Has your car been in an accident? Even after perfect repairs, its value has likely dropped simply because it now has an accident history. A Progressive diminished value claim is your tool to recover that lost money from the at-fault driver’s insurance, but navigating the process can feel overwhelming.

This guide breaks down exactly how to build a strong claim, negotiate effectively, and get the fair compensation you deserve. We’ll show you how to counter their lowball offers with solid proof.

Understanding Progressive’s Approach to Diminished Value

When you file for diminished value, you aren’t questioning the quality of the bodywork. You’re pointing out a simple market reality: given two identical cars, a buyer will always pay less for the one with an accident history. This drop in your car’s fair market value is a real financial loss, and you have the right to recover it.

Progressive acknowledges this loss exists, but their goal is to settle your claim for the lowest amount possible. They often use a generic formula that doesn’t account for your vehicle’s actual loss in value. To learn more about the fundamentals, read our full guide on what a diminished value claim is.

The Problem with Their Formula

Progressive adjusters often rely on a variation of the “17(c) formula” to calculate their initial offer. This method typically caps the potential loss at 10% of the car’s pre-accident value and then reduces that number further using “modifiers” for mileage and damage severity.

For example, a 2023 case involved a vehicle worth $32,000 before the crash. Progressive’s formula-based offer was only $4,000, despite significant repairs. This cookie-cutter approach is a disadvantage for vehicle owners because it ignores the real factors that determine a car’s value.

Here is what their formulas often miss:

- Vehicle Desirability: A popular truck, luxury SUV, or sports car loses a much larger percentage of its value than a standard sedan after an accident.

- Local Market Conditions: A generic national formula can’t capture what buyers in your specific city are willing to pay for a vehicle with an accident history.

- The Stigma of Structural Damage: If your car had frame or unibody damage, the negative stigma is huge, even if repairs meet factory specifications. The formula rarely accounts for this properly.

To see how different states handle these claims, you can review this helpful 50-state diminished value survey.

Are You Eligible to File a Claim?

Before investing time in building your claim, you need to confirm you are eligible to file for Progressive diminished value. The rules can change significantly depending on where you live and who was at fault.

The most important requirement is that the other driver must be at fault. Since they are insured by Progressive, you are filing what’s known as a “third-party claim.” You are the third party seeking compensation from their insurance policy to cover the loss they caused.

Third-Party vs. First-Party Claims

Understanding this distinction is critical because it determines your rights.

- Third-Party Claim: This is you filing a claim against the at-fault driver’s Progressive policy. In most states, the law gives you the right to recover the drop in your car’s market value caused by their insured driver’s negligence.

- First-Party Claim: This would involve filing with your own insurance company. Unfortunately, this is almost always a dead end. Standard auto policies typically exclude diminished value from collision coverage. Your policy is designed to pay for repairs, not the hit to your car’s resale value.

So, if a driver insured by Progressive hit you and was at fault, you are eligible to file a third-party claim.

How State Laws Affect Your Claim

Where the accident occurred is just as important as who was at fault. Diminished value is governed by state law, creating a patchwork of different rules across the country. A claim that is straightforward in one state might be an uphill battle in another.

For example, Georgia has strong legal precedents that support a vehicle owner’s right to be compensated for diminished value by the at-fault party. On the other hand, a state like Michigan has a “mini-tort” system that caps recovery for all vehicle damage at just $3,000, making it difficult to pursue a meaningful claim for a high-value car.

You must know the rules for your specific location. Our state-by-state diminished value law guide can help you confirm if you are on solid ground before you begin.

How to Assemble Proof for Your Progressive Diminished Value Claim

To win your Progressive diminished value claim, you can’t just state your car lost value—you must prove it. Insurance adjusters are trained to challenge weak arguments, so your best defense is a collection of solid, organized evidence.

A well-documented claim shows you are serious and makes it much harder for Progressive to dismiss you with a lowball offer. Your goal is to create a clear picture of your vehicle’s pre-accident condition, the extent of the damage, and the details of the repairs.

Your Essential Evidence Checklist

Gathering the right paperwork is the foundation of a strong claim. Each document helps tell the story, from establishing fault to detailing every part that was replaced.

Here’s what you need to collect:

- The Official Police or Accident Report: This is the official record that establishes the facts of the accident and, most importantly, identifies the at-fault driver.

- The Finalized Repair Invoice: You need the final, itemized bill from the body shop—not an initial estimate. It details every part, labor hour, and procedure performed.

- Pre- and Post-Repair Photographs: Visuals are powerful. Take clear photos of the damage before repairs begin. Afterward, take another set from the same angles to create a compelling before-and-after comparison.

This documentation proves the “what” and “how” of the incident, setting the stage for you to demonstrate the financial loss.

Why the Repair Invoice Is So Important

Your final repair invoice is more than a receipt; it’s a technical map of your car’s journey through the body shop. A Progressive adjuster will analyze this document to determine the collision’s severity.

Look for these key terms on your invoice, as they indicate significant diminished value:

- Structural or Frame Damage: Any mention of a “frame machine,” “unibody alignment,” or the replacement of core structural parts is a major red flag for future buyers and a key point in your claim.

- OEM vs. Aftermarket Parts: The invoice specifies if Original Equipment Manufacturer (OEM) parts were used. The use of cheaper aftermarket parts can contribute to your loss in value.

- Blended Paint Panels: This subtle detail indicates the new paint had to be “blended” into adjacent panels to match the color, signaling a larger and more obvious repair area.

Properly collecting critical evidence to preserve after a car accident is the first step. Having this proof ready puts you in a much stronger negotiating position.

Proving Your Car’s Actual Lost Value with an Appraisal

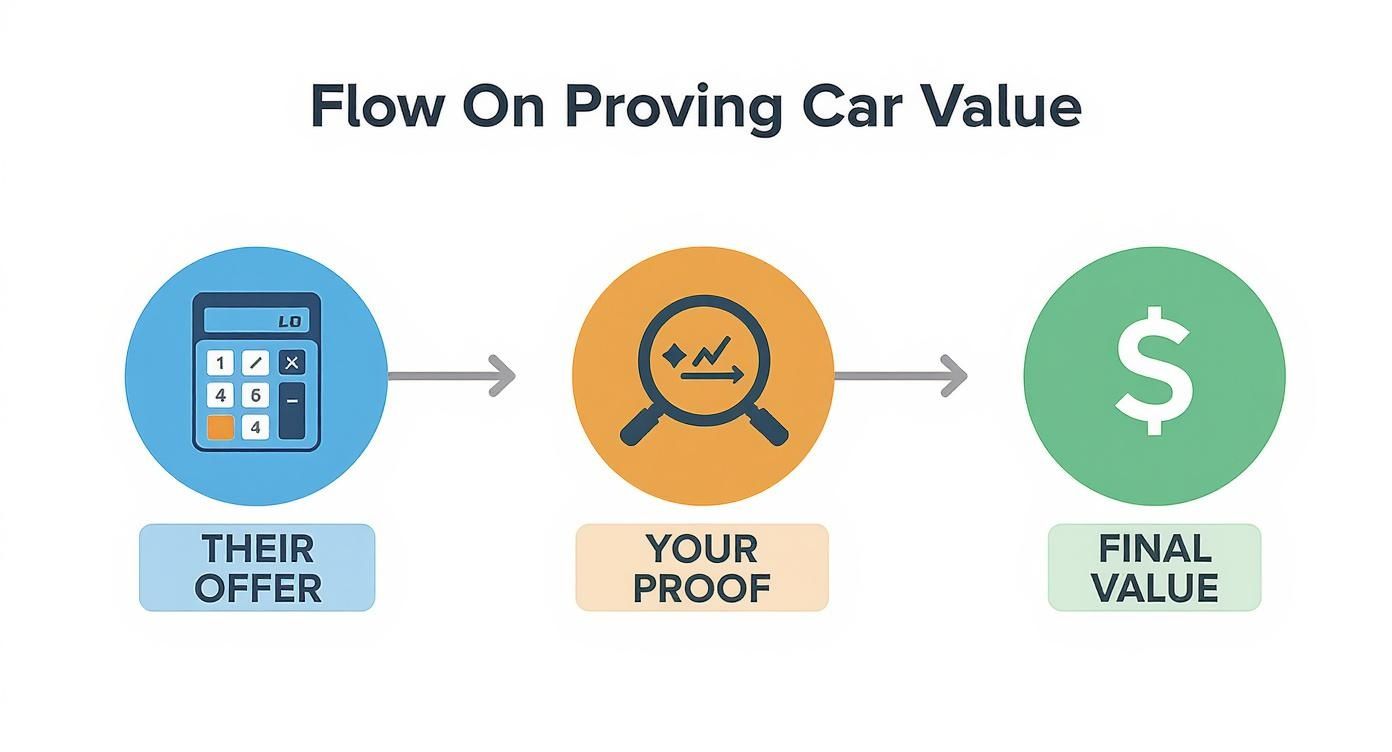

This is the most critical part of your Progressive diminished value claim: proving the exact dollar amount your car has lost. After you submit your claim, the adjuster will provide an offer. Be prepared for it to be low.

That initial offer is based on Progressive’s internal formula, which is designed to produce the smallest possible payout. You are under no obligation to accept it. The key is to counter their formula with data-driven proof of your vehicle’s true loss in market value.

Why Their Offer Is Just a Starting Point

Progressive’s adjusters may try to control the negotiation by presenting their low number as a “standard industry practice” or the “maximum allowed.” These are common tactics, not facts.

Their calculations often ignore the factors that truly determine a car’s worth:

- Make and Model Reputation: A luxury brand or popular truck takes a bigger value hit after an accident than a basic commuter car.

- Accident Severity Stigma: A record of “structural” or “frame” damage on a vehicle history report is toxic to its resale value.

- Local Market Dynamics: Your car’s value depends on what buyers in your city are willing to pay. A generic, national formula cannot capture these local nuances.

Your job is to shift the conversation away from their internal math and toward real-world market evidence.

The Power of an Independent Appraisal

An independent, certified appraisal is your most effective tool. It is a professional report that analyzes objective market data to pinpoint your exact financial loss. A comprehensive appraisal, like those provided by SnapClaim, acts as an expert witness by comparing your repaired vehicle to identical ones on the market with clean histories.

An independent appraisal is your official rebuttal to Progressive’s lowball offer. It provides the third-party validation needed to show your demand is based on real market data, not just your opinion.

How to Respond to Common Adjuster Arguments

With your appraisal in hand, you’ll be ready for the negotiation. Here’s how you can confidently counter common objections:

| What the Adjuster Might Say | How to Respond (Using Your Appraisal) |

|---|---|

| “Our 17c formula is the industry standard.” | “That formula is an internal tool and doesn’t reflect my vehicle’s specific market. This appraisal analyzes real-time sales data, which is a more accurate measure of my loss.” |

| “The car was repaired to pre-accident condition, so there’s no loss.” | “While the repairs are excellent, the vehicle now has a permanent accident history. This report proves its market value has dropped, which is a separate and recoverable loss.” |

| “We can’t rely on a report you paid for.” | “This is a USPAP-compliant report from a certified appraiser based on objective market data. I expect you to consider the expert evidence it presents.” |

| “You haven’t sold the car, so you haven’t realized a loss.” | “The loss occurred at the moment of the accident. Diminished value is the immediate drop in fair market value, regardless of when I plan to sell.” |

A certified car appraisal after an accident provides the language and data to stand your ground. It transforms you into an informed negotiator with a fact-based argument.

Submitting Your Demand and Negotiating a Fair Settlement

Once you’ve gathered your evidence and have a certified appraisal, it’s time to formally pursue your Progressive diminished value claim. The goal is to present a professional case built on solid proof.

Your first step is to send Progressive a formal demand letter. This is a straightforward letter that outlines the facts, states your demand, and attaches all your supporting evidence.

Crafting a Professional Demand Letter

Your demand letter should guide the adjuster to the same conclusion you’ve reached: your vehicle has lost a specific, provable amount of value.

Here is a simple structure to follow:

- Introduction: State your name, claim number, and the date of the accident. Clearly state that you are requesting compensation for the inherent diminished value of your vehicle.

- Summary: Briefly recap the accident, confirming their insured driver was at fault.

- The Demand: State the exact dollar amount of diminished value you are claiming, taken directly from your independent appraisal report.

- The Evidence: List every document you are including: the police report, final repair bill, photos, and your certified appraisal report.

- Call to Action: Politely ask them to review the documents and let them know you look forward to their response to settle the claim.

Preparing for the Negotiation

After sending your demand, an adjuster will contact you. Expect a low counteroffer based on their internal formula. Stay calm, be firm, and keep the conversation focused on your evidence. Before the call, it helps to review expert tips for communicating with auto adjusters.

Remember, their first offer is just a starting point. Your SnapClaim appraisal is your anchor. Each time they try to pull the conversation back to their numbers, politely redirect it to the real-world market data in your report.

The secret to a successful negotiation is persistence, not aggression. Treat it like a business transaction. Use phrases like, “I understand your position, but the market data in my appraisal shows a different figure,” or “Can you point to specific errors in my appraisal report that justify your lower offer?”

This tactic forces them to engage with your evidence instead of repeating their script. If negotiations stall, you still have options, like asking to speak with a supervisor or filing a complaint with your state’s Department of Insurance. In some cases, you may need to invoke the appraisal clause in the at-fault driver’s policy to force an independent resolution.

Frequently Asked Questions (FAQ)

Can I file a diminished value claim if I caused the accident?

Almost always, the answer is no. A diminished value claim is a third-party claim made against the at-fault driver’s insurance—in this case, Progressive. Your own collision coverage pays for physical repairs to your vehicle but does not cover its drop in market value.

How long do I have to file my claim?

Every state has a deadline, known as the statute of limitations, for filing property damage claims. This window is typically two to three years from the date of the accident. It is crucial to start your claim as soon as repairs are complete. Check our guide on state-specific diminished value laws for your state’s exact deadline.

Will filing a diminished value claim make my own insurance rates go up?

No. Filing a third-party claim against the at-fault driver’s Progressive policy will not affect your own insurance rates or driving record. Your insurance company is not involved in the payout and has no right to raise your premiums.

Can I file a claim if my car is leased or financed?

Yes, and you absolutely should. An accident on your car’s record lowers its trade-in or resale value, which can leave you owing more on your loan than the car is worth. For a leased vehicle, this loss in value can result in “excessive wear and tear” charges at the end of your term. The money from a successful Progressive diminished value claim helps offset these financial risks.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes. Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step. Our certified reports provide the proof you need to negotiate fairly.

And remember our Money-Back Guarantee: If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee — guaranteed.