Diminished Value Appraisal in

Florida

Get fast, accurate, and court-ready Diminished Value and Fair Market Value reports.

No guesswork, No delays. Trusted by insurers and legal professionals.

No credit card required.

Recover What Insurance Owes You After an Accident

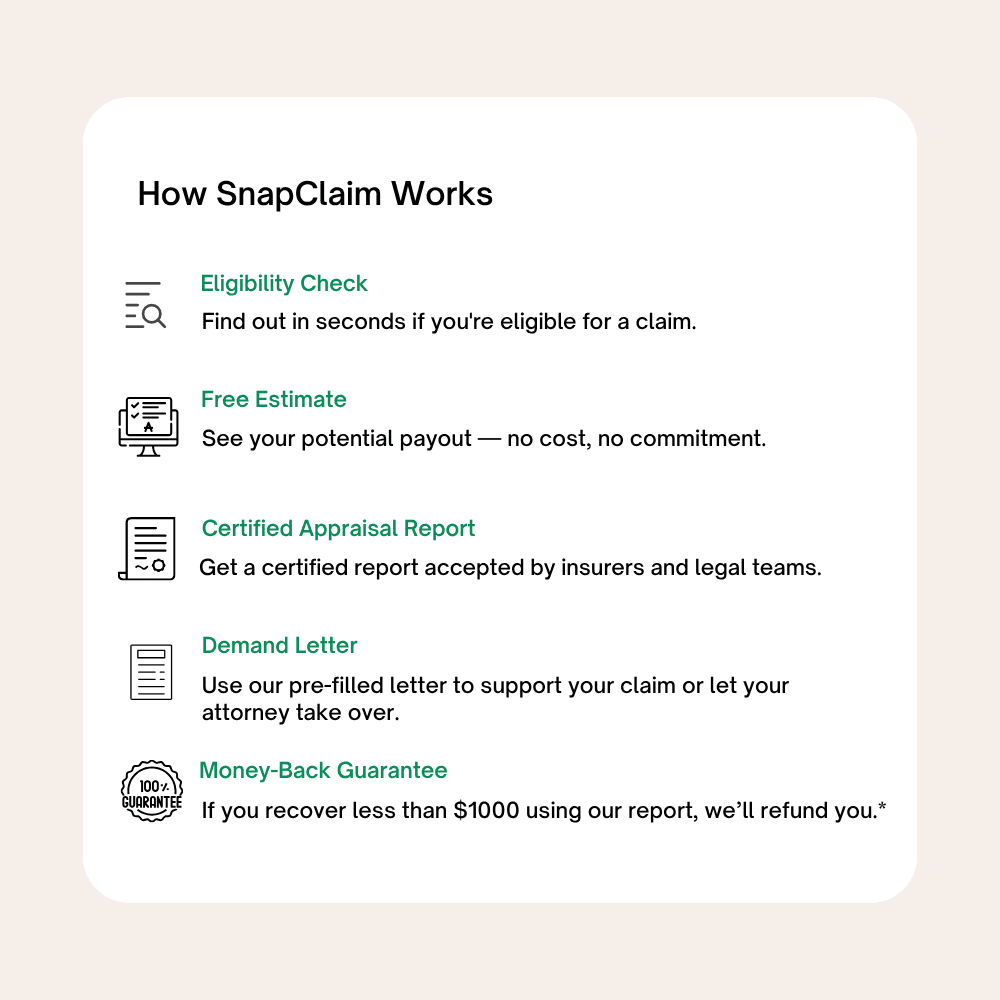

SnapClaim makes it easy to recover your car’s lost value after an accident. We provide a free estimate, a fully certified appraisal report, and a ready-to-send demand letter — all within minutes. No guesswork, no waiting.

“I had no idea my car had lost that much value after the crash. SnapClaim gave me everything I needed to file the diminished value claim — I got the report in less than an hour.”

Mark

Vehicle Owner, Colorado

Filing A Diminished Value Claim In Florida

If you were involved in a car accident in the state of Florida and weren’t at-fault, you could be eligible for a diminished value claim settlement. Due to favorable case law concerning the right to recover diminished value in Florida such as McHale v. Farm Bureau Mutual Insurance Co. 409 So.2d 238 (1982) and Siegle vs. Progressive Consumer’s Insurance Company819 So.2d 732 (Florida 2002), Florida happens to be one of the best states in the country for getting compensated for your vehicle’s loss in value due to a car accident if you weren’t at fault.

Florida diminished value law

Florida allows drivers to file a diminished value claim if they were not at fault in the accident. The statute of limitations for such claims is four years from the date of loss. These claims are filed with the at-fault driver’s insurance company.

Florida law mandates that when an insurer chooses to repair a vehicle, it must restore the vehicle to substantially the same appearance, function, and value.

Florida Standard Jury Instructions – Property Damage

The standard jury instructions provide that the measure of damage to personal property (such as an automobile) includes:

· The difference between the value of the vehicle immediately before and after the incident.

· The reasonable cost of repair, with due allowance for any difference in value before and after repair.

· Towing or storage charges, and compensation for the loss of use of the vehicle during the period reasonably required for repair or replacement.

Florida Department of Insurance Bulletin 84-270

This bulletin supports the right to claim diminished value. It states:

“The responsibility of the insurance company for automobile accident damages is the substantial restoration of the automobile as to function, appearance, and value. The owner has not been properly indemnified unless there is no diminution in value of the automobile as it was before the damage and as it is after repairs.”

Florida is a diminished value state, and vehicle owners are entitled to compensation for any loss in market value resulting from an accident.

How to file a diminished value claim in Florida

Step 1. Get a free estimate. Start by checking if your vehicle qualifies for a diminished value claim. SnapClaim provides a fast, no-cost estimate to help you understand your potential recovery.

Step 2. Order your certified appraisal report. If eligible, SnapClaim will generate a professional, independent diminished value appraisal—often in minutes. This report is formatted for insurance use and backed by industry data.

Step 3. Submit your claim. Along with your appraisal, SnapClaim provides a pre-filled demand letter to send to the at-fault driver’s insurance company. This makes it easy to start the claims process without a lawyer.

Step 4. Settle your claim. Most insurers will respond with a settlement offer. You can choose to accept, negotiate, or escalate the claim. If needed, SnapClaim can help you provide documentation to support further action.

SnapClaim is designed to help you recover fair compensation with less stress, faster turnaround, and no upfront legal fees.

Money-back guarantee: If your final insurance recovery is under $1,000, SnapClaim will refund 100% of your appraisal fee. We only succeed when you do.

Florida diminished value law

Statute of Limitations: 4 years

Third Party Diminished Value Claim: Yes

First Party Diminished Value Claim: No

Most insurance policies will exclude diminished value.

Florida Property Damage Minimum Limits: $10,000 in coverage

Uninsured Motorist Coverage for Diminished Value: No coverage

Underinsured Motorist Coverage for Diminished Value: No coverage

Florida Small Claims Court Limit: $8,000

attorney representation and appeals are permitted

How to File a Diminished Value Claim in Florida

Last updated: August 13, 2025

If your vehicle was damaged in a Florida crash and repaired, it may still be worth less than before. That lost market value is called diminished value (DV). This comprehensive guide explains when DV is recoverable in Florida, the evidence you need, the exact steps to file, critical deadlines (including the 2023 statute-of-limitations change), and how a professional appraisal from SnapClaim strengthens your case.

Does Florida Allow Diminished Value Claims?

Third-party DV (against the at-fault driver’s insurer): Yes. Florida recognizes recovery of diminution in value as a component of property damage in tort claims. The Florida Department of Financial Services explains that while Florida law is “silent” on a formula, DV may be covered in third-party property damage claims and the claimant must prove the loss. See the DFS consumer guidance under “Personal Automobile Insurance Overview.”

First-party DV (under your own policy): Generally not covered unless your policy explicitly provides it. In Siegle v. Progressive (Fla. 2002), the Florida Supreme Court held that when an insurer repairs or replaces with like kind and quality as the policy promises, it is not obligated to pay for inherent diminished value (unless the contract says otherwise). This is why first-party DV is usually denied.

New to DV? Start with our Diminished Value Overview.

Key Florida Law & Authority

- First-party diminished value: Siegle v. Progressive Consumers Ins. Co., 819 So. 2d 732 (Fla. 2002) — no inherent DV payment required if the policy provides for repair/replace to like kind and quality and the carrier fulfills that promise.

- Third-party diminished value: Florida DFS (CFO) consumer guidance notes DV can be a covered loss in third-party property damage claims; the claimant bears the burden of proof.

- Statute of limitations (SOL): For negligence actions accruing on or after March 24, 2023, Florida reduced the negligence SOL to 2 years (HB 837 amending §95.11). For claims that accrued before March 24, 2023, the prior 4-year period generally applies. Always confirm which deadline governs your case.

- Small Claims & County Civil: Small Claims up to $8,000 are in County Court; County Civil jurisdiction extends up to $50,000 (useful if you litigate a DV dispute).

For a 1-page summary of DV concepts nationwide, see the NAIC Journal overview (linked in References).

Types of Diminished Value Recognized

- Immediate DV: Reduction in value immediately after the crash and before repairs (rarely pursued by consumers).

- Repair-related DV: Loss caused by sub-optimal repairs (non-OEM parts, structural/frame issues, paint mismatch, poor refinish quality).

- Inherent (residual) DV: Loss that remains even after high-quality repairs because the vehicle now has an accident history (the stigma effect in the resale market).

What Documentation You Need

- Crash report: Florida Highway Safety and Motor Vehicles (FLHSMV) crash report from the Crash Report Purchasing Portal (available online; agencies have up to 10 days to submit).

- Photos: Pre-loss (if available), post-crash damage, and post-repair.

- Repair records: Full estimates, final invoices, parts list (OEM vs. aftermarket), frame/unibody measurements, paint materials sheets.

- Vehicle info & condition: VIN, trim/options, mileage before/after, service history, ownership/title (no salvage branding), and market comps.

- Professional appraisal: An independent DV report quantifying inherent/repair-related loss using transparent methodology and local market comps — order a SnapClaim DV appraisal.

If the vehicle is a total loss, you’ll want a Fair Market Value (Total Loss) Appraisal instead.

Step-by-Step: Filing a Diminished Value Claim in Florida

- Confirm liability & coverage. DV is typically pursued as a third-party property damage claim against the at-fault driver’s liability insurer.

- Gather your evidence. Crash report, photos (damage and post-repair), complete repair documentation, service/ownership records.

- Get a professional DV appraisal. Use SnapClaim to obtain a fast, credible, court-ready valuation grounded in Florida market data.

- Send a formal demand. Write a concise demand letter to the insurer. Attach the appraisal and exhibits (photos, estimates/invoices, comparable listings/auction data). State the precise DV amount and valuation basis.

- Negotiate with data. Be prepared to address mileage/condition adjustments, repair-quality issues, and comparables. If the carrier uses heuristic formulas (e.g., “17c”), counter with your documented market evidence.

- Escalate if needed. If adjusters stall or undervalue the claim:

- Insurance complaint: Contact Florida DFS Consumer Services (helpline and online portal) for assistance and to log issues with the insurer.

- Small Claims / County Civil: Consider filing suit — Small Claims (≤ $8,000) or County Civil (≤ $50,000). Check your county clerk for forms and filing instructions.

- Counsel: Consult a Florida attorney experienced in auto property damage/DV if the dispute persists.

- Know your deadlines. For negligence claims that accrued on or after March 24, 2023, you generally have 2 years to file suit. Claims that accrued before that date usually retain the older 4-year period. Contract-based claims may differ (read your policy).

Florida-Specific Tips to Strengthen Your File

- Use Florida-based comps. Include local dealer and private-party listings and recent auction data that reflect buyer discounting for accident history in your metro.

- Document repair quality. Frame specs, paint meter readings (if available), and body shop certifications help establish (or negate) repair-related DV.

- Be precise in your theory. Your demand should clearly state you seek the difference between pre-loss and post-repair fair market value (diminution in value) and identify whether the loss is inherent and/or repair-related.

- Track deadlines & communications. Diary your SOL, keep email chains, and maintain a clean exhibit stack (A, B, C…) for quick submission.

Why Using a Professional Appraisal Is Crucial

Insurers scrutinize DV submissions and often rely on rough formulas that understate real-world market impact. A SnapClaim appraisal applies market-verified comparables, transparent adjustments, and expert review — built to stand up in negotiation, Small Claims, or County Civil. Our Money-Back Guarantee Policy helps you pursue your claim with confidence.

- Order a Diminished Value Report

- Diminished Value Overview

- Fair Market Value (Total Loss) Appraisal

- Money-Back Guarantee Policy

- Diminished Value State Laws

References & Resources

- Florida DFS (CFO) — Personal Automobile Insurance Overview (DV guidance): Consumer Insurance Overview

- Florida Supreme Court — Siegle v. Progressive Consumers Ins. Co., 819 So. 2d 732 (Fla. 2002): Opinion (FindLaw) | Court filings

- Florida Statute of Limitations (negligence) — §95.11 as amended by HB 837 (effective Mar. 24, 2023): HB 837 Bill Page | §95.11 Current Text

- Crash Reports — Florida Highway Safety & Motor Vehicles: Traffic Crash Reports | Crash Report Purchasing Portal

- Small Claims Info (≤ $8,000) — Florida Courts Help: Small Claims Guide; County Civil jurisdiction up to $50,000 — Florida Courts: Know Your Court

- Background reading — NAIC Journal, “Automobile Diminished Value Claims” (2023): PDF

- SnapClaim internal resources:

See what ourclientsare sharing about us!

“I didn’t know about diminished value until I found SnapClaim. Their report was done in minutes, and the support team explained everything clearly. I used the letter they provided and ended up with an extra $3,200. Super easy.”

“SnapClaim helped me file a diminished value claim after repairs. The process was smooth, fast, and I received more money than expected. Their team handled everything so I could focus on getting my car and life back to normal.”

“I uploaded my repair estimate and got a professional report the same day. SnapClaim made everything so simple. Their platform saved me hours of back-and-forth with insurance and got me a solid payout”

“After my car was totaled, SnapClaim gave me a fair market value report that clearly beat the insurance offer. I submitted it with my claim and they increased the payout. The process was fast, fair, and worth every penny."

“SnapClaim made a huge difference for me. I had no clue how to value my vehicle post-accident. Their diminished value report was detailed, with comps and expert review. I sent it in and got a great settlement in less than a week. Truly amazing.”

“SnapClaim is a game-changer. I used their fair market value report after a total loss, and it helped me negotiate a much better offer. The design, speed, and clarity of the report made a real difference with my adjuster..”

Certified appraisal report in minutes.

Let us help you recover the true value of your car

Free Estimate, no credit card required.