Diminished Value Appraisal in

Arizona

Recover the lost value of your car after an accident with a certified Arizona diminished value appraisal.

Fast, accurate, and court-ready reports trusted by insurers and attorneys. No delays. No guesswork.

No credit card required.

Filing a Diminished Value Claim in Arizona: What You Need to Know

Does Arizona Allow Diminished Value Claims?

- Third-party (liability) claims — Yes. If another driver is at fault, Arizona permits recovery of the vehicle’s post-repair loss in market value in addition to reasonable repair costs. Arizona courts apply the Restatement (Second) of Torts § 928 measure: cost of repair plus any proven residual diminution and loss of use. See Oliver v. Henry (Ariz. Ct. App. 2011) and Farmers Ins. Co. of Ariz. v. R.B.L. Inv. Co. (Ariz. App. 1983).

- First-party (collision) claims — Generally no DV. Under your own collision coverage, DV is usually not owed unless the policy expressly provides it. Industry and legal guidance treat DV primarily as a liability (third-party) damage element, not a standard first-party collision benefit. See a 50-state survey and definitions from Matthiesen, Wickert & Lehrer (MWL) and Arizona trade guidance (Independent Insurance Agents of AZ) noting DV applies to liability losses, not routine collision claims.

Relevant Arizona Law & How Damages Are Measured

- Measure of property damage: Difference in value immediately before vs. after the harm; if repaired, damages include cost of repair plus any proven residual loss in value and loss of use. Oliver v. Henry (adopting Restatement § 928 and relying on R.B.L. Inv. Co.).

- Comparative negligence: Arizona follows pure comparative negligence (damages reduced by your percentage of fault). See A.R.S. § 12-2505.

- Statute of limitations (private defendants): Two years for injury to personal property (includes DV). See A.R.S. § 12-542.

- Claims involving public entities/employees: Strict pre-suit Notice of Claim within 180 days and a one-year filing deadline. See A.R.S. § 12-821.01 (notice) and § 12-821 (one-year limitations).

Types of Diminished Value Recognized

- Immediate DV: The drop in market value right after damage, before repairs.

- Inherent DV: The market stigma that remains after proper repairs because the vehicle now has an accident history.

- Repair-related DV: Additional loss due to substandard repairs, frame damage, panel misalignment, or use of inferior parts.

What to Document for an Arizona DV Claim

- Accident report: Obtain your report from the investigating agency (e.g., Arizona DPS Records or the city police portal; minor fender-benders may use the DPS Citizen’s Collision Report).

- Liability evidence: citations, admissions, photos, witness info.

- Repair records: estimates, final invoices, parts lists, and any pre- and post-repair scan/calibration sheets.

- Photos: clear pre-repair damage photos and post-repair condition photos (multiple angles, VIN tag/dashboard).

- Professional DV appraisal (post-repair): A written valuation showing pre-loss value, post-repair value, and the DV figure, with data and methodology. (Arizona appellate courts accept expert appraisal as competent proof; see Oliver.) Order yours from SnapClaim.

Step-by-Step: How to File a Diminished Value Claim in Arizona

- Confirm fault and insurance paths. If you’re not at fault, pursue a third-party DV claim against the at-fault driver’s liability insurer. (DV under your own collision policy is typically not covered unless your policy expressly includes it.) See MWL’s overview of DV frameworks: source.

- Finish repairs or obtain final repair documentation. Courts assess residual loss in value after repairs. Oliver v. Henry.

- Get an independent DV appraisal. Use a credentialed appraiser experienced with insurer negotiations. Arizona courts allow proving DV with expert valuation; you don’t need to sell the vehicle to prove loss. Oliver.

- Assemble your demand package. Include: police report, liability evidence, before/after photos, repair documents, and the appraisal. State claim facts, legal basis (Arizona law allows repair cost + residual DV), your DV dollar amount, and a payment deadline.

- Send a written demand to the liability insurer. Keep proof of delivery. Be professional and precise; cite legal authority and attach your exhibits.

- Negotiate. Insurers may counter. Your appraisal quality and documentation drive outcomes. (There is no mandated formula in Arizona; credible market evidence controls.)

- Escalate if needed:

- Regulator help (claims handling issues): File a complaint with the Arizona Department of Insurance & Financial Institutions (DIFI) or use the NAIC complaint portal for AZ: submit here.

- Civil action: For private defendants, the limitations period is 2 years (A.R.S. § 12-542). For public entities/employees, serve a Notice of Claim within 180 days and file suit within 1 year (A.R.S. §§ 12-821.01, 12-821).

- Small claims / Justice Court: For modest DV amounts, consider Arizona Justice Court options. (As of 2025, legislation (SB 1022, Ch. 94) increased small-claims jurisdiction from $3,500 to $5,000; court websites may lag in updating.)

Deadlines You Must Track

- Standard property damage/DV (private party): 2 years from accrual. A.R.S. § 12-542.

- Claims vs. public entities/employees: Notice of Claim within 180 days, then suit within 1 year. A.R.S. § 12-821.01; § 12-821.

- Comparative fault may reduce DV: Arizona is pure comparative negligence. A.R.S. § 12-2505.

Practical Tips for Evidence & Negotiation

- Don’t rely on generic “formula” worksheets. Arizona law looks to real market evidence and expert valuation, not a mandated multiplier.

- Ask your repairer for all scan/calibration printouts and final quality-control sheets—these support (or rule out) repair-related DV.

- Keep communications professional and fact-based; insurers respond to organized, defensible files.

Why Using a Professional Appraisal Is Crucial

In Oliver v. Henry, the Arizona Court of Appeals affirmed that an owner can prove diminished value with expert testimony/appraisal—no sale required. Insurers and courts want a substantiated, reproducible analysis tied to VIN-specific comparables, condition, equipment, mileage, and repair impacts. SnapClaim provides attorney-grade reports designed for insurer review and litigation support:- Order a Diminished Value Report — fast turnaround, negotiation-ready.

- Diminished Value Overview — learn how DV is calculated and proven.

- Fair Market Value (Total Loss) Appraisal — if your vehicle is totaled instead of repaired.

- Money-Back Guarantee Policy — risk-free assurance on report quality.

- Diminished Value State Laws — compare rules across states.

References & Resources

- Oliver v. Henry (Ariz. Ct. App. 2011) — expert appraisal can prove DV without a sale.

- A.R.S. § 12-542 — 2-year statute for injury to property.

- A.R.S. § 12-2505 — pure comparative negligence.

- A.R.S. § 12-821.01 & § 12-821 — Notice of Claim (180 days) and 1-year suit deadline for public entities/employees.

- MWL: Automobile Third-Party Diminution in Value Claims — DV types and national overview.

- Arizona Department of Insurance & Financial Institutions — File a Complaint (NAIC portal here).

- Arizona DPS — Public Records (accident reports) and Citizen’s Collision Report.

Internal SnapClaim Resources

Recover Diminished Value After an Accident in Arizona

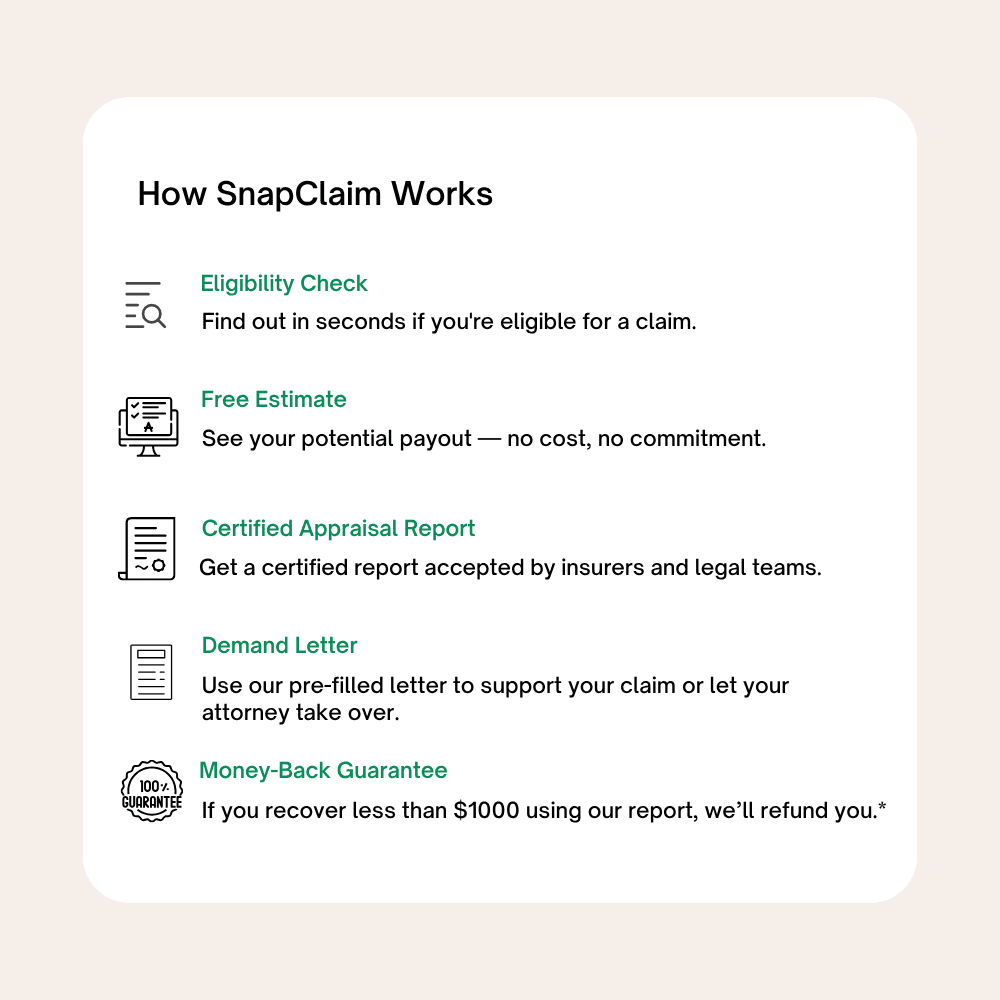

If your vehicle was damaged in an Arizona car accident, it may lose resale value even after professional repairs. This is called diminished value. With a Arizona diminished value appraisal, you can prove the loss and recover it under state law. SnapClaim makes filing an Arizona diminished value claim simple. We provide a free diminished value estimate, a certified Arizona diminished value appraisal report, and an insurer-ready demand letter you can submit immediately. No delays. No guesswork. Just fast, accurate documentation trusted by attorneys and insurance adjusters across Arizona.

"After my accident in Tucson, the repairs didn’t fully restore my car’s resale value. SnapClaim prepared a detailed Arizona diminished value report and a demand letter for me the same day. My attorney submitted it, and the insurance company quickly agreed to pay the difference. I was impressed with how fast and professional the process was."

Nina R.

Tucson, AZ

Frequently asked questions:

- Does Arizona allow diminished value claims?

Yes. Arizona recognizes diminished value claims when your vehicle loses market value after an accident. Read more in our full State Laws Guide.

- Why do I need an appraisal instead of just repair invoices?

Repair invoices only show the cost of fixing your car, not the drop in resale value. An diminished value appraisal documents the market loss and is essential when negotiating with insurers.

- How much does an Arizona diminished value appraisal cost?

The appraisal report cost $350. Every order includes a certified appraisal, comps, and insurer-ready documentation. Learn more about our Money-Back Guarantee.

- Will insurance companies accept a SnapClaim appraisal in Arizona?

Yes. Our reports are designed to meet insurer standards and have been used successfully in settlements across the U.S. Review our Certified Auto Appraisal Guide to see how our process works.

- How long does it take to get my report?

Most Arizona reports are ready within an hour. Start your free estimate here: Get a Diminished Value Report.

- Can I file a diminished value claim if I was at fault?

In Arizona, diminished value is usually a third-party claim against the at-fault driver’s insurance. Learn the difference between claim types in our Diminished Value Overview.

- Where do I order an Arizona diminished value appraisal?

You can order directly online: Start Your Report. If your vehicle is a total loss, visit our Fair Market Value Appraisal page instead.

Arizona diminished value appraisal in minutes.

Don’t leave money on the table. Start your free estimate now and get a certified Arizona diminished value appraisal report within hours.

Free Estimate, no credit card required.