When your car is declared a total loss, the insurance company’s first move is to generate a valuation report, often using a platform like Mitchell WorkCenter. This report sets the stage for their settlement offer, but it’s critical to remember one thing: it’s just a starting point, not the final word. Understanding how to read and challenge this report is key to getting the compensation you deserve.

Understanding the Mitchell WorkCenter Total Loss Process

If your adjuster mentions a Mitchell WorkCenter total loss report, they’re using a common software tool in the insurance industry. This system helps them calculate your vehicle’s Actual Cash Value (ACV)—a term for what your car was worth moments before the accident.

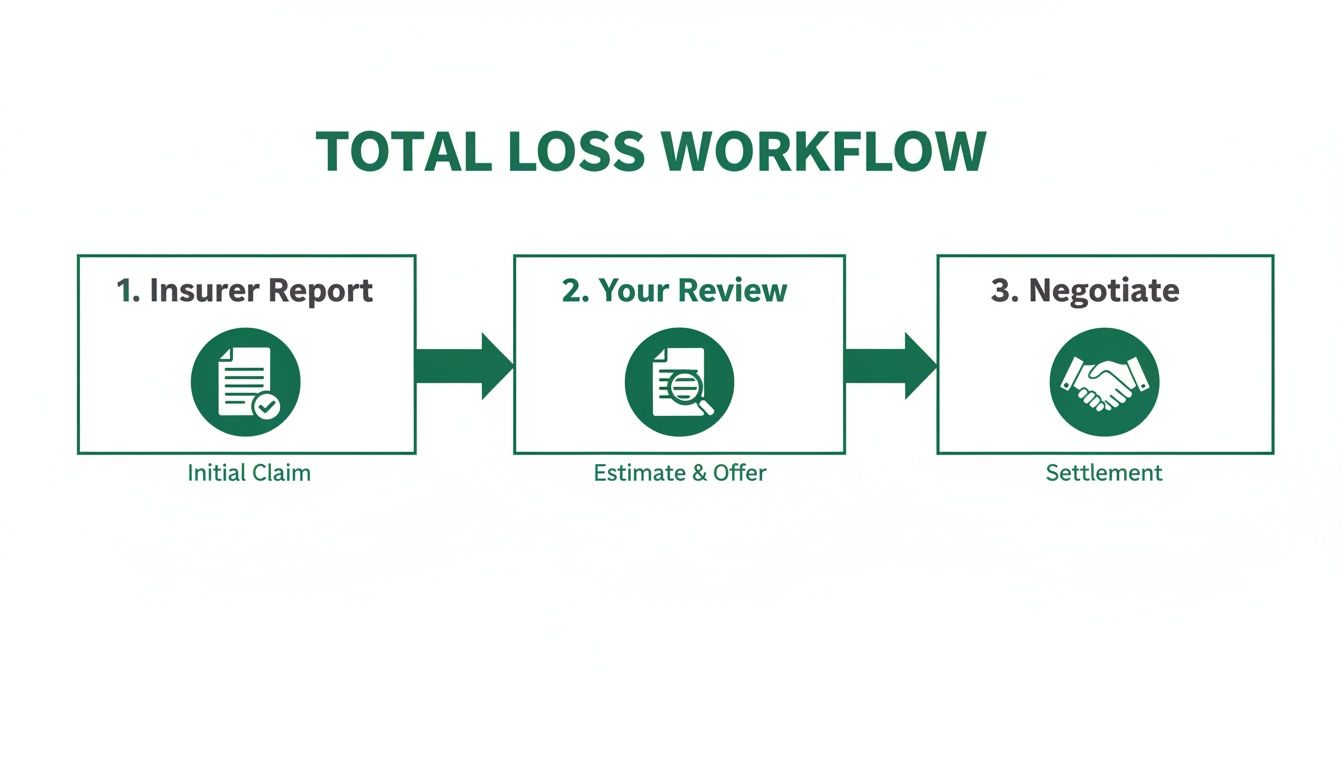

The problem is, the valuation is only as good as the data entered into it. Simple mistakes or overlooked details can easily lead to a lowball offer that doesn’t reflect your car’s true market value. The entire total loss process is a negotiation that starts with the insurer’s report.

As you can see, your review is the most important step. This is where you have the power to spot the errors that are costing you money and push back for a fair settlement. The table below breaks down the typical stages, giving you a clearer picture of what’s happening on their end.

| Key Stages of a Mitchell Total Loss Workflow |

| :— | :— | :— |

| Stage | Adjuster Action | Key Takeaway for Vehicle Owners |

| 1. Data Entry | The adjuster inputs your vehicle’s VIN, mileage, options, and pre-accident condition. | This is where most errors happen. Incorrect trim packages, missing options, or an unfair condition rating (e.g., “fair” instead of “good”) will lower the value. |

| 2. Comparable Search | The system searches for similar vehicles (“comparables” or “comps”) that have recently sold in your local market. | The quality of these comps is everything. The insurer might use vehicles with higher mileage, fewer options, or from a less relevant market area. |

| 3. Value Calculation | Mitchell applies adjustments to the comps to account for differences in mileage, options, and condition, then calculates an average ACV. | These adjustments are often based on generic formulas that might not reflect real-world market value. Scrutinize every line item. |

| 4. Report Generation | The adjuster generates the final total loss valuation report, which becomes the basis for the settlement offer. | Your job is to treat this report as a first draft. Never accept it without a thorough review. |

Ultimately, understanding this workflow demystifies the process and puts you in a much better position to challenge the insurer’s numbers effectively.

Why Are Total Losses Becoming More Common?

It’s not just you—more cars are being totaled now than ever before. The auto insurance industry saw total loss rates hit a record 22.8% of all collision claims. A big reason for this is the age of cars on the road; over 72% of total loss vehicles are seven years or older.

This trend makes it absolutely essential for you to understand how your settlement is calculated. Your goal is to ensure the insurer’s report accurately reflects your car’s pre-accident condition, features, and mileage. You can learn more about how to determine your car’s actual cash value in our detailed guide.

Getting the payout you deserve comes down to challenging inaccuracies with solid proof. An independent, certified appraisal report provides the data-backed evidence you need to strengthen your claim and negotiate from a position of power.

How to Read Your Mitchell Valuation Report

When you first see a Mitchell Workcenter total loss valuation report, it’s easy to feel overwhelmed. They are dense documents, loaded with charts, acronyms, and industry jargon. But learning to read this report is your most important move, as it’s the blueprint for the insurance company’s settlement offer.

Think of it this way: the insurer is showing you their math. Your job is to check their work. Breaking the report down piece by piece is the only way to find errors and push back against a lowball offer.

The Key Sections to Scrutinize

While the layout can vary, every Mitchell valuation is built on a few core components. Knowing where to look is half the battle.

- Vehicle Information: This sounds simple, but you’d be surprised how often mistakes happen here. Double-check the VIN, mileage, and especially the trim level (e.g., LX vs. EX-L). If they’ve listed your top-tier model as a base version, that’s a huge red flag that will tank the value right from the start.

- Condition Adjustments: The adjuster assigns a pre-accident condition rating to your vehicle—maybe “Excellent,” “Good,” or “Fair.” This is entirely subjective and a classic spot for insurers to chip away at the value. If your meticulously maintained car gets slapped with a “Fair” rating, the system automatically deducts money. Have your service records and photos ready to prove them wrong.

- Comparable Vehicles: This is the most important part of the report. Mitchell’s system pulls a list of supposedly similar vehicles that were recently sold or listed for sale to generate a “base value.” You need to pick these “comps” apart. Are they actually from your local market, or did the adjuster pull them from a cheaper area hundreds of miles away? Do they have similar mileage, features, and engine sizes?

Pro Tip: Insurers love to use “comparable” vehicles that aren’t comparable at all. A car with 20,000 more miles or a less desirable engine isn’t a fair comparison. Challenge every single one that doesn’t match up.

Finding the Red Flags and Flaws

Once you know the layout, you can start hunting for the common errors that lead to a low insurance total loss payout. It’s like a treasure hunt, but instead of gold, you’re finding the money the insurer tried to hide. If you want to see how this plays out with other valuation systems, you can learn more about the pitfalls of the CCC ONE market valuation report as well.

One of the biggest issues is the “Projected Sold Adjustment.” This is a blanket deduction insurers apply, assuming every car on the market sells for less than its asking price. The problem is, these adjustments are often arbitrary and don’t reflect what’s actually happening in the used car market.

As you dig into the numbers, having a tool to help you make sense of the data can be a game-changer. For anyone who’s comfortable with spreadsheets, a tool like Excel AI can be an intelligent partner to help you spot trends and inconsistencies.

Keep an eye out for these other classic red flags in your Mitchell report:

- Geographic Mismatches: Comps should come from your local area. An insurer using vehicles from another state or a rural market to value your city-based car is a tactic designed to undervalue your claim.

- Missing Options: Did they forget your sunroof, premium sound system, or that expensive tech package you paid for? Every feature adds value, and they need to be accounted for.

- Unfair Condition Deductions: Getting dinged for a few minor, age-appropriate scratches is just nickel-and-diming. Those small deductions can add up to hundreds of dollars.

By going through your Mitchell Workcenter total loss report with a fine-tooth comb, you stop being a passive recipient and become an informed negotiator. Document every single error you find—this is the evidence you’ll use to build a powerful counteroffer.

Challenging Common Valuation Errors in a Mitchell Report

Valuation tools like Mitchell WorkCenter are only as good as the data an adjuster feeds into them—and mistakes happen more often than you’d think. This is your playbook for spotting and fighting the most common errors that tank your settlement offer. Arming yourself with facts is the best way to counter their numbers and secure an accurate valuation for your Mitchell WorkCenter total loss claim.

Unfair ‘Dealer Ready’ Deductions

One of the sneakiest ways insurers lower your car’s value is through “dealer-ready” or “reconditioning” fees. Their argument is that your vehicle had normal wear and tear—like minor scuffs—that a dealer would fix before selling it. They then deduct the estimated cost of these fixes from your payout.

The problem? These deductions are often subjective and not based on real-world quotes for the work.

Key Takeaway: Your insurance policy is designed to make you whole by returning you to your pre-loss financial state. It’s not meant to restore your car to perfect, showroom condition. You should challenge any deduction that seems unreasonable for a vehicle of its age and mileage.

Inaccurate or Missing Vehicle Options

Did you pay extra for the premium sound system, a panoramic sunroof, or that pricey tech package? These features add significant value to your vehicle, but they’re frequently left off a Mitchell WorkCenter total loss report. An adjuster might list your top-tier trim as a base model, instantly wiping thousands of dollars off its value.

Your best defense is to gather your own evidence:

- Original Window Sticker: If you still have it, the Monroney label is the gold standard for proving every factory-installed option.

- Receipts and Invoices: Got new tires recently? A new battery? Document any major upgrades or recent repairs.

- Detailed Photos: Use pictures you took before the accident to highlight your vehicle’s features and pristine condition.

Presenting this proof to the adjuster forces them to acknowledge your car’s true configuration and recalculate the valuation.

Flawed ‘Comparable’ Vehicle Selections

The core of any valuation report is the list of “comparable” vehicles—the “comps”—used to establish your car’s market price. This is where adjusters have the most leeway to tilt the scales in their favor. A bad selection can dramatically reduce your insurance total loss payout.

Keep an eye out for these red flags:

- Geographic Mismatches: Using comps from another city or state where cars are cheaper is a classic move. A truck’s value in a rural town is completely different than in a major metro area.

- Mileage Discrepancies: A “comp” with 20,000 more miles on the odometer isn’t comparable at all.

- Condition Differences: The adjuster might use comps that were in clearly worse shape than your vehicle was pre-accident.

Global market trends also play a role. Factors like tariffs can impact claims costs and lead to more total loss declarations. You can learn more about how tariffs and tech are reshaping auto insurance from industry sources.

How to Build Your Case with Better Comps

Don’t just accept the insurer’s list of comps. Do your own research. Spend an hour on sites like AutoTrader, Cars.com, and local dealership websites to find vehicles that are a true match for yours in your area.

Save screenshots of any good listings you find, making sure to capture:

- Asking Price: Find vehicles with similar mileage, trim, and options.

- Vehicle Details: Get the VIN, mileage, and a full list of features.

- Location: Stick to dealers within a reasonable distance from your home.

Presenting the adjuster with a handful of better, more accurate local comps is one of the most powerful moves you can make. It forces them to address hard evidence from the real market.

Using a Third-Party Appraisal to Prove Your Car’s Value

When your insurance company’s Mitchell WorkCenter total loss report comes back with a value that just feels wrong, your strongest move is to get a certified, independent appraisal. This isn’t just a second opinion; it’s a rock-solid document built on real-world market data that replaces their questionable estimate.

A professional appraisal from a service like SnapClaim becomes the new anchor for your negotiation. It completely shifts the conversation from the insurer’s generic numbers to your vehicle’s specific, proven worth. It’s the tool that helps you negotiate for a fair settlement.

The Power of an Independent Report

The real difference between the insurer’s report and an independent appraisal is the methodology. The Mitchell system relies heavily on algorithms and historical data, often applying broad adjustments that may not reflect your local market. An independent appraisal is a detailed analysis from experts who dig into real-time, local market evidence to determine your vehicle’s true Actual Cash Value (ACV).

This screenshot from SnapClaim’s homepage shows the focus on providing data-driven, defensible reports for vehicle owners.

The key takeaway here is the emphasis on arming car owners with certified evidence, a world away from the often murky process insurers use.

Mitchell Valuation vs SnapClaim Certified Appraisal

Knowing the differences between these two reports is critical for your negotiation strategy. The insurer’s report is built to serve their interests, while an independent appraisal is designed to document objective market reality. Here’s a quick breakdown.

| Feature | Mitchell WorkCenter Report | SnapClaim Certified Appraisal |

|---|---|---|

| Data Source | Relies mainly on aggregated historical sales data and dealer listings, which can be outdated or from other regions. | Uses real-time, local market data, including current listings for comparable vehicles right in your area. |

| Condition Assessment | Based on a subjective, often brief inspection or photos, which leads to unfair “dealer-ready” deductions. | Considers your vehicle’s actual pre-accident condition, backed up by your documentation (photos, service records). |

| Adjustments | Often applies blanket negative adjustments like the “Projected Sold Adjustment” to drive the base value down. | Focuses on positive adjustments for valuable options, recent upgrades, and great condition, so all value is counted. |

| Goal | To land on a settlement figure that minimizes the insurer’s payout while sticking to general guidelines. | To establish the true, fair market value of your vehicle, giving you a strong, evidence-based negotiation tool. |

This comparison makes it clear why an independent report is so effective. It directly counters the weakest points of the insurer’s valuation with stronger, more relevant data.

Submitting Your Appraisal to the Insurer

Once you have your certified appraisal, you need to present it to the insurance company formally. This is more than just emailing a PDF; it’s about making a clear, professional demand for a revised settlement.

- Draft a Formal Letter or Email: Write a clear message to your adjuster. State that you are formally disputing their valuation from the Mitchell WorkCenter total loss report and are providing a certified appraisal reflecting your vehicle’s true market value.

- Attach the Full Report: Include the complete SnapClaim appraisal as a PDF. The full report contains all the data that justifies the final value.

- State Your Demand: Clearly state the valuation from your appraisal and request that the insurer revises their settlement offer to match it.

- Set a Deadline: Politely ask for a response within a reasonable timeframe, like 7-10 business days, to keep the process moving.

Expert Tip: Keep emotion out of your communication. Stick to the facts. Your argument isn’t about what you feel your car was worth; it’s about what the market data proves it was worth. Your SnapClaim report provides all the proof you need.

Overcoming Adjuster Pushback

It’s normal for adjusters to push back against an outside report. You might hear, “We can’t accept third-party appraisals.” This is a standard negotiation tactic.

Your response should be firm but professional: “My policy requires you to pay the Actual Cash Value, and your report fails to do that. This certified appraisal provides a more accurate analysis of the local market. Please review the data and provide a specific, factual rebuttal to my appraiser’s findings.”

This puts the burden of proof back on them to show—with evidence—why their valuation is more accurate than yours. You can learn more about how a professional car appraisal for a total loss strengthens your position. With a certified appraisal, you change the dynamic. You are no longer just questioning their numbers; you’re presenting a superior set of facts.

How to Negotiate Your Final Total Loss Settlement

With your independent appraisal in hand, you have the leverage to negotiate from a position of strength, backed by hard market data. This phase is about communicating clearly, staying professional, and steering the conversation toward a fair number based on facts—not the insurer’s flawed Mitchell WorkCenter total loss report.

The goal is simple: move the discussion away from subjective opinions and anchor it to the concrete evidence in your SnapClaim appraisal. This shifts the negotiation from an emotional argument into a business-like discussion about numbers and proof.

Frame the Conversation Around Facts

When you speak with the adjuster, your tone should be confident, professional, and firm. Don’t get pulled into debates about what you “feel” the car was worth. Instead, keep bringing the conversation back to the evidence.

Your opening line can be direct: “I’m formally disputing your valuation. I’ve obtained a certified appraisal that more accurately reflects my vehicle’s true pre-accident market value.”

From there, zero in on the key differences between their report and yours. Point to specific, data-backed items in your SnapClaim appraisal:

- Highlight Better Comparable Vehicles: “My report identifies three local vehicles with similar mileage and the same trim package, whereas your report used comps from over 200 miles away with fewer options.”

- Point Out Missed Features: “Your valuation overlooked my vehicle’s premium technology package and the new tires I put on last month, both of which are accounted for in my appraisal.”

- Question Unfair Deductions: “My appraisal correctly assesses the vehicle’s condition without applying a speculative ‘projected sold adjustment,’ which has no basis in our local market.”

When you do this, you control the narrative. The adjuster is now forced to defend their report’s specific flaws against your documented proof.

Responding to Common Adjuster Tactics

Insurance adjusters are trained negotiators and often use standard phrases to dismiss outside evidence. Knowing these tactics ahead of time is key to responding confidently.

You will likely hear, “We cannot accept third-party reports” or “Our policy requires us to use our own valuation tool.” This is almost always a bluff.

Your insurance policy obligates the company to pay you the Actual Cash Value (ACV) of your vehicle. It does not state they are the sole authority on what that value is. The method is secondary to the outcome—a fair payout.

A strong, professional response puts the burden of proof back on them: “My policy requires you to pay me the vehicle’s Actual Cash Value, and your initial report fails to do that. My certified appraisal provides a more accurate analysis. Please review it and provide a specific, data-driven rebuttal to its findings.”

This simple script is powerful because it forces them to engage with your evidence on a factual basis. They can’t just dismiss it; they have to prove why their data is better than yours.

The Importance of Detailed Record-Keeping

Throughout this process, document every single interaction. Meticulous records are your best friend if the dispute needs to be escalated. After every phone call, send a quick follow-up email summarizing what was discussed. For example: “Per our conversation today, you confirmed receipt of my appraisal and will provide a response within three business days.” This creates a paper trail that confirms timelines and verbal agreements.

Escalating Your Claim if Necessary

If the adjuster digs in their heels and refuses to negotiate in good faith, don’t be afraid to escalate. Politely ask to speak with their supervisor or a claims manager. A manager often has more authority to approve a higher settlement and may be more willing to resolve the dispute.

Remember, the total loss trend is growing, partly due to the aging U.S. vehicle fleet. Insurers are processing more total losses than ever and often rely on flawed, automated systems. You can read more about how the aging fleet contributes to this trend.

Your persistence, backed by a solid SnapClaim report, shows you understand the process and won’t be pushed into accepting an unfair offer.

Frequently Asked Questions About Mitchell WorkCenter Total Loss Claims

Navigating a Mitchell WorkCenter total loss claim can be frustrating. Here are answers to common questions vehicle owners have when fighting for a fair payout.

Can I reject the insurance company’s settlement offer?

es, absolutely. You are never obligated to accept an insurer’s first offer. It’s best to think of their initial Mitchell WorkCenter valuation as their opening bid in a negotiation, not the final word. You have the right to dispute their offer if you believe it undervalues your vehicle. The key is to counter their numbers with your own concrete evidence, like an independent, certified appraisal.

What is the “appraisal clause” in my auto policy?

l process for resolving valuation disputes when you and the insurer cannot agree on the vehicle’s value.

Here’s how it generally works:

You and the insurance company each hire your own independent appraiser.

Those two appraisers then select a neutral third-party appraiser, called an umpire.

A decision agreed upon by any two of the three becomes binding.

Starting the process with a certified SnapClaim report provides enough proof to resolve the dispute in many cases, often before you even need to invoke the appraisal clause.

What should I do if the adjuster says my vehicle’s options don’t add value?

his is a classic tactic used to justify a low insurance total loss payout. Adjusters often overlook—or conveniently omit—valuable options, packages, or recent upgrades in the Mitchell WorkCenter total loss report.

Your job is to prove those features add value with documentation:

The Original Window Sticker: This is the best proof of all factory-installed options.

Receipts and Invoices: Gather paperwork for major repairs, new tires, or aftermarket parts.

Detailed Photos: Use pictures taken before the accident to highlight your car’s pristine condition and special features.

A certified SnapClaim report properly documents these valuable add-ons, giving you the ammo you need to prove their contribution to your vehicle’s fair market value.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes. Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step. Our Money-Back Guarantee ensures you can strengthen your claim with zero risk: if your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee — guaranteed.

Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.