Even after perfect repairs, a car with an accident history is worth less money. This loss in value is called diminished value, and using a diminished value claim calculator is the first step toward figuring out how much compensation you might be owed. Think of it as the starting point for building a strong case with the at-fault driver’s insurance company.

What a Diminished Value Calculator Really Shows You

When your car is damaged in an accident, the financial impact goes beyond the repair bill. That accident becomes a permanent part of your vehicle’s history report—a major red flag for any future buyer. This history instantly reduces its resale value. It’s a real, tangible loss that the at-fault party’s insurance company is responsible for covering, but they often won’t volunteer to pay for it.

This is where a diminished value claim calculator becomes a powerful tool. It provides a baseline estimate by analyzing your car’s pre-accident value, mileage, and the severity of the damage. Armed with this initial number, you can confidently start a conversation with the insurer about how much you are owed.

The Three Types of Diminished Value

It helps to know exactly what kind of value loss you’re dealing with. A calculator’s estimate mostly focuses on one type, but all three are important to understand.

Inherent Diminished Value: This is the most common type and the focus of nearly every claim. It’s the automatic drop in market value simply because the vehicle now has an accident on its record, even if repairs were flawless.

Repair-Related Diminished Value: This occurs when the body shop does a poor job. Think mismatched paint, cheap aftermarket parts, or lingering mechanical issues. This loss is in addition to the inherent value drop.

Claim-Related Diminished Value: This is less common but can be significant. It happens when an insurer’s actions during the claim—like initially declaring a vehicle a “total loss” before reversing the decision—permanently damage its value.

An online calculator is a fantastic, free tool to get started. But to successfully negotiate with an adjuster, you’ll need more than just an estimate. A professional report from SnapClaim provides the detailed, certified proof needed to support your claim for what you’re rightfully owed.

How Calculators Estimate Your Car’s Value Loss

Ever wondered what happens behind the scenes when you enter your car’s info into a diminished value claim calculator? These tools typically rely on a simplified formula that insurance companies have used for years, often to keep their payouts low. Understanding how this formula works is your first line of defense against a lowball offer because it gives you insight into the adjuster’s starting point.

The Notorious “Rule 17c” Formula

Many online calculators and insurance adjusters initiate their calculations with a formula known as “Rule 17c.” This method became widespread following a key Georgia court case involving State Farm in 2001. While its straightforwardness made it easy for insurers to implement, this same straightforwardness is its greatest limitation for car owners. For those interested in the history, KBB.com provides a detailed overview of how this court case influenced current claims.

The formula operates as follows:

Determine the Pre-Accident Value: Initially, the calculator establishes your vehicle’s fair market value just before the accident, typically using a source like Kelley Blue Book.

Apply a 10% Cap: Subsequently, it imposes a cap, assuming the maximum potential loss is 10% of the car’s value. For a $30,000 vehicle, this instantly restricts your potential claim to $3,000.

Deduct for Damage and Mileage: Finally, it further decreases that $3,000 amount by applying multipliers based on the damage severity and your vehicle’s mileage.

This inflexible approach seldom represents the actual market loss, especially for newer vehicles, luxury cars, or EVs that might lose much more than 10% of their value after an accident.

A standard formula rarely suits everyone perfectly. The 17c rule overlooks a vehicle’s individual history, local market demand, and the impact of structural damage—all factors that matter to a real buyer.

Why a Calculator Is a Start, Not a Finish

Using a diminished value claim calculator is an excellent first step. It gives you a ballpark figure and confirms you have a legitimate claim. However, taking that number alone into a negotiation is like bringing a notepad to a legal battle. Insurance adjusters are trained to rely on this formula because it works in their favor.

That’s why you need to move from a free estimate to a certified appraisal. A professional report from SnapClaim goes beyond generic formulas, providing a detailed analysis of your specific vehicle in your local market. This gives you the concrete evidence needed to challenge the insurer’s low offer and strengthen your claim.

Key Factors That Affect Your Diminished Value

A diminished value claim calculator provides a great starting point, but the real value of your claim is in the details. Every car and every accident is different, and several key factors can dramatically shift the amount you’re owed. Understanding these variables helps you build a solid case that goes far beyond a generic formula.

One of the biggest drivers is your vehicle’s make, model, and age. A two-year-old luxury SUV will see a much steeper drop in value after a collision than a ten-year-old sedan. For newer, high-end vehicles, a clean history is a huge selling point, which makes an accident report particularly damaging to their worth.

Severity and Type of Damage

Where your car was hit and how badly it was damaged are critical. The difference between minor cosmetic touch-ups and major structural repairs is night and day when it comes to diminished value.

Cosmetic Damage: This includes scratches, small dings, or a replaced bumper. This damage still hurts the value, but the loss is usually more limited.

Structural Damage: This is the most significant factor. If the vehicle’s frame or unibody was compromised, the value loss skyrockets. This type of damage leaves a permanent stigma that informed buyers will avoid.

Airbag Deployment: Deployed airbags are a massive red flag on any vehicle history report. They signal a major impact and almost always lead to a much higher diminished value claim.

The standard 10% cap that insurance adjusters use in the 17c formula often fails to cover these realities.

How Vehicle Type and Damage Affect Value Loss

|

Vehicle Type |

Typical Mileage |

Damage Severity |

Potential Value Loss |

|---|---|---|---|

|

10-Year-Old Economy Sedan |

120,000 |

Minor cosmetic (bumper) |

5% – 8% |

|

3-Year-Old Mid-Size SUV |

35,000 |

Moderate (door replacement) |

10% – 15% |

|

2-Year-Old Luxury Sedan |

20,000 |

Severe (frame damage) |

20% – 30% or more |

|

1-Year-Old Pickup Truck |

15,000 |

Severe (airbags deployed) |

25% – 35% or more |

As you can see, a simple 10% rule doesn’t reflect the true market loss for many vehicles. You can discover more insights about diminished value calculations to see just how much these claims can vary.

A dented door is an inconvenience; a bent frame is a permanent scar on a vehicle’s history. Your claim must reflect the true severity of the damage to get fair compensation.

Ultimately, a free online calculator can’t capture this level of detail. A professional SnapClaim appraisal analyzes your specific vehicle, its unique damage, and local market factors to build a data-driven report that provides proof of your actual loss.

Getting a Ballpark Figure for Your Claim

Ready to find out what your diminished value claim might be worth? The quickest way to get a starting point is by using an online diminished value claim calculator. This process is simple—it’s just about plugging in the right details to get a reliable first look.

To get an accurate estimate, you’ll need a few key pieces of information about your vehicle:

Vehicle Identification Number (VIN): Your car’s unique 17-digit ID.

Pre-Accident Value: Its fair market value right before the crash. A trusted resource like Kelley Blue Book (KBB) is perfect for this.

Current Mileage: The exact number from your odometer.

Repair Invoice Details: The total cost of repairs and a summary of what was done, noting any structural repairs.

Putting the Calculator to Work

Let’s walk through a real-world example. Imagine you have a recently repaired Toyota RAV4. You find its pre-accident value was $28,000, and it has 30,000 miles on the odometer. The accident caused moderate damage, and the repair bill totaled $6,500. You would simply enter these details into the calculator, which then runs the data through its algorithm to produce an initial estimate of your car’s value loss.

For instance, another car valued at $21,500 before an accident might be valued at just $17,300 after repairs, suggesting a diminished value of $4,200.

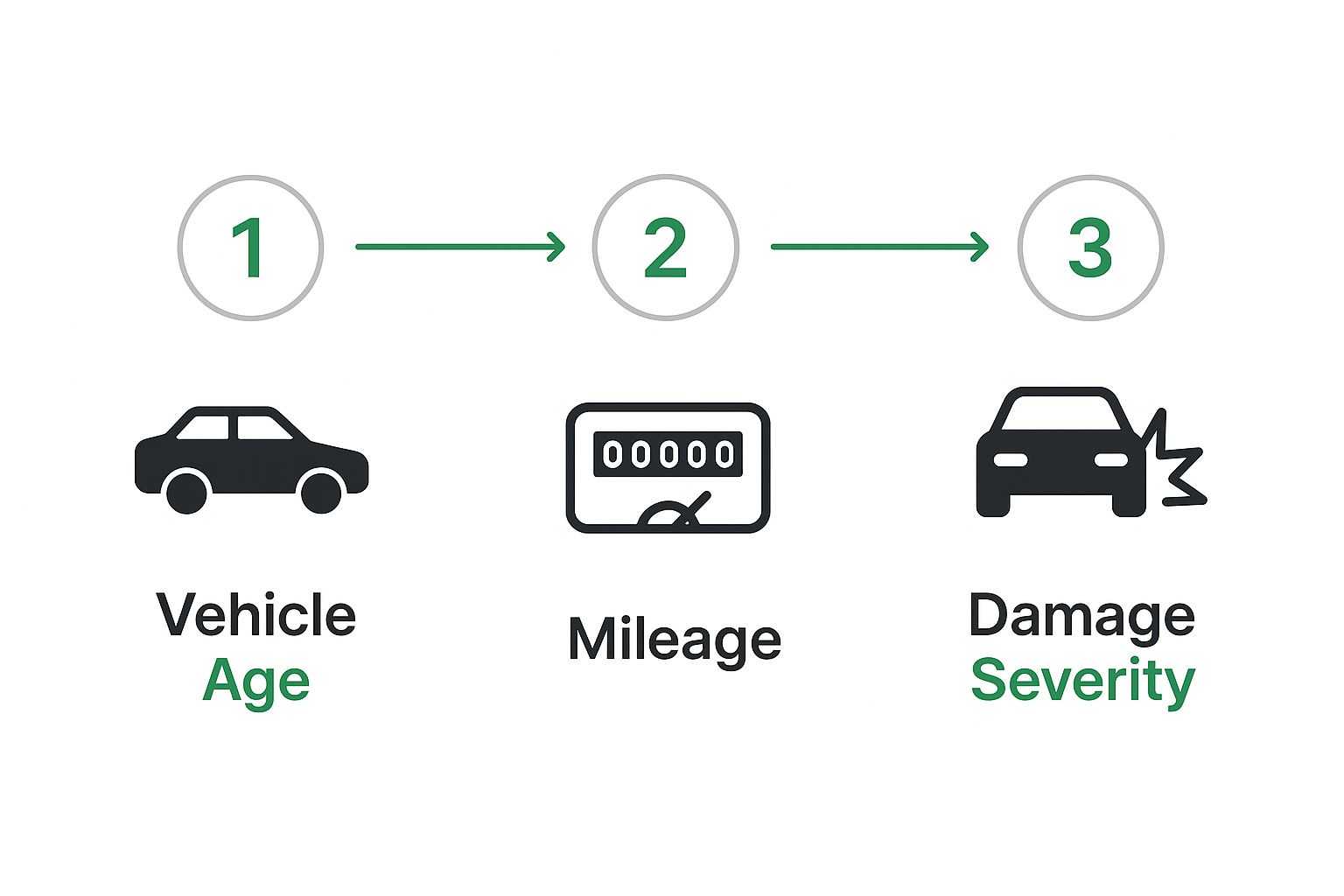

This visual helps break down the core data points—age, mileage, and damage severity—that these calculators rely on to produce an estimate.

Each factor builds on the last to create a basic, but useful, calculation of what your potential claim could be.

Moving Beyond the Calculator for a Stronger Claim

An online diminished value claim calculator is an excellent starting point, but it’s just the first step. When you’re negotiating with an insurance adjuster whose job is to minimize payouts, a simple estimate isn’t enough. You need to move from an estimate to undeniable proof. This is where a professional, certified appraisal becomes your most powerful tool.

Unlike a generic calculation from a broad formula, a certified report is built around your specific situation. It’s a detailed analysis of your car’s unique history and the real-world market where it now has to compete.

The Power of a Certified Appraisal

A professional appraisal provides the hard data that an adjuster can’t easily dismiss. It’s a comprehensive document that methodically builds the case for your diminished value claim. Here’s what makes it so effective:

Vehicle-Specific Analysis: An appraiser examines your exact car, including its pre-accident condition, trim level, mileage, and unique features.

In-Depth Damage Review: The report details the repairs, highlighting critical items like structural damage or airbag deployment that scare off future buyers.

Local Market Evidence: This is the game-changer. It includes data from your local market, showing what similar cars with accident histories are actually selling for. This local evidence is far more compelling than a national average.

This level of detail transforms your claim from a simple request into a well-supported demand. To see how these claims are handled in your area, check out our state law pages.

An online calculator tells an adjuster you think you’re owed money. A certified appraisal report provides proof to support your claim.

We believe every vehicle owner deserves fair compensation, which is why we back every SnapClaim appraisal report with a money-back guarantee. If the insurance recovery from the claim is less than $1,000, your appraisal fee is fully refunded. It’s a risk-free way to arm yourself with the proof needed to negotiate a fair settlement.

FAQ: Common Questions About Diminished Value Claims

Understanding a diminished value claim can be perplexing. Below are answers to frequently asked questions from vehicle owners.

Can I file a diminished value claim if the accident was my fault?

Typically, a diminished value claim is filed against the at-fault driver’s insurance. If you were responsible for the accident, your policy probably won’t cover the reduction in your car’s market value. However, insurance policies can be complicated and differ by state. It’s advisable to review your policy and check the specific regulations in your area on our state law pages.

Is there a time limit for filing a claim?

Yes, and this deadline is important. States impose a legal time limit called the statute of limitations for filing property damage claims. This period varies by state but is usually two to three years from the accident date. Initiating the claim process soon after your vehicle is repaired is recommended to avoid missing your chance for compensation.

What if the insurance company denies my claim?

Don’t worry if this happens. It’s common for an insurance adjuster to deny a diminished value claim or offer a low amount initially. This is often a standard approach to encourage you to abandon the claim. A denial marks the beginning of negotiations, not the end. Your evidence is essential here. A certified appraisal report offers a detailed, data-supported analysis that is more challenging for an adjuster to refute.

Do I need a lawyer to file a diminished value claim?

For most simple claims, a lawyer isn’t needed. A thorough, certified appraisal provides the necessary evidence to negotiate a fair settlement with the insurance company. Consulting an attorney might be wise if you’re dealing with a very high-value vehicle or if there are significant disputes.

Ready to stop guessing and start proving your vehicle’s true loss in value? Get a free estimate from SnapClaim today or order your certified appraisal report to build a rock-solid case. Visit https://www.snapclaim.com to get started and negotiate with confidence.