Hearing that your car is a “total loss” from an insurance adjuster can feel overwhelming. It’s a stressful moment, but it’s important to know this is a financial decision, not a final verdict on your vehicle. It simply means the insurance company calculated that repairing your car would cost more than its value before the accident.

This guide will walk you through exactly what to do with a totaled car, explaining your options and how to ensure you receive a fair insurance total loss payout.

Your Car Is Totaled—What Happens Next?

The moments after an adjuster declares your car totaled are often filled with questions. While it’s a jarring experience, you have more control than you might think. The most important thing to remember is that the insurer’s initial settlement offer is just that—an opening bid. You don’t have to accept it without doing your own research.

In simple terms, a vehicle is “totaled” when its cost of repairs plus its salvage value (what the wrecked car is worth) exceeds its Actual Cash Value (ACV) before the crash. ACV is a term for your car’s fair market value. State laws have different thresholds for this calculation, which you can explore on our state-specific law pages.

Understanding Your Immediate Options

Once your car is declared a total loss, you have three main paths you can take. Each one has different financial and logistical considerations.

Here’s a simple breakdown of your choices.

Your Immediate Options After a Total Loss Declaration

| Option | What It Means | Best For You If… |

|---|---|---|

| Accept the Payout | You sign over the title to the insurer, give them the keys, and they give you a check for the agreed-upon ACV. This is the most common choice. | You want a clean, straightforward resolution and need the funds to buy a replacement vehicle quickly. |

| Keep the Car (Salvage) | You decide to keep the wrecked vehicle. The insurer pays you the ACV minus the car’s predetermined salvage value. | The car has sentimental value, you’re a mechanic, or you plan to repair it yourself or sell it for parts. |

| Dispute the Valuation | You believe the insurer’s ACV offer is too low. You provide evidence of your car’s true market value to negotiate a better settlement. | You’ve done your research and are confident the insurer’s valuation is inaccurate and want to get what you’re rightfully owed. |

Each path requires a different approach, but the power to choose is yours.

Key Takeaway: An insurer’s first settlement offer is just a starting point. Never treat it as the final word. Knowing your car’s real value is the first and most critical step toward getting the compensation you deserve.

The journey from here involves understanding how insurance companies calculate their offers and how to effectively challenge them when they fall short. This is where a SnapClaim total loss appraisal becomes your most powerful tool, providing the certified proof you need to negotiate with confidence.

How Insurance Companies Decide a Car Is Totaled

When an adjuster says your car is a “total loss,” it can feel personal, but the decision is purely business. It has nothing to do with whether your car can be repaired. It’s all about whether it makes financial sense for the insurance company to pay for those repairs.

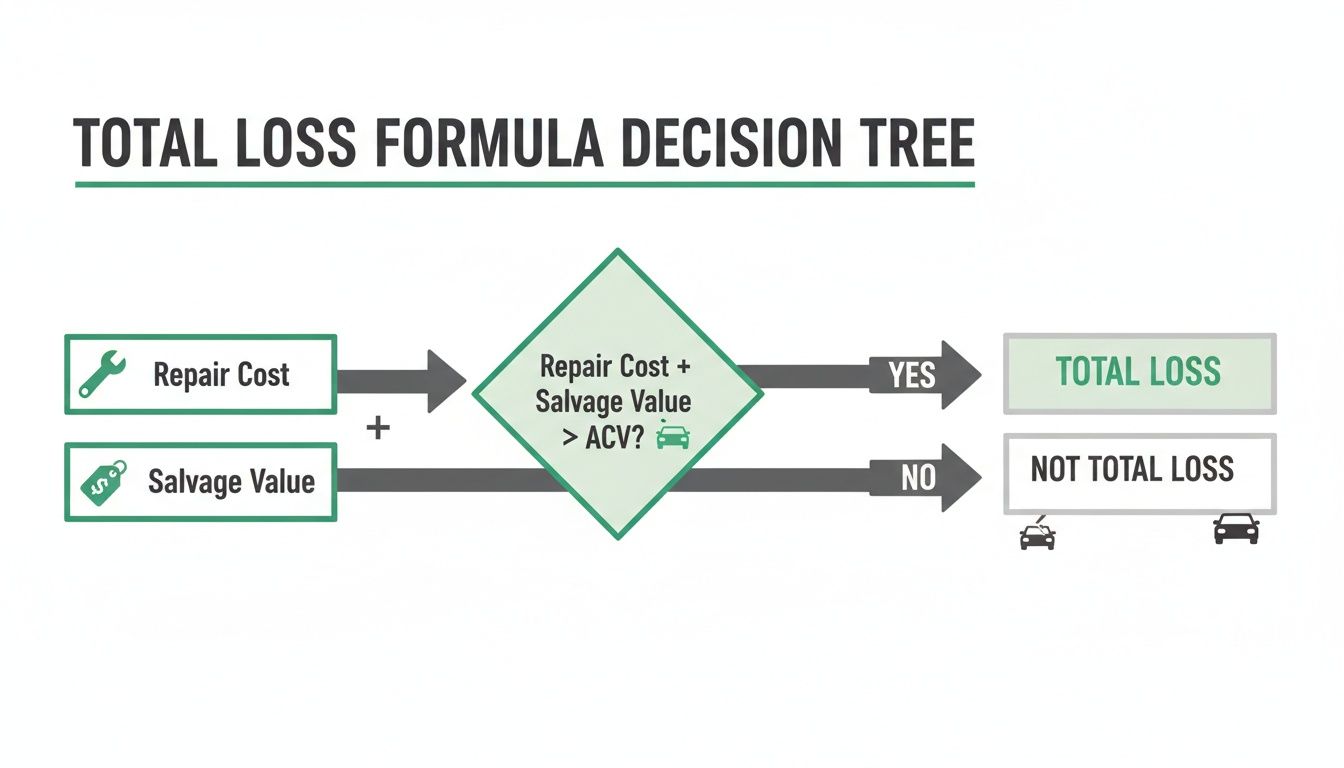

The entire decision comes down to a simple formula. Your car is declared totaled if:

Cost of Repairs + Salvage Value > Actual Cash Value (ACV)

Let’s break down these terms so you can see exactly how they make the call.

Understanding the Total Loss Formula

These three figures dictate everything. Getting a handle on them is your first step toward figuring out what to do with a totaled car.

Actual Cash Value (ACV): This is what your vehicle was worth on the open market the moment before the accident. It’s not what you paid for it or what you owe on your loan; it’s the price a reasonable buyer would have paid. This is almost always the most disputed part of a claim.

Cost of Repairs: This is the full estimate from a body shop to bring your car back to its pre-accident condition, including all parts and labor.

Salvage Value: This is the amount the insurer can recover by selling your wrecked car at a salvage auction. They are experts at recouping a portion of their payout this way.

The adjuster runs the numbers. If the repair cost plus the salvage value is more than the car’s ACV, it’s declared a total loss. Your state may also have specific laws setting a threshold, like 75% of the ACV, but the principle is the same. For a deeper look, check out our guide on calculating a total loss vehicle.

Why Modern Cars Total Out So Easily

It’s often shocking how a seemingly minor fender-bender can send a newer car to the salvage yard. The reason is that a small impact can damage thousands of dollars worth of technology hidden just beneath the surface.

Consider what’s packed into a modern bumper:

- Parking assist sensors

- 360-degree view cameras

- Radar systems for adaptive cruise control and collision avoidance

What looks like a simple dent now involves replacing and recalibrating expensive electronics, which requires specialized tools and skilled labor. All of that sends repair costs soaring.

The Reality of Modern Repairs: Even if a car looks drivable, a minor collision can easily generate a repair bill of $5,000 to $10,000. These high costs are a primary reason newer cars are totaled after what seems like minor damage.

The Impact of an Aging Vehicle Fleet

Another significant factor is the age of cars on the road. Older vehicles naturally have a lower ACV due to depreciation, making them much easier to total.

According to data from S&P Global Mobility, the average age of light vehicles in the U.S. has hit a record 12.5 years. This isn’t just a statistic; it has a massive impact on insurance claims. When a car with a low market value sustains even moderate damage, repair costs can quickly exceed its ACV.

At the end of the day, the insurer’s decision is purely economic. They are managing financial risk, not trying to save your car. This is why your focus shouldn’t be on the repairs—it should be on ensuring their ACV number is fair and accurate, as that figure determines your payout.

Your Three Main Choices for a Totaled Car

After the insurance company declares your car a total loss, you’re at a key decision point. It’s a stressful situation, but you have three distinct paths you can take.

Figuring out what to do with a totaled car is about understanding these choices and picking the one that makes the most financial sense for your situation.

As you can see, the decision is based on pure economics. When the cost to fix your car plus its scrap value (salvage value) is more than its pre-accident value, they write it off. Now, let’s explore your three primary responses.

Option 1: Accept the Payout and Surrender the Vehicle

This is the most common path. It’s clean, simple, and the quickest way to move forward.

You agree to the insurance company’s settlement offer for your car’s Actual Cash Value (ACV), sign over the title, hand them the keys, and they provide a check. The insurer then takes possession of the wrecked car and typically sells it at a salvage auction to recover some of their cost.

This option is a good fit if you:

- Want the fastest, simplest resolution.

- Need cash immediately to purchase another car.

- Have no interest in dealing with a heavily damaged vehicle.

The biggest risk here is accepting a lowball offer. Never take the insurer’s first number at face value without doing your own research.

Option 2: Keep the Car and Accept a Salvage Title

Many people don’t realize this is an option, but you can almost always choose to keep your totaled car.

If you go this route, the insurance company pays you the car’s ACV, but they subtract its salvage value. For example, if your car’s ACV was $15,000 and its salvage value is $3,000, they would send you a check for $12,000. You keep the car, but the DMV rebrands its title as a salvage title.

A salvage title is a permanent red flag that makes the car illegal to drive on public roads until it’s properly repaired and passes a rigorous state inspection. If it passes, it’s issued a rebuilt title.

Be Warned: A rebuilt title carries a permanent stigma. Securing full coverage insurance can be difficult, financing is often impossible, and its resale value is significantly lower than a car with a clean title.

This path is typically best for a select group—skilled mechanics who can do the work themselves or those who plan to sell it for parts. Be sure to check your state’s laws, as the process for obtaining a rebuilt title can be complex.

Option 3: Negotiate or Dispute the Insurer’s Valuation

This is where you take back control. You are under no obligation to accept the insurance company’s first offer, especially if you feel it’s too low. This is your chance to become an active negotiator.

Your success depends entirely on the evidence you provide. Simply stating you “feel” the car is worth more won’t work. You need to build a strong case with concrete facts.

Here’s how to arm yourself to fight a low settlement offer:

- Compile Your Records: Gather all maintenance receipts and proof of recent upgrades, like new tires or a brake job. This documentation shows your car was well-maintained.

- Find Real-World Comparables: Search for vehicles of the exact same make, model, year, and trim with similar mileage that have recently sold in your local area. Use local dealer listings, not just national estimators.

- Get a Certified Appraisal: This is your most powerful tool. An independent, certified appraisal from a service like SnapClaim provides an unbiased, data-backed report on your vehicle’s true fair market value.

A professional report is not just an opinion—it’s market evidence. It forces the adjuster to justify their low number against verifiable data and provides the proof you need to negotiate fairly for the full compensation you deserve.

How to Dispute a Low Settlement Offer

Receiving a settlement offer should feel like a relief, but for many, it’s the start of another battle. If the number seems shockingly low, your instincts are probably correct.

Don’t just accept it. The insurer’s first offer is almost always a starting point. Disputing it successfully means replacing emotion with evidence and building a solid case for your vehicle’s true car value after the accident.

Why Are Initial Offers Often Low?

It’s simple business. Insurance companies aim to close claims quickly and at the lowest possible cost. They rely on third-party valuation services like CCC ONE or Audatex, which are fast but can lack accuracy.

These platforms often use outdated sales data, dealer wholesale prices, or “comparable” vehicles that don’t truly match yours. They might miss your specific trim level, recent upgrades, or the excellent condition you maintained. This is where you find your leverage.

Building a Strong Counter-Offer with Facts

Telling an adjuster you “feel” your car is worth more is ineffective. You need a logical, fact-based argument that shows them precisely where their valuation is flawed.

Start by gathering your own proof:

- Maintenance and Repair Records: Collect every receipt for oil changes, new tires, or other work. This proves your vehicle was well-maintained, which adds value.

- Receipts for Upgrades: Did you add a premium sound system, new wheels, or a tow package? These tangible improvements increase your car’s fair market value.

- Local Market Research: Search for vehicles of the exact same year, make, model, and trim with similar mileage being sold in your area. Screenshot listings from local dealer sites and private sellers. Local data is more relevant than national averages.

Expert Tip: Try to find “sold” listings if possible, as asking prices can be inflated. However, active dealer listings are powerful evidence because they represent the actual replacement cost you now face.

The Deciding Factor: An Independent Appraisal

While your own research is a great start, the single most effective tool for negotiation is a certified, independent appraisal. This is an objective, data-driven report from an unbiased expert that establishes your vehicle’s true fair market value.

Presenting an adjuster with a total loss appraisal from a trusted source like SnapClaim changes the conversation. You are no longer arguing opinions. You are replacing their report with a professional one built on:

- Hyper-Local Market Data: Analysis of real sales figures from your specific geographic area.

- Condition Adjustments: Proper accounting for your vehicle’s excellent condition and low mileage.

- Feature and Upgrade Valuation: Assigning the correct value to every factory option and recent improvement.

A certified report forces the adjuster to justify their low number against professional valuation they cannot easily dismiss. It provides the hard evidence needed to negotiate with confidence.

With SnapClaim, the process is also risk-free. If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee—guaranteed. This lets you challenge a lowball offer without financial risk, empowering you to fight for the money you’re rightfully owed when figuring out what to do with a totaled car.

Navigating the Paperwork and Getting Paid

Once you and the insurer agree on a fair value for your car, you’re in the final stretch. However, you still need to complete the necessary paperwork to receive your settlement check.

This part of the process can be tedious, but getting it right is crucial for a smooth payout. Let’s walk through what you need to do, from signing the title to dealing with your lender.

Signing Over the Title

If you are surrendering the vehicle to the insurance company, you must officially sign the title over to them. Your adjuster will provide instructions, but it typically involves signing your name in the “seller” field on the title certificate.

Pay close attention here. State rules for transferring a car title can be specific, so sign your name exactly as it appears on the title. Do not fill out any other sections unless instructed by the adjuster, as mistakes can cause significant delays.

What Happens If You Still Have a Loan

This is a very common situation. If you still owe money on your totaled car, the insurance company will not pay you directly. The payment must first go to your lender, also known as the lienholder.

Here are the two most common scenarios:

- The settlement is more than your loan balance. The insurance payout goes to the lender, pays off the loan in full, and the lender sends you a check for the remaining amount.

- The settlement is less than your loan balance. You are responsible for the difference between the payout and what you owe. This shortfall is what GAP (Guaranteed Asset Protection) insurance is designed to cover. If you have it, it will pay that difference.

A critical piece of advice: continue making your car payments throughout this entire process. Missing payments will damage your credit score, creating another problem you don’t need.

Key Insight: The final insurance total loss payout is sent directly to the lienholder first. Understanding who gets the insurance check when a car is totaled helps set proper expectations and manage your finances.

Finalizing Your Policy and Registration

After the claim is settled, you have a few more loose ends to tie up to avoid future bills and liability issues.

First, contact your insurance agent to remove the totaled car from your policy. If it was your only vehicle, you’ll need to cancel the policy. You may even receive a prorated refund for any premium you paid in advance.

Next, contact your state’s DMV to cancel the vehicle’s registration. This officially severs your ties to the vehicle, preventing future registration bills or other issues.

If You Keep the Car with a Salvage Title

If you decide to keep the car, the process is slightly different. Once you receive the settlement check (minus the salvage value), you must apply for a salvage title at the DMV. This document officially brands the car as totaled and not road-worthy.

Before you can legally drive it again, you’ll have to:

- Complete all necessary repairs.

- Pass a rigorous state safety and anti-theft inspection.

- Apply for a “rebuilt” or “reconstructed” title.

This path requires significant effort and a deep understanding of your state’s specific laws and inspection requirements.

FAQ: What to Do With a Totaled Car

Navigating a total loss claim can be confusing. Here are answers to some of the most common questions vehicle owners ask.

Do I have to accept the insurance company’s first settlement offer?

No, you do not. The insurance company’s initial offer is a starting point for negotiations. You have the right to dispute their valuation if you believe it is too low. To do so effectively, you must provide evidence, such as comparable vehicle sales in your area or a certified independent appraisal, to support your claim for a higher car value after the accident.

What if I owe more on my loan than the total loss payout?

This situation, known as being “upside down” on your loan, is what GAP (Guaranteed Asset Protection) insurance is for. If you have GAP coverage, it will pay the difference between your insurance total loss payout and your remaining loan balance. If you don’t have GAP insurance, you will be responsible for paying the remaining balance to your lender out of pocket.

Can I keep my totaled car?

Yes, in most cases, you can choose to keep your totaled vehicle. This is called “owner retention.” The insurance company will pay you the car’s Actual Cash Value (ACV) minus its salvage value. However, the vehicle’s title will be rebranded as a “salvage title,” making it illegal to drive on public roads until it is repaired and passes a state inspection to receive a “rebuilt” title.

Should I continue making car payments after a total loss?

Yes, absolutely. You are contractually obligated to continue making your loan payments until the lender receives the final insurance payout and the loan is officially closed. Missing payments during the claim process will negatively impact your credit score, so it is crucial to stay current on your obligations.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes.

Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step. Get your free estimate today or order a certified appraisal report to strengthen your insurance claim.