After an accident, the big question is always the same: what’s my car really worth now? Forget the quick online calculators. To get the compensation you’re owed from an insurance company, you need a professional, independent car appraisal—it’s your most powerful tool for negotiating a fair settlement.

Why an Independent Car Appraisal Is Crucial

Here’s the thing about insurance companies: their valuation of your damaged or totaled car serves their bottom line, not yours. Their goal is to minimize the payout, which is why their first offer often feels insultingly low. It probably is.

This is where an independent appraiser changes the game. They work for you, not the insurance company. Their only job is to calculate your vehicle’s true Fair Market Value (FMV) using objective data and professional expertise. An FMV is simply the price your car would have sold for right before the accident. This appraisal levels the playing field, shifting the conversation from opinion to a negotiation based on hard facts.

The Power of a Certified Report

A certified appraisal report isn’t just a number on a page—it’s a legally defensible document that strengthens your negotiating position. It gives you the concrete proof needed to push back against an insurer’s low valuation. Honestly, it’s hard for them to argue with a detailed, expert report.

This becomes a must-have in a few key situations:

- Total Loss Claims: It provides the evidence to argue for a higher insurance total loss payout that truly reflects your car’s pre-accident worth.

- Diminished Value Claims: It officially documents the drop in resale value your car has suffered even after perfect repairs, helping you recover that loss. A diminished value claim is your right when the accident wasn’t your fault.

- Private Sales or Disputes: It sets a credible, fair price for a potential buyer or for use in legal matters like a divorce or estate settlement.

Don’t think of the car appraisal cost as an expense. It’s an investment that arms you with the official documentation you need to walk into negotiations with confidence and walk out with the settlement you actually deserve.

To see how this works in practice, check out our full guide on getting a car appraisal after an accident.

What Drives the Car Appraisal Cost?

When you get a quote for a professional vehicle valuation, it’s natural to wonder what’s behind the car appraisal cost. You’re paying for a skilled expert’s time, in-depth research, and a report built to withstand scrutiny from an insurance company.

A cheap, surface-level report might look okay at first, but it can easily fall apart when an insurance adjuster starts picking it apart. A quality appraisal from a company like SnapClaim is an investment in accuracy and defensibility.

The Appraiser’s Expertise and Certification

A huge part of the cost comes down to the appraiser’s qualifications. You aren’t just paying for someone’s opinion; you’re investing in professional judgment backed by legitimate, industry-recognized credentials.

- Certifications: Professionals often hold certifications from respected organizations like I-CAR or ASE. These aren’t just fancy badges; they prove a deep understanding of vehicle construction, repair methods, and damage analysis.

- Experience: A seasoned appraiser has handled thousands of cases and knows exactly how insurance adjusters think. They can spot common tactics used to undervalue claims and build a report that counters them from the start.

This combination of training and real-world experience ensures the final document is both accurate and authoritative.

The Complexity of Your Claim

Not all appraisals are created equal because no two situations are the same. The complexity of your case directly impacts the amount of work required, and that’s reflected in the price.

A simple fair market valuation for a private car sale, for example, is fairly straightforward. An insurance claim, however, is a different beast entirely. A claim for car value after an accident demands a sophisticated analysis of market data, comparable vehicle sales, and the specific type of damage sustained. This takes much more time and research than a basic value check.

The Depth of the Report

Finally, the car appraisal cost reflects the quality and detail of the final report itself. A generic one-page summary from a free online tool isn’t going to hold up against an insurance company’s team of adjusters.

A comprehensive, court-ready report from a service like SnapClaim is built to be ironclad evidence. It typically includes:

- Detailed Market Analysis: A thorough review of what similar cars are actually selling for in your local area.

- Methodology Explanation: A clear, step-by-step breakdown of how the valuation number was reached.

- Supporting Evidence: All the documentation, photos, and data needed to justify the final figure.

This level of detail transforms your claim from a simple request into a well-supported demand for the money you’re rightfully owed.

Typical Cost Ranges for Different Appraisals

Figuring out the typical car appraisal cost is the first step to budgeting smart and knowing a fair price when you see one. The cost depends on what you need the report for—a simple valuation for a private sale is different than a detailed report built to take on an insurance company.

For most standard market value reports, you can expect to pay between $150 and $300. These reports are great for establishing a baseline value, but they usually don’t have the deep analysis required to win an insurance dispute.

Specialized Appraisal Costs

When you’re going toe-to-toe with an insurance company, you need a much more robust and defensible report.

- Diminished Value Appraisals: These are complex. They require a deep dive into market data to prove how much value your car lost after repairs. A certified diminished value report typically runs from $400 to $600.

- Total Loss Appraisals: If you’re fighting a lowball total loss offer, an appraiser must meticulously document your vehicle’s pre-accident condition, features, and true worth. These reports also tend to fall in the $300 to $600 range.

We get into the nitty-gritty in our detailed guide on the diminished value appraisal cost.

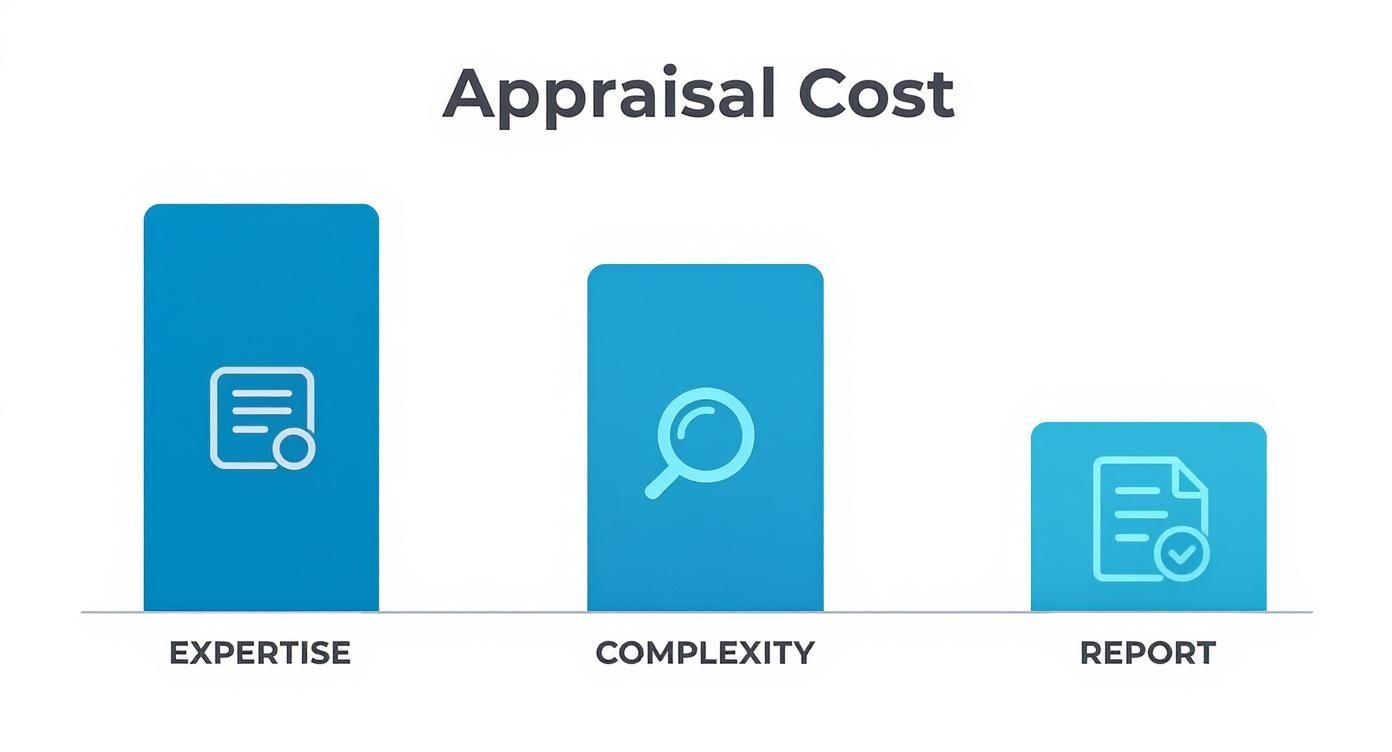

This infographic breaks down what drives the final price tag on an appraisal.

As you can see, the appraiser’s experience, the complexity of your claim, and the depth of the report are the three main factors behind the cost.

The wider auto market also plays a huge role. Things have been volatile lately, making accurate valuations trickier than ever. With average used car prices hovering around $25,512 in early 2025, appraisers must dig deep to nail down a car’s true value, and that extra work can be reflected in the price. Even straightforward regulatory checks like Texas state inspection costs come with set fees. With appraisals, you’re paying for the level of detail your specific situation demands.

How Market Volatility Impacts Your Appraisal

A car’s value isn’t set in stone; it shifts with the market. When things are unpredictable, a professional appraisal becomes absolutely essential because outdated book values just can’t keep up.

Factors like new car inventory shortages, manufacturer incentives, and the growth of the electric vehicle (EV) market create a complex landscape for used cars. When the market gets this choppy, an appraiser’s job gets more intense, which is a key reason behind the car appraisal cost.

Why Deeper Research Is Essential

In a volatile market, a quick glance at online listings just won’t cut it. A certified appraiser has to dig deep into a wide range of data points to build a valuation that can stand up to scrutiny.

- Supply and Demand Shifts: A shortage of new cars can send the value of late-model used vehicles soaring—but that wave can crash just as quickly.

- Economic Factors: Big-picture things like tariffs and incentives have a ripple effect on car prices. Appraisers must account for these complex variables, a point echoed in recent automotive market predictions.

- Regional Differences: The exact same car can be worth dramatically different amounts from one state to the next based on local demand.

This in-depth analysis is what separates a real appraisal from a rough estimate. It ensures your report is built on what’s happening right now, not on old assumptions, and provides the proof you need for a fair insurance outcome. Understanding how much your car is worth requires this level of expert attention.

Calculating the ROI of Your Appraisal

So, is paying the car appraisal cost really worth it? The answer is a clear yes when you think of it as an investment, not an expense. An appraisal is a tool to get back what you’re rightfully owed.

Let’s walk through a common scenario. Your insurance company declares your car a total loss and offers you $15,000. It feels low, but how do you prove it? This is where a certified appraisal changes the game.

Turning Opinion into Fact

A professional report transforms the negotiation from your word against theirs into a discussion grounded in verifiable market data.

If a certified appraisal shows your car’s true fair market value was actually $18,500, you now have the concrete evidence to demand that extra $3,500. In this case, spending a few hundred dollars on an appraisal fee helps put thousands back in your pocket. This return on investment supports your case with certified data.

A Risk-Free Decision

We get it. Paying for an appraisal can feel like a gamble when you’re already stressed from an accident. That’s why at SnapClaim, we take the risk completely off the table.

SnapClaim’s Money-Back Guarantee: If your insurance recovery from the claim is less than $1,000, SnapClaim refunds the full appraisal fee—guaranteed.

This guarantee makes your decision easy. You either get a significant return by backing your claim with data, or you get your money back. There’s no downside.

The global auto market is massive, and its complexity affects every car’s value. A professional appraisal cuts through the noise to find what your vehicle is truly worth. You can learn more about global auto industry trends to see why expert analysis is so critical.

Frequently Asked Questions About Car Appraisal Cost

Here are some of the most common questions we get about the car appraisal cost and the process.

How is a professional appraisal different from a free online tool?

Free online tools like Kelley Blue Book provide a decent ballpark estimate based on generic data. A professional appraisal is a deep dive into your specific vehicle, its condition, features, and local market data, resulting in a detailed, legally defensible report that insurers must take seriously.

Can I claim diminished value if the accident wasn’t my fault?

Yes. In most states, you are entitled to file a diminished value claim against the at-fault driver’s insurance policy. This claim is designed to compensate you for the loss in your vehicle’s resale value, even after it has been fully repaired. A certified appraisal from SnapClaim provides the proof you need to negotiate fairly.

Can the at-fault party’s insurance pay for my appraisal?

It’s possible and something you should push for, especially in a diminished value claim. While not guaranteed, some states have laws that support reimbursement for reasonable claim-related expenses. Presenting a certified report shows you are serious and can make the insurer more willing to cover the car appraisal cost to settle the dispute.

What information do I need for a car appraisal?

To get started, have these key documents ready:

Vehicle Basics: Your car’s VIN, make, model, year, and current mileage.

Damage Info: The insurance adjuster’s estimate and any photos of the damage.

Repair Records: The final invoice from the body shop detailing all work done.

About SnapClaim

SnapClaim is a premier provider of expert diminished value and total loss appraisals. Our mission is to equip vehicle owners with clear, data-driven evidence to recover the full financial loss after an accident. Using advanced market analysis and industry expertise, we deliver accurate, defensible reports that help you negotiate confidently with insurance companies.

With a strong commitment to transparency and customer success, SnapClaim streamlines the claim process so you receive the compensation you rightfully deserve. Thousands of reports have been delivered to vehicle owners and law firms nationwide, with an average of $6,000+ in additional recovery per claim.

Why Trust This Guide

This guide was reviewed and verified by SnapClaim’s auto appraisers, who specialize in diminished value and total loss disputes.

Our team continually updates every article to reflect current insurer guidelines, valuation standards, and court-accepted appraisal practices, ensuring that you’re relying on information trusted by professionals nationwide.

Get Started Today

Whether you’re challenging a low total loss settlement or proving your vehicle’s post-repair loss in value, SnapClaim makes it simple to take the next step.

Get your free estimate today or order a certified appraisal report to strengthen your insurance claim.

👉 Get your free estimate today