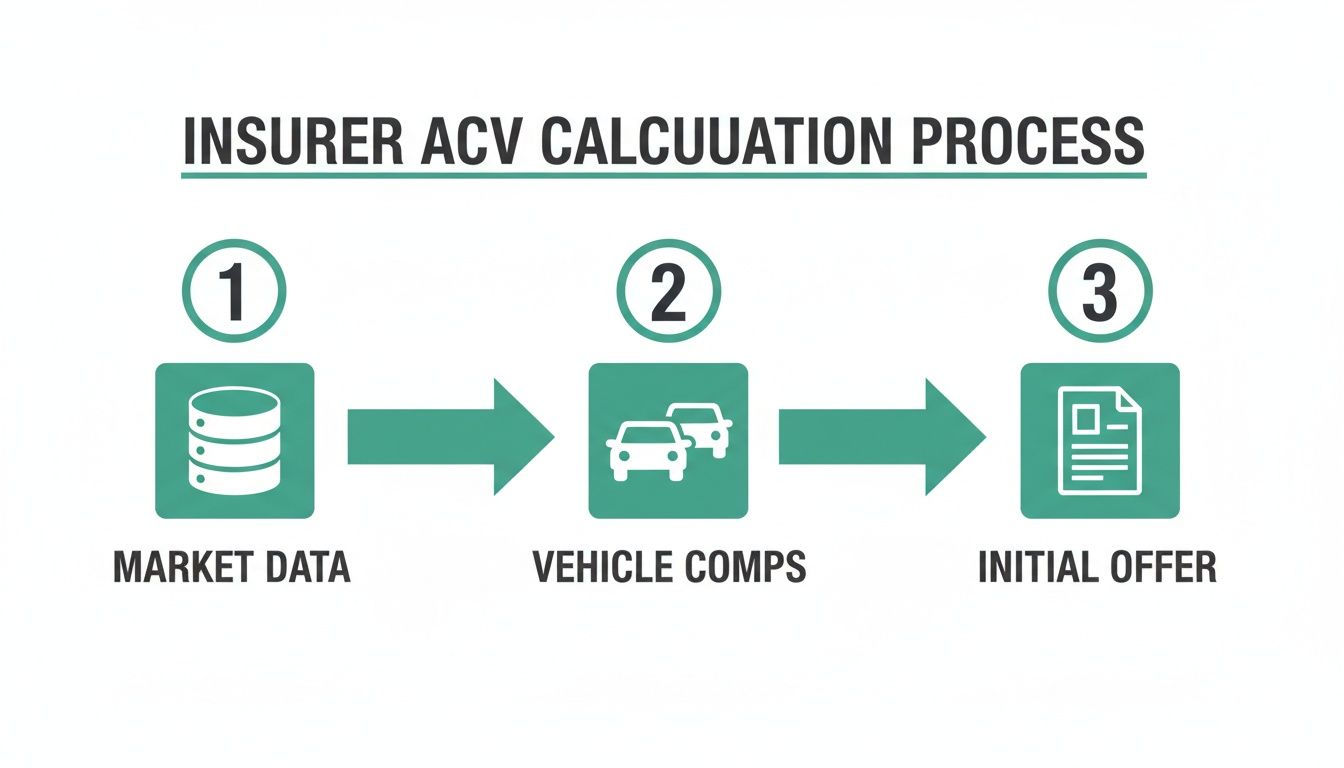

How Insurers Calculate Your Total Loss Offer

To negotiate a total loss claim successfully, you have to understand how the insurance company arrived at their number. The entire process revolves around one key term: Actual Cash Value (ACV). In simple terms, this is what your vehicle was worth the moment before it was damaged.

Insurers don’t guess this number. They use third-party valuation systems from companies like CCC Intelligent Solutions or Mitchell International. These platforms analyze market data by looking at recent sales of cars “like yours” in your area to generate a valuation report. But here’s the problem—these automated systems are often flawed.

Common Flaws in Insurer Valuation Reports

The valuation report from the insurer might look official, but it’s often an incomplete picture of your car’s real worth. Here are the most common ways these reports miss the mark:

- Poor Comparisons: The system often compares your well-maintained, low-mileage vehicle to “comps” with higher mileage, previous accidents, or a basic trim package. It’s not an apples-to-apples comparison.

- Missing Upgrades: Did you recently install new tires? What about a premium sound system or a tow package? Automated reports almost never factor in these value-adding features unless you provide proof.

- Incorrect Condition: Adjusters often assign a generic “average” condition rating without ever seeing your car’s pristine interior or knowing its perfect service history.

- Ignoring Local Market Data: The data pools these systems use can be too broad. They might not capture a surge in local demand for your specific make and model that drives up its value in your area.

Think of it like selling a house. You wouldn’t let a buyer ignore a brand-new roof or remodeled kitchen, would you? Your car is no different. Every upgrade and maintenance record is a bargaining chip that proves its real-world value.

This matters now more than ever. The rate of cars being totaled is increasing, with one analysis finding that 21% of collision claims in 2022 resulted in a total loss. With more cars being written off, insurers often undervalue vehicles to protect their profits. You can read more about these vehicle loss insurance trends to see how common this has become.

The bottom line is that the insurer’s report is just their opening offer. So when you ask, “do you have to accept an insurance offer on a totaled car?” the answer is no—especially once you know where to find the weaknesses in their report.

How to Dispute a Low Insurance Settlement Offer

Knowing you can reject a lowball settlement offer is one thing; doing it effectively is another. Disputing your insurer’s valuation isn’t about arguing. It’s about building a calm, evidence-based case that’s too solid for them to ignore.

Your first step is simple: put your rejection in writing. An email to the claims adjuster is sufficient. State clearly that you are rejecting their offer because you believe their Actual Cash Value (ACV) calculation is inaccurate and that you will be providing documentation to support a higher value. This officially starts the negotiation process.

Build Your Counteroffer with Solid Evidence

Your counteroffer can’t be based on feelings; it needs a foundation of proof. Hard data is what moves the needle, not emotion. Your goal is to show that your car was worth more than their generic valuation software determined.

As you can see, their process is often a high-level overview. Your job is to fill in the specific details about your car that their system missed. To do this, you’ll need to gather the right paperwork to showcase its unique value.

Your Counteroffer Documentation Checklist

Here’s a quick checklist of the essential documents you’ll need to build a strong counteroffer.

| Document Type | Why It's Important | Where to Find It |

|---|---|---|

| Maintenance Records | Proves the vehicle was well-cared for, directly impacting its condition and value. | Your mechanic's office, digital dealership records, or your personal files. |

| Receipts for Upgrades | Documents recent investments like new tires, brakes, or a battery that add immediate value. | Your glove box, email receipts, or credit card statements. |

| Original Window Sticker | Gold-standard proof of every factory option and trim package, which valuation tools often miss. | With your original purchase documents or sometimes available online by VIN. |

| Pre-Accident Photos | Powerful visual evidence to counter a low condition rating from the adjuster. | Your phone's photo gallery, social media posts, or family photos. |

Having these documents organized makes your counteroffer professional and difficult for an adjuster to dismiss.

Find Comparable Vehicles for Proof

Now for the knockout punch: real-world market data. The most convincing evidence you can present is what a car just like yours is actually selling for in your local area.

Search online auto listings for vehicles that are the same make, model, year, and trim.

Look for comps with:

- Similar mileage (aim for within 10-15% of your car’s).

- The same major options and features.

- Listings from local dealers in your immediate area.

Save screenshots of three to five solid examples. When you can show an adjuster that comparable cars are listed for thousands more than their offer, it’s tough for them to argue. As a general rule, it’s wise to not accept the first settlement offer after a car accident, because these initial numbers are so often based on incomplete data.

For a more detailed walkthrough, check out our step-by-step guide to disputing a total loss offer. While this evidence is powerful, your ultimate tool is a certified independent appraisal, which provides a defensible, expert valuation.

Using an Independent Appraisal to Get a Fair Payout

While your own research is powerful, an independent appraisal is your ultimate tool for leveling the playing field. This isn’t just a second opinion—it’s certified proof of your vehicle’s true fair market value from an unbiased expert. An appraiser works for you, not the insurance company.

This single step transforms the negotiation from a frustrating argument into a data-driven discussion. Suddenly, you’re holding a court-ready document proving what your car was really worth.

What an Expert Appraisal Report Provides

A professional appraiser conducts a deep, forensic analysis of your vehicle that goes far beyond the automated systems insurers use. They meticulously investigate every factor that contributes to its real-world value.

This includes a deep dive into:

- Specific Condition: The appraiser assesses the actual pre-accident condition of your car’s interior, exterior, and mechanical parts, moving past a generic “average” rating.

- Options and Packages: A real appraiser verifies every factory-installed option and special trim package—details that can easily add thousands to the value.

- Mileage and Maintenance: Your vehicle’s low mileage and consistent service history are properly weighted to reflect its superior condition.

- Local Market Analysis: They research current listings and recent sales of truly comparable vehicles in your immediate area to determine a real-time market value.

This detailed report replaces the adjuster’s subjective opinions with verifiable facts. It becomes the bedrock of your counteroffer, making it much harder for them to justify a low insurance total loss payout. Learn more about how a total loss car appraisal puts you in the driver’s seat.

A Risk-Free Way to Strengthen Your Claim

We understand that paying for an appraisal can feel like a gamble when you’re already dealing with a major financial hit. That’s why at SnapClaim, we’ve made the decision completely risk-free for you.

We stand behind our work with a simple promise. SnapClaim’s Money-Back Guarantee ensures that if your insurance recovery from the claim is less than $1,000, we will refund the full appraisal fee. This guarantee makes getting an expert valuation a secure investment in fighting for the fair settlement you deserve.

Understanding Your Final Settlement Options

Once you’ve negotiated a fair settlement for your totaled car, you’re at the final crossroads: what to do with the vehicle and the cash. Most people take the simplest route, but it’s smart to know you have other options.

The most common path is to accept the cash settlement. You sign the title over to the insurance company, hand them the keys, and they give you a check for the agreed-upon amount. It’s a clean break that lets you start shopping for a new vehicle. But there’s another choice, known as owner retention.

Should You Keep Your Totaled Car?

Owner retention means you choose to keep your damaged vehicle. If you go this route, the insurance company pays you the negotiated Actual Cash Value (ACV) minus the car’s salvage value. The salvage value is what the insurer estimates they could get for your wrecked car at a salvage auction.

This can be a smart move, but only in a few specific situations:

- The damage is mostly cosmetic. If the car is still safe and structurally sound, you might be able to live with the dents or get it fixed affordably.

- You’re a DIY mechanic. If you can do the repairs yourself, you can save a lot of money compared to a professional shop.

- The car has sentimental value. Sometimes a classic car or a family vehicle is worth restoring, regardless of market value.

Before you decide, you must check your local DMV rules. Every state has a strict process for dealing with salvage vehicles, which you can research on sites like DMV.org.

Keeping your car means it will be issued a salvage title—a permanent brand that follows the car forever.

The Reality of a Salvage Title

A salvage title completely changes your car’s future. To make it road-legal again, you’ll have to get it repaired to meet your state’s safety standards and then pass a rigorous inspection to earn a “rebuilt” title.

Even after all that work, its resale value is permanently damaged. A rebuilt title can slash a vehicle’s market price by 20% to 40%. Selling it later will be a significant challenge.

According to the Insurance Information Institute, the vast majority of drivers carry collision and comprehensive coverage, so total loss claims are incredibly common. You can discover more insights about auto insurance statistics to see how these trends are shaping claims today. Knowing all your options gives you the power to make the best financial decision.

You Are in Control of Your Total Loss Claim

If you take away one thing, let it be this: you are in control of your total loss claim. You absolutely do not have to accept an insurance offer on a totaled car, especially the first one. That initial number is a starting point, not the final word on what your vehicle was worth.

Now you understand how insurers calculate their lowball offers and, more importantly, how to fight back. By gathering evidence and getting a certified independent appraisal, you shift the power dynamic and can negotiate from a position of strength. This isn’t about getting a windfall; it’s about making sure you can replace what you lost without paying out of pocket due to an undervalued settlement.

With this knowledge, you can approach the claims process with confidence. Your next move is to build a rock-solid case and fight for the fair insurance total loss payout you deserve. A certified appraisal from SnapClaim provides the undeniable proof you need to strengthen your claim.

Frequently Asked Questions About Total Loss Claims

How long do I have to accept or reject an insurance offer?

There is no immediate deadline, so don’t let an adjuster rush you. While timelines vary by state and policy, you have a reasonable amount of time to review the valuation report and gather your evidence. The absolute final deadline is your state’s statute of limitations for property damage—often two years or more—but you should aim to resolve it much sooner.

What if the insurance company refuses to negotiate?

If an adjuster won’t budge even after you provide evidence, check your policy for an “appraisal clause.” This provision allows both you and the insurer to hire independent appraisers to settle a value dispute. If that fails, you can file a complaint with your state’s Department of Insurance. As a last resort for a significant claim, you may need to consult an attorney.

Can I keep my car if it is declared a total loss?

Yes, in most states, you can. This is called “owner retention.” The insurance company will pay you the agreed-upon fair market value minus the vehicle’s salvage value. You will receive a “salvage” title, and you must follow your state’s specific laws for rebuilding, inspecting, and re-registering the vehicle to make it road-legal again.

Does my loan balance affect the total loss settlement?

No, it does not. Your outstanding loan has zero impact on your car’s actual cash value. The insurance company’s only obligation is to pay what the vehicle was worth just before the accident. If the settlement is less than what you owe, you are responsible for the difference. This is the exact scenario that GAP (Guaranteed Asset Protection) insurance is designed to cover.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes. Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step. Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.