Even after a perfect repair job, your car is worth less simply because it has an accident on its record. This drop in resale price is called diminished value, the hidden financial loss that follows nearly every collision. You fixed the physical damage, but the financial damage—the drop in what a buyer is willing to pay—is still there.

What Is a Diminished Value Car After Accident?

Picture this: two identical used cars are for sale. Same make, model, year, and mileage. One has a clean vehicle history report, while the other was in an accident and repaired. Which one would you buy?

Even if you considered the repaired car, you wouldn’t pay the same price. That price difference is its diminished value.

Your insurance company pays to fix the physical damage, but they almost always sidestep this real financial loss. This leaves you, the vehicle owner, to absorb the cost when you decide to sell or trade in your car. It’s a loss you didn’t cause but are expected to carry.

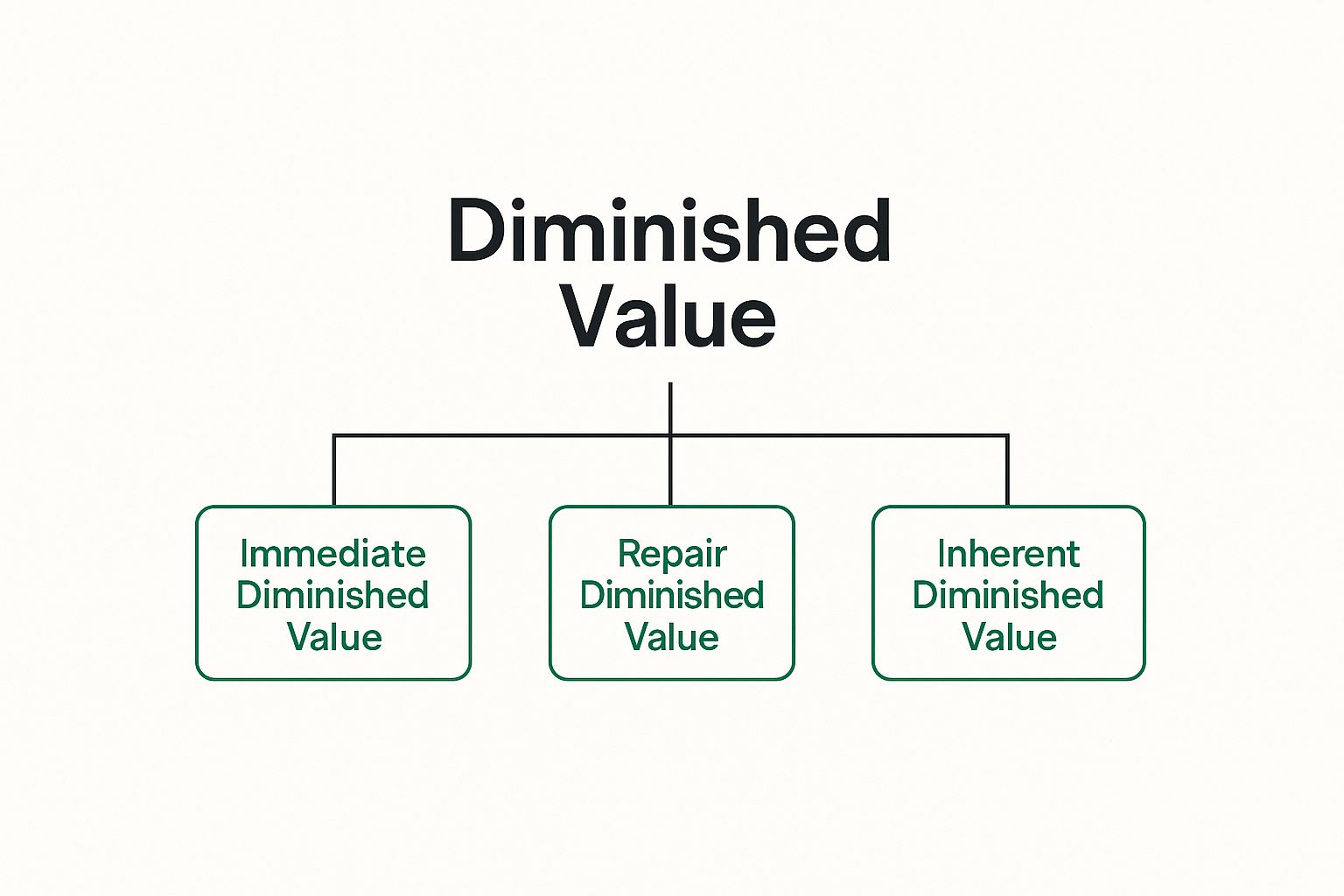

Three Types of Diminished Value Explained

To get what you’re owed, you need to understand the different ways your car’s value can drop. Diminished value isn’t a single concept; it breaks down into three distinct types.

| Type of Diminished Value | What It Means for You | Real-World Example |

|---|---|---|

| Immediate Diminished Value | This is the instant drop in value the moment an accident happens, before any repairs. It’s the gap between its pre-crash market value and its value as a damaged vehicle. | A car worth $25,000 gets into a fender bender. In its damaged state, before heading to the shop, it might only be worth $18,000. The immediate DV is $7,000. |

| Repair-Related Diminished Value | This loss comes from poor repair work. Think mismatched paint, cheap aftermarket parts, or a strange noise that wasn’t there before. Shoddy repairs make the car worth even less. | The body shop uses a slightly off-color paint or a non-OEM bumper. A sharp-eyed buyer will notice and demand a lower price, adding to the financial loss. |

| Inherent Diminished Value | This is the most common and important type. It’s the permanent loss in value that exists even after your car has been repaired perfectly. The simple fact that it has an accident history makes it less desirable. | Your car is repaired flawlessly to factory standards. Still, when you go to sell it, a buyer sees the accident history and offers you $3,000 less than an identical car with a clean record. |

For most people fighting an insurance company, the battle is over Inherent Diminished Value.

The infographic below shows how these three types of loss all fall under the wider umbrella of diminished value.

This makes it clear that Inherent Diminished Value is the core issue for most car owners, since it sticks around long after the vehicle looks as good as new.

Why This Loss Is So Significant

The financial hit from diminished value is not pocket change. Kelley Blue Book experts have noted that a repaired vehicle can lose a significant portion of its market value just because of its accident history. This steep decline comes from one simple thing: buyer fear. People worry about hidden damage or the long-term reliability of a car that’s been in an accident.

This permanent loss is exactly what you are entitled to claim from the at-fault party’s insurance.

Key Takeaway: Your car’s value drops the second an accident happens. While insurance covers the repairs, the permanent loss in resale value—known as Inherent Diminished Value—is a separate, recoverable damage that you have every right to pursue.

Filing a claim for this loss is crucial for protecting your vehicle’s equity. To navigate this process successfully, you need to understand the basics of what is a diminished value claim. Proving this loss requires objective, data-driven evidence, which is precisely what a professional appraisal provides.

How Insurers Calculate Your Car’s Diminished Value

When you file a diminished value car after accident claim, the insurance company uses specific methods designed to calculate—and usually minimize—what they have to pay you. Understanding their playbook is the first step toward challenging their inevitable lowball offer.

Most insurance carriers use a one-size-fits-all formula known as “Rule 17c.” Originally from a Georgia court case, this formula has become an industry go-to because it systematically reduces the final payout through a series of caps and modifiers. It’s a tool built for their benefit, not yours.

Unpacking the 17c Formula

The 17c formula is a tool designed to start with your car’s pre-accident value and then chip away at it. Here’s a simplified breakdown:

- Start with Market Value: The process begins by looking up your vehicle’s fair market value before the accident, often using a guide like NADA or Kelley Blue Book.

- Apply a 10% Cap: Right away, the formula caps the maximum possible diminished value at 10% of the car’s pre-accident value. If your car was worth $30,000, the most you could get is $3,000—no matter how severe the damage was.

- Multiply by a Damage Modifier: Next, they apply a multiplier based on the severity of the damage. This is a subjective scale that gives the adjuster a way to shrink the number even further.

- Multiply by a Mileage Modifier: Finally, they apply another multiplier based on your car’s mileage, penalizing you for having driven it.

The final number is almost always just a fraction of your vehicle’s true lost value.

Key Takeaway: The 17c formula is engineered to produce a low, predictable number for the insurance company. Its built-in caps and arbitrary multipliers ignore how real car buyers think.

Why This Method Is Flawed

The biggest problem with the 17c formula is that it ignores the single most important factor: actual market perception. What a potential buyer is really willing to pay for a car with an accident on its record is what truly determines its diminished value.

- It’s Arbitrary: The 10% cap has no basis in real-world market data. A vehicle with significant structural damage could easily lose far more than 10% of its value.

- It’s Inconsistent: The damage and mileage multipliers are subjective and can be applied inconsistently by different adjusters.

- It’s Not Localized: The formula fails to account for local market conditions, which heavily influence resale values.

An insurer’s reliance on this formula is a negotiation tactic. They present it as a standard calculation, hoping you’ll accept their first offer without question. To learn more about how different factors impact your car’s value, check out our guide on how much an accident will devalue a car.

This is why getting an independent appraisal is so critical. A SnapClaim report doesn’t use flawed, self-serving formulas. Instead, it provides a data-driven valuation based on real-time market evidence. This gives you the hard proof needed to counter the insurer’s inadequate assessment.

The Real-Life Hit to Your Car’s Value

The term “diminished value” can sound like insurance jargon until you see actual dollars disappear from your car’s worth. This isn’t just a technicality; it’s a real, tangible financial loss. Let’s look at how an accident history impacts the resale value of everyday vehicles.

Imagine you own a popular SUV worth $35,000 before someone rear-ends you. After $6,000 in high-quality repairs, it looks perfect. But that accident is now a permanent stain on its vehicle history report. A year later, you go to trade it in. The dealer pulls up the report and offers you $4,000 less than an identical SUV with a clean record, pointing directly to the collision history.

That $4,000 is your diminished value. It’s real money out of your pocket.

Real-World Examples of Financial Loss

To really drive the point home, let’s look at a couple of common scenarios. These examples show how an accident history scares off buyers and lowers what they’re willing to pay.

- The Luxury Sedan: A two-year-old luxury sedan worth $50,000 is T-boned. The repairs cost $10,000 and are flawless. Even so, its resale value could easily drop by $7,000 or more. Buyers in the high-end market are extremely picky and will almost always choose a car with a clean history.

- The Work Truck: A contractor’s one-year-old pickup, valued at $45,000, suffers frame damage. It’s repaired to factory specs, but the history of structural damage makes future buyers nervous, leading to a potential $5,500 loss in value.

These aren’t just made-up numbers. They represent the financial hit thousands of vehicle owners experience when they discover their investment has been permanently devalued by an accident that wasn’t their fault. Wondering what your vehicle’s specific loss might be? You can get a clearer picture by requesting a free diminished value estimate.

The Bigger Picture: The Economic Cost of Accidents

Your personal financial loss is just one piece of a much larger economic puzzle. On a global scale, the cost of traffic accidents is staggering.

According to the World Health Organization, road traffic crashes cost most countries 3% of their gross domestic product.

That massive figure covers everything from healthcare costs and lost productivity to property damage—including the often-ignored diminished value of millions of vehicles worldwide. On top of the vehicle damage, the true cost can also include expenses from addressing physical injuries, adding another layer of financial stress.

When you don’t file a diminished value claim, you’re volunteering to pay for a loss that the at-fault party’s insurance policy should cover. Protecting your investment starts with recognizing this loss and taking the steps to get that money back.

How to Build a Strong Diminished Value Claim

Fighting for the compensation you deserve takes more than a quick phone call to the insurance company. To get what you’re rightfully owed, you need to build a powerful, evidence-based argument they can’t simply brush aside. Your goal is to turn your belief that you’re owed money into a fact-based demand.

Gathering Your Core Evidence

First, you need to assemble all the essential documents from the accident and repairs. This foundational paperwork sets the stage for your entire claim.

Here’s what you need to collect:

- The Police Report: This official document is critical for establishing who was at fault.

- Repair Invoices and Estimates: The final, itemized bill from the body shop proves how extensive the damage was.

- Photos and Videos: A complete visual record is a must. Gather photos from before the accident, right after the crash, and of the finished work.

- Vehicle History Report: A report from CARFAX or AutoCheck shows the accident is now a permanent part of your vehicle’s record—the root of inherent diminished value.

This documentation proves the accident happened and that significant repairs were needed. You can learn more about the complete process in our detailed guide on how to file a diminished value claim.

The Centerpiece of Your Claim: An Independent Appraisal

While the documents above are crucial, they don’t prove the financial loss you’ve suffered. This is where an independent, certified appraisal becomes your most important tool. An appraisal from an unbiased third party like SnapClaim carries far more weight than the insurer’s internal math because it’s based on real-world market data, not a formula designed to save them money.

Key Takeaway: A certified appraisal report is the single most powerful piece of evidence you can have. It provides a credible, data-driven valuation of your loss that an insurance adjuster cannot easily ignore.

A professional report shows you’ve done your homework and are serious about being paid fairly. It shifts the conversation away from the insurer’s flawed 17c formula and forces them to deal with the actual market value your car has lost. A SnapClaim report supports your negotiations with the insurer and helps strengthen your claim.

Navigating State Laws and Your Right to Compensation

Your right to compensation for a diminished value car after accident depends almost entirely on the laws in your state. These rules aren’t the same everywhere, creating a patchwork of regulations across the country. Knowing your local laws is the first and most critical step.

First-Party vs. Third-Party Claims

The biggest legal hurdle is the difference between a first-party and a third-party claim. This distinction determines which insurance company is responsible for your diminished value.

- Third-Party Claim: This is the most common path. You file a claim against the at-fault driver’s insurance policy. In nearly every state, you have a legal right to be “made whole,” which includes recovering the value your vehicle lost.

- First-Party Claim: This is when you file against your own insurance company. Most insurance policies are written to specifically exclude coverage for diminished value in first-party claims, making it nearly impossible to get paid in most states.

Because of this, proving the other driver was at fault is essential for almost all diminished value cases.

Your State Matters Most

Every state has its own statutes and court decisions that shape diminished value claims. Some states make it easier to recover what you’re owed, while others have tougher requirements. It’s vital to know where you stand.

Knowing your rights is the foundation of a successful negotiation. Insurers are well aware of the laws in your state, and being uninformed puts you at a significant disadvantage.

To help you get clarity, we’ve put together a collection of state-specific diminished value guides. It’s also smart to be aware of how broader legal changes, like the recent Florida Tort Reform, might affect your rights. While roads are getting safer in some regions, non-fatal accidents still add millions of cars with damaged histories to the market each year.

Ultimately, no matter your state’s laws, one thing is constant: you need objective proof of your loss. A SnapClaim appraisal gives you the hard data needed to back up your claim.

How a SnapClaim Appraisal Strengthens Your Position

Filing a diminished value claim is about proving a real, quantifiable financial loss. An insurance adjuster’s job is to minimize payouts, and they will almost always dismiss a claim that isn’t backed by solid, credible evidence. This is where a certified appraisal from SnapClaim becomes your most powerful tool.

Simply put, a SnapClaim report transforms your argument from an opinion into an objective, data-driven fact. It provides the proof needed to counter the insurer’s lowball offer, which is often based on the flawed 17c formula.

Evidence Overcomes Opinion

An insurance company isn’t going to write you a check based on a gut feeling. They require a formal, documented analysis. A SnapClaim appraisal delivers just that, arming you with a report built on a robust and transparent methodology.

We use:

- Real-Time Market Data: We analyze current listings and recent sales of vehicles identical to yours, both with and without accident histories, to establish what your car is actually worth today.

- Comparable Sales Analysis: We pinpoint specific, comparable vehicles sold in your geographic area to give you a localized and accurate picture of your car’s diminished value.

- Expert Assessment: Our certified appraisers review all documentation to determine how the specific damages impact your vehicle’s desirability to a real-world buyer.

This comprehensive report gives the adjuster concrete evidence they can’t easily ignore. It forces them to negotiate based on the actual financial hit you’ve taken. You can learn more about what goes into a professional car appraisal after an accident on our services page.

Our Risk-Free Guarantee Makes It an Easy Decision

We understand you might hesitate to spend money to recover money, especially after an accident. That’s why we stand behind our work with a clear, money-back guarantee that removes the financial risk.

If the insurance recovery from your diminished value claim is less than $1,000, we will refund your appraisal fee in full. No questions asked.

This guarantee makes investing in a professional report a confident first step. It ensures you won’t be out of pocket for pursuing the compensation you’re rightfully owed. Let SnapClaim provide the proof you need to level the playing field and support your negotiations for a fair settlement.

Frequently Asked Questions (FAQ)

Here are answers to a few common questions we hear from drivers about their diminished value car after accident claim.

How long do I have to file a diminished value claim after accident?

Every state has a statute of limitations, which is a legal deadline for filing property damage claims. This period can range from one to several years, depending on where the accident occurred. It’s crucial to act quickly after your repairs are complete, or you could lose your right to file. You can find the deadline for your area on our state-specific law pages.

Will filing a diminished value claim raise my insurance rates?

No, it should not. A diminished value claim after accident is a third-party claim, meaning you file it against the at-fault driver’s insurance. Because you aren’t filing against your own policy for an accident you didn’t cause, your insurance company has no reason to raise your rates.

Can I claim diminished value after accident if I was at fault for the accident?

Unfortunately, no. Your own insurance policy is designed to cover the damage you cause to others. It is not designed to cover the inherent loss of value to your own vehicle when you are the at-fault driver. This type of loss is almost always excluded from standard collision coverage.

What should I do if the insurance company denies my claim?

An initial denial or a low offer is a standard tactic. This is the start of the negotiation, not the end. Your best response is to counter their rejection with undeniable proof. Politely reject their offer in writing and provide them with your certified SnapClaim appraisal report. This provides a credible, data-backed valuation of your loss and forces them to justify their position.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This article was reviewed by SnapClaim’s team of certified auto appraisers and claim specialists with years of experience preparing court-ready reports for attorneys and accident victims. Our content is regularly updated to reflect the latest industry practices and insurer guidelines.

Get Started Today

Ready to prove your claim? Generate a free diminished value estimate in minutes and see how much you may be owed.

Get your free estimate today