When your car is declared a total loss, the most pressing question is: What was it actually worth? While a totalled car value calculator offers a quick estimate, securing a fair insurance settlement requires a deeper understanding of your vehicle’s true value.

This isn’t about what you originally paid. It’s about your car’s Actual Cash Value (ACV)—a term insurance companies use for what your vehicle was worth in the local market right before the accident. Understanding your car’s ACV is the first step toward getting the compensation you deserve.

What Was Your Car Really Worth Before the Accident?

Receiving the news that your car is a total loss is stressful enough, but the insurance company’s settlement offer can often add to the confusion. It’s important to view their first offer not as a final number, but as the starting point for a negotiation.

That initial offer is based on their internal assessment of your car’s ACV, which considers factors like its age, mileage, condition, and recent sales of similar cars in your area. The problem is that insurers often rely on automated systems that can easily overlook the unique details of your vehicle. Perhaps it had a spotless interior, recent major service, or desirable factory options. This is precisely why their first offer frequently feels too low.

The Key Factors Driving Your Car’s Value

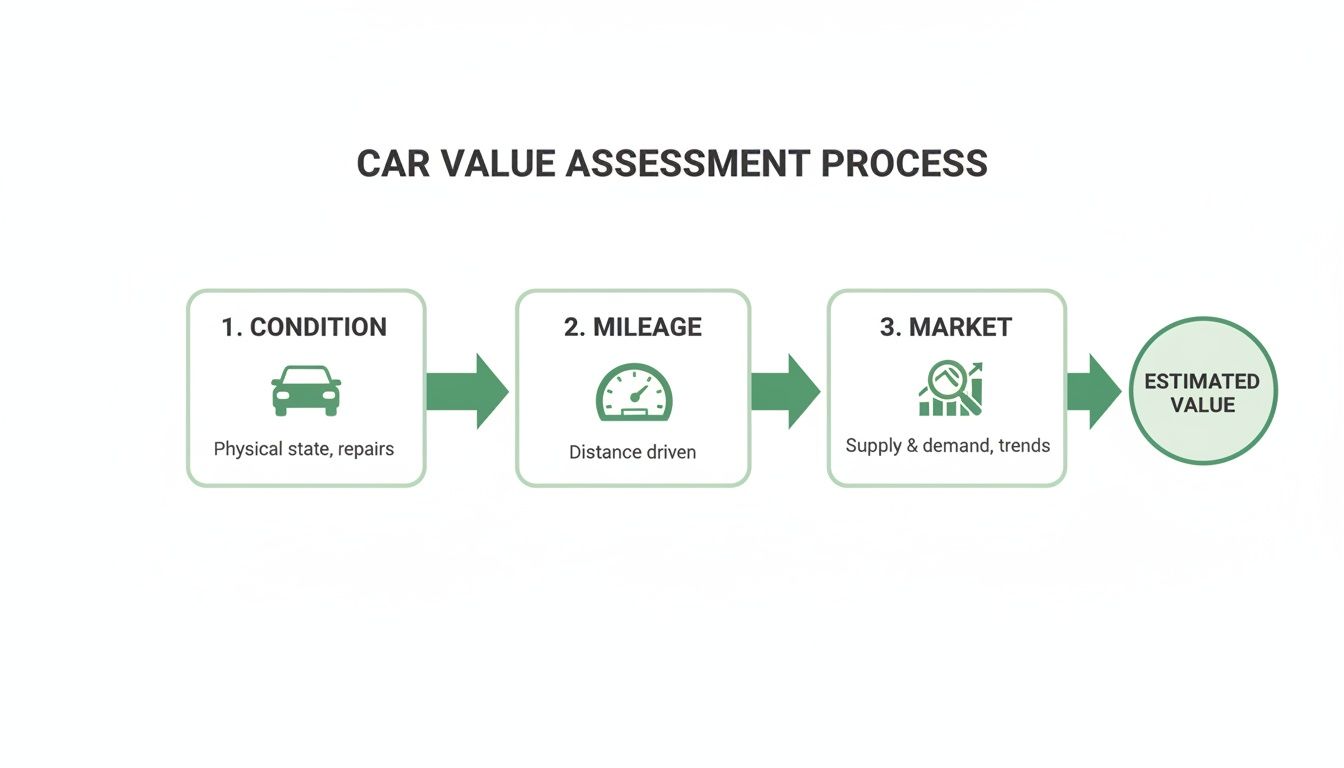

To secure a fair insurance total loss payout, you need to think like an appraiser. A car’s value isn’t just one number; it’s a combination of several key details that tell its full story.

The table below breaks down the core components that determine your vehicle’s Actual Cash Value (ACV).

Key Factors That Determine Your Car’s Total Loss Value

| Factor | Why It Matters | How to Document It |

|---|---|---|

| Pre-Accident Condition | Insurers often default to “average” unless you prove otherwise. A car in excellent condition is worth significantly more. | Photos from before the accident, detailed service records, receipts for detailing or cosmetic work. |

| Mileage | This is a huge value driver. A car with 50,000 miles is worth much more than the same model with 150,000 miles. | Odometer photos (if possible after the accident), state inspection reports, and service invoices that list the mileage. |

| Recent Upgrades | New tires, a new battery, or an upgraded audio system all add value. If you don’t mention them, the insurer won’t know. | Receipts are everything here. Keep a folder for any money you’ve put into the car. |

| Local Market Data | This is the most critical piece. National averages don’t matter. What matters is what a comparable car is selling for right now, in your city. | Screenshots of local dealer listings and private party ads for cars with similar year, make, model, trim, and mileage. |

Ultimately, putting together a strong case is about documenting these factors to build a clear, evidence-based picture of your car’s true value. This flowchart shows how these pieces come together to create a final valuation.

As you can see, a car’s final worth is a direct result of its documented condition, verified mileage, and the real-time demand for similar models in your local market.

From Online Estimate to Defensible Proof

A free online tool provides a useful starting point, but it isn’t the hard evidence needed to challenge a low insurance offer. For a deeper look into the valuation process, our complete guide explains https://www.snapclaim.com/how-much-is-my-car-worth and the methods used to prove it.

Key Takeaway: An insurance company’s valuation is an opinion, not a fact. To negotiate effectively, you must counter their opinion with your own evidence, showing the vehicle’s true condition and what it would actually cost to replace it in your local market.

To build an even stronger case, it helps to understand the broader market. Exploring general Car Valuation Resources can give you more insight into how market prices are determined. The goal is simple: build a comprehensive picture of your car’s value based on tangible proof. This moves you from being a passive recipient of an offer to an active, informed negotiator ready to get a fair settlement.

Decoding the Insurer’s Valuation Report

Once the insurance company declares your car a total loss, you’ll receive a valuation report. This document is their official breakdown of what they believe your car was worth just before the crash. However, this report isn’t the final word—it’s their opening offer in a negotiation.

Insurance carriers don’t just pull a number out of thin air. They typically rely on third-party data providers like CCC ONE or Mitchell to generate these reports. While these platforms are sophisticated, they are still automated systems that rely on generalized market data. They often miss the unique details and qualities that made your car special, which almost always leads to a lower settlement offer. The key to getting what you’re owed is understanding how they built their number so you can find the flaws.

Common Flaws in an Insurer’s Calculation

An insurer’s valuation report is essentially a formula. It starts with a “base value” and then applies adjustments to arrive at a final number. It’s in those adjustments where your settlement can be won or lost.

A classic example is the condition adjustment. Unless you provide solid proof of your car’s pristine condition—like recent service records or pre-accident photos—the system will likely default its condition to “average.” That single setting can shave hundreds, or even thousands, of dollars off your car’s value.

Then there are the comparable vehicles, or “comps.” The system scours recent sales of similar cars in your area to justify its valuation. But are those comps really comparable? We’ve seen reports use cars with much higher mileage, fewer options, or worse condition than the vehicle they were supposed to match. A proper totalled car value calculator must focus on true, like-for-like comparisons, not just what an algorithm suggests.

The Importance of Trim Packages and Regional Differences

Did your car have a premium sound system, a panoramic sunroof, or a specific sport package you paid extra for? These features can dramatically increase a vehicle’s value, but they are often missed in a standard valuation report.

If those options aren’t listed on the report, it’s a massive red flag. They likely were not factored into the final number. For instance, a top-tier trim level can easily be worth $3,000 to $5,000 more than the base model. You can get a much clearer picture of how these reports work by reviewing a detailed guide on the CCC ONE report, one of the most common tools insurers use.

Pro Tip: The first thing you should do is double-check the VIN on the report. A single incorrect digit can cause the system to pull data for a completely different model or trim, leading to a wildly inaccurate valuation.

Understanding the Total Loss Threshold

The decision to “total” a car is based on the total loss threshold. This is the point where repair costs reach a certain percentage of the car’s value, making it more economical for the insurer to pay you out than to fix it. This threshold varies by state. Some states set it at 75% of the car’s value, while others may go up to 100%.

- Fixed Percentage States: Most states have a set Total Loss Formula (TLF) defined by law.

- Insurer Discretion States: In other states, it’s up to the insurance company. They’ll usually total a vehicle when repair costs plus its salvage value exceed its pre-accident ACV.

Knowing the law in your state is crucial. It helps you understand the insurer’s decision and gives you a firm foundation if you believe their valuation is too low. A lower ACV makes it much easier for repair costs to hit that total loss threshold, pushing a potentially repairable car over the edge. By digging into these details, you can start building a solid, evidence-backed case for the fair compensation you rightfully deserve.

How to Build Your Case for a Higher Payout

Remember, the insurer’s first offer is just an opening bid. You have the right to challenge it, but to negotiate successfully, you must counter their valuation with solid proof. This is where you shift from accepting their number to actively proving what your car was really worth.

Start With Your Paperwork

First, gather every document that proves your car’s value and the care you put into it. Adjusters operate on facts and figures, so a detailed paper trail is your most powerful tool.

Pull together the following:

- Maintenance Records: Every oil change, tire rotation, and service receipt helps prove your car was in better-than-average condition.

- Receipts for Recent Work: Did you get new tires six months ago? Replace the battery last year? Without receipts, those upgrades don’t exist in the insurance company’s calculation.

- Pre-Accident Photos: If you have photos of your clean, well-maintained car before the crash, they serve as instant visual proof of its superior condition.

Find Your Own Comparable Vehicles (This Is Crucial)

This is the most important step in building your case. The insurance company used “comps”—comparable vehicles for sale—to justify their offer. Now, you need to do the same.

Your goal is to find real cars for sale in your local area that show what it would actually cost to replace your vehicle today. A strong comp should match your car as closely as possible in these key areas:

- Year, Make, and Model

- Trim Level and Options (e.g., a loaded Touring model vs. a base Sport model)

- Mileage (look for listings within 10-15% of your car’s mileage)

- Condition (seek ads describing the car as “excellent” or “very good”)

Expert Tip: Don’t just look in one place. Scour local dealership sites, online marketplaces like Autotrader and Cars.com, and private seller listings. Screenshot at least three to five strong comps that support a higher value for your car.

A great resource to get started is Kelley Blue Book (KBB). You can plug in your car’s details to see a value range, which helps you know what to look for when hunting for comps.

Present Your Case Professionally

Once you have your maintenance records, receipts, and a solid list of local comps, it’s time to put it all together.

Draft a polite but firm email to the adjuster and attach all your evidence. Clearly state that you believe their valuation missed key factors contributing to your car’s value. Then, lay out your points one by one, referencing your proof. This organized, evidence-based approach shows you’re serious and makes it easier for the adjuster to justify a higher payout.

Why More Cars Are Being Totaled Today

If it seems like more cars are being “totaled” after accidents, you’re not imagining it. A major shift is happening in the auto insurance industry, making it far more common for insurers to write off a vehicle rather than repair it.

It all comes down to the incredible complexity of modern cars. A minor fender-bender is no longer a simple fix. Vehicles today are loaded with advanced driver-assistance systems (ADAS), cameras, and sensors tucked into bumpers, grilles, and side mirrors. What used to be a simple bumper replacement can now become a five-figure repair bill once you factor in replacing and recalibrating all that sensitive technology.

The New Math of Vehicle Repairs

For an insurance company, it’s a simple cost-benefit analysis. They weigh the repair estimate against your car’s Actual Cash Value (ACV). Once the repair cost hits a certain percentage of that ACV, often around 75%, the car is declared a total loss.

With repair costs soaring, it doesn’t take much damage to reach that tipping point. A few key factors are driving this trend:

- High-Tech Parts: A single LED headlight assembly on a newer car can easily cost over $3,000.

- Specialized Labor: Cars built with aluminum or carbon fiber require specially trained technicians, driving up labor costs.

- Parts Shortages: Lingering supply chain disruptions inflate prices and add rental car costs while you wait for parts.

The Numbers Don’t Lie

This isn’t just a feeling; the data proves it. The industry has seen a massive jump in total loss frequency. The total loss rate for vehicles under seven years old has exploded to 32% in recent years, up from just 6-7% not long ago. You can see more on this trend by reading the full research on global auto insurance dynamics.

This new reality makes getting a fair valuation for your car more important than ever. If your insurer starts with a lowball ACV, it makes it much easier for them to declare your car a total loss—even for damage that seems repairable.

Key Takeaway: The line between “repairable” and “totalled” is blurring. Because of high-tech components and rising labor costs, insurers are quicker to total a vehicle. This makes an accurate, independent valuation your best defense against an unfair settlement.

Understanding this trend shows why you can’t just accept the insurance company’s first number. Having your own evidence and using an accurate totalled car value calculator backed by an expert appraisal is the only way to ensure you get the money needed to replace the car you lost.

Using a Certified Appraisal to Maximize Your Settlement

So you’ve done your homework, and the numbers are clear: your car is worth thousands more than the insurance company is offering. At this point, you’ve likely hit a negotiation roadblock, and a simple online totalled car value calculator is no longer enough.

To break the stalemate, you need a tool that adjusters are trained to respect: a certified, independent appraisal.

Unlike a generic estimate from an algorithm, a certified report is a detailed, defensible analysis of your specific vehicle’s value. It provides the hard proof you need to effectively challenge a lowball offer and force a fair negotiation based on facts, not just opinions.

The Power of an Independent Report

Insurance companies use their own internal systems, which are often designed to favor their financial interests. An independent appraisal levels the playing field by introducing a valuation from a neutral, third-party expert. Think of it as your official counter-offer, backed by the same kind of data and methodologies the insurance industry itself relies on.

This is more critical than ever. In 2025, the total loss frequency for vehicles rocketed to a record high of 22.2% globally. As modern cars become more expensive to repair, insurers are quicker to total them, making an accurate valuation absolutely essential. You can explore the data on rising total loss frequency to see just how much the industry is shifting.

Why Insurers Respect USPAP-Compliant Appraisals

A professional appraisal is an expert valuation that follows strict industry standards. The most credible reports adhere to the Uniform Standards of Professional Appraisal Practice (USPAP), the gold standard for professional appraisals across North America.

A USPAP-compliant report proves the valuation was:

- Objective and Impartial: The appraiser has no stake in the outcome, providing a fair and unbiased assessment.

- Thoroughly Researched: The report digs deep into local market data, your vehicle’s specific condition, all its options, and recent maintenance.

- Professionally Documented: Every finding is supported by clear evidence, building a logical case for your car’s true worth.

When you submit this type of report, the entire conversation with the adjuster changes. It shifts the negotiation away from opinions and puts the focus squarely on verifiable data, making it very difficult for them to justify their lower number. If you’re ready to take this step, our guide on a total loss car appraisal explains the process from start to finish.

Key Insight: A certified appraisal isn’t just a second opinion. It’s about presenting your claim with the same level of professional documentation the insurance company uses, which helps strengthen your claim.

Pursue Fair Compensation Without Financial Risk

We understand that paying for an appraisal while dealing with the financial stress of a total loss can feel like a big step. That’s why SnapClaim offers a powerful safety net to give you complete confidence.

Our Money-Back Guarantee is straightforward: If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee. This guarantee ensures you can challenge the insurance company’s offer without worrying about the cost. It’s our commitment to helping you secure the fair settlement you rightfully deserve.

Frequently Asked Questions About Total Loss Claims

When your car is declared a total loss, it’s normal to have a lot of questions. Here are clear, simple answers to some of the most common concerns we hear from vehicle owners.

Can I keep my totaled car?

Yes, in most cases, you can. This is called “owner retention.” If you choose this option, the insurance company will pay you the car’s actual cash value (ACV) minus its salvage value. However, your vehicle will be issued a salvage title, which can make it difficult to insure and significantly reduces its future resale value. Be sure to check your state-specific laws, as re-titling a salvage vehicle can be a complex process.

What if I owe more on my loan than the car is worth?

This stressful situation is known as being “upside down” on your auto loan. When your car is totaled, the insurance settlement is paid directly to your lender. If the settlement amount doesn’t cover your full loan balance, you are responsible for paying the remaining difference. This is where GAP (Guaranteed Asset Protection) insurance helps. If you have GAP coverage, it pays the “gap” between the insurance payout and what you still owe.

How long does a total loss settlement take?

The timeline varies. A simple claim might be resolved in a few days, but more complex cases can take several weeks. The biggest factor that causes delays is the negotiation over the vehicle’s value. If you have to go back and forth with the adjuster, the process will take longer. Presenting a certified appraisal report from the start can help shorten this timeline and lead to a faster, fairer resolution.

Does my insurance total loss payout include taxes and fees?

This is an excellent question. In many states, the answer is yes. Insurance companies are often required to include sales tax, title transfer fees, and registration costs in the final payout. The goal of the settlement is to “make you whole,” meaning it should be enough to purchase a comparable replacement vehicle, including the associated fees. Always review your settlement breakdown, and if these costs are missing, you have the right to ask that they be included.

Challenging an insurance company’s low offer can feel overwhelming, but you don’t have to do it alone. A totalled car value calculator is a good start, but a certified appraisal from SnapClaim provides the data-backed proof you need to negotiate fairly and confidently.

Get your free estimate today or order a certified appraisal report to strengthen your insurance claim.

👉 Get your free total loss car value estimate today

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes.

Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step.

Generate a free diminished value or total loss estimate in minutes and see how much compensation you may be owed.

👉 Get your free fair market value estimate of your total loss vehicle today